Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Klutch Cannabis is stocked at 117 licensed dispensaries across Ohio, with the deepest coverage in Columbus, Cincinnati, Cleveland, Lorain, and Warren. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

