Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Buckeye Relief is stocked at 122 licensed dispensaries across Ohio, with the deepest coverage in Columbus, Cincinnati, Akron, Athens, and Cleveland. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

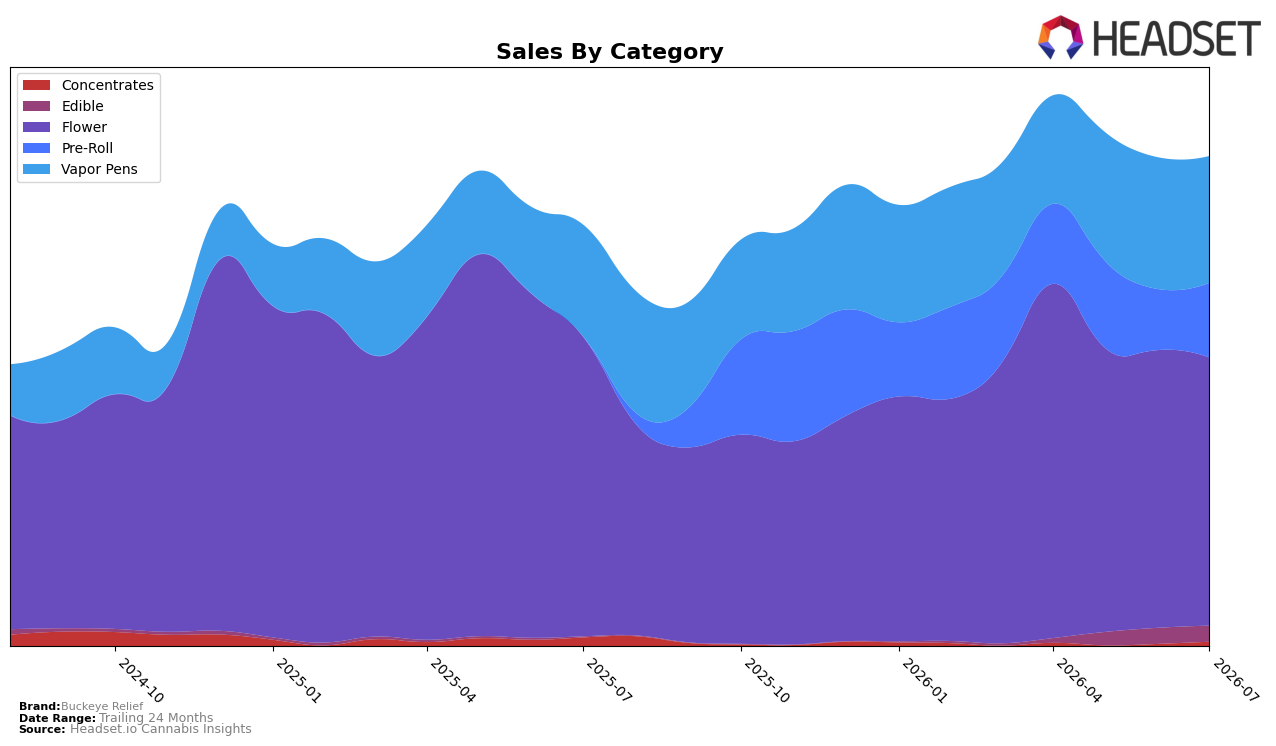

In July 2026, Buckeye Relief’s mix concentrated in Flower at 54.81% share with year-over-year decline of 10.49% and month-over-month dip of 3.45%, while Vapor Pens held 25.89% share with 13.50% YoY growth but a 3.79% MoM slide; Pre-Roll rose to 15.21% share on a 22.53% MoM surge, and Edible, though only 3.22% share, posted a 1,953.25% YoY jump alongside a 0.13% MoM contraction. Concentrates remained sub-1.00% share at 0.87% with a 50.10% YoY decline but spiked 105.34% MoM; average price across the brand fell 33.19% YoY to $29.16, indicating volume-led expansion as total brand sales grew 16.35% YoY and 256.25% over 24 months. The pattern implies Buckeye Relief is reallocating volume toward faster-moving, lower-priced form factors to offset Flower softness while preserving overall growth.

These shifts reposition Buckeye Relief toward value-accessible inhalables and entry formats, with Pre-Roll’s 22.53% MoM upswing and Vapor Pens’ 13.50% YoY gain counterbalancing Flower’s 10.49% YoY and 3.45% MoM declines, and Edible’s 1,953.25% YoY increase adding a small but expanding trial funnel. Holding rank 4 in Flower in Ohio while Flower’s share remains above 50% suggests near-term dependence on Flower for visibility, but the accelerating mix into Pre-Roll and Vapor Pens provides a hedge that supports price elasticity gains from the 33.19% YoY average price drop; this implies a pricing-and-format strategy prioritizing basket penetration over premium positioning.

Competitive Landscape

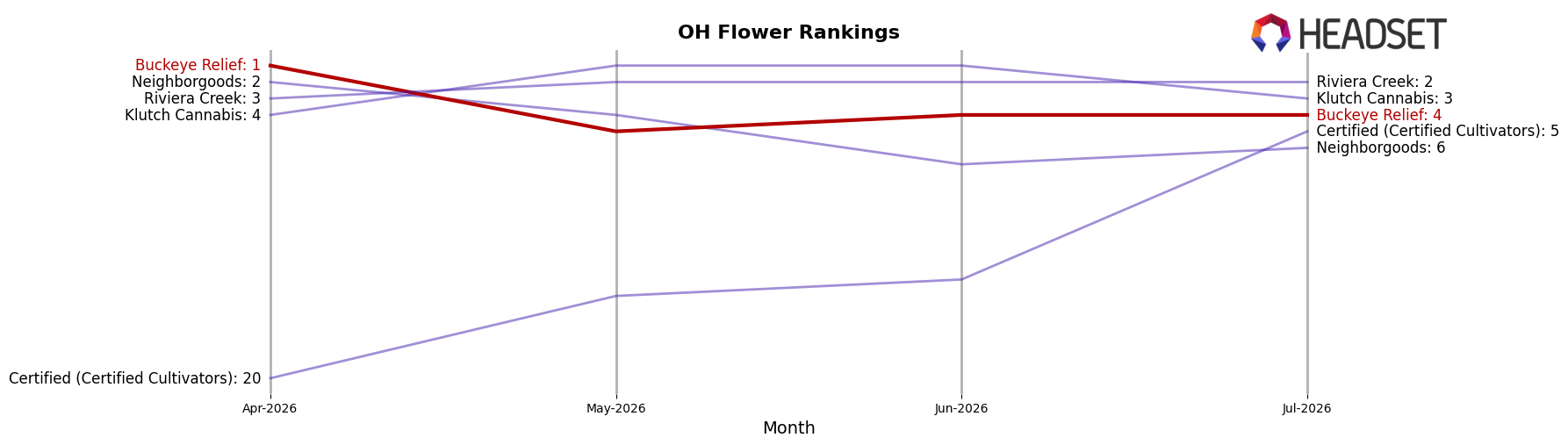

Buckeye Relief sits at rank #4 in OH Flower in July 2026, down 2 positions year over year but off a recent peak at #1 in April 2026 and sliding 3 spots from its #1 position three months ago; in the same window, RYTHM moved to #1 from #6 year over year while growing sales 74.99%, and Klutch Cannabis advanced to #3 from #21 with a 403.04% sales increase, indicating Buckeye Relief’s shift from #1 to #4 is less about absolute collapse and more about being overtaken by faster climbers, which implies a trajectory where maintaining share will require countering competitor momentum rather than regaining a singular lost rank.

Notable Products

The steepest movement in July 2026 was a decline, as Sour Larry Cross (3.5g) fell 12.4% MoM and slid to rank 8 while Cherry Gummy Bar 10-Pack (100mg) dipped 8.5% MoM at rank 1, indicating pressure on Flower even as Edibles keep the top slot. Orange Gummy Bar 10-Pack (100mg) rose 8.3% MoM at rank 2 and Grape Gummy Bar 10-Pack (100mg) eased 1.4% MoM at rank 3, and with three of the top ten being Edibles the format concentration signals sustained pull toward value-driven, repeatable dosage. Strawberry Guava Distillate Dank Tank Disposable (1g) advanced 33.8% MoM at rank 6, but Pre-Rolls occupy ranks 4, 5, 7, and 10, pointing to a split demand curve where ready-to-use formats compress Flower share despite total Flower dollars near $106,985. Altogether, the mix suggests Buckeye Relief is tilting toward convenience-led formats (Edibles, Pre-Rolls, and a rising Disposable) while flagship Flower requires repositioning to stem double-digit MoM declines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.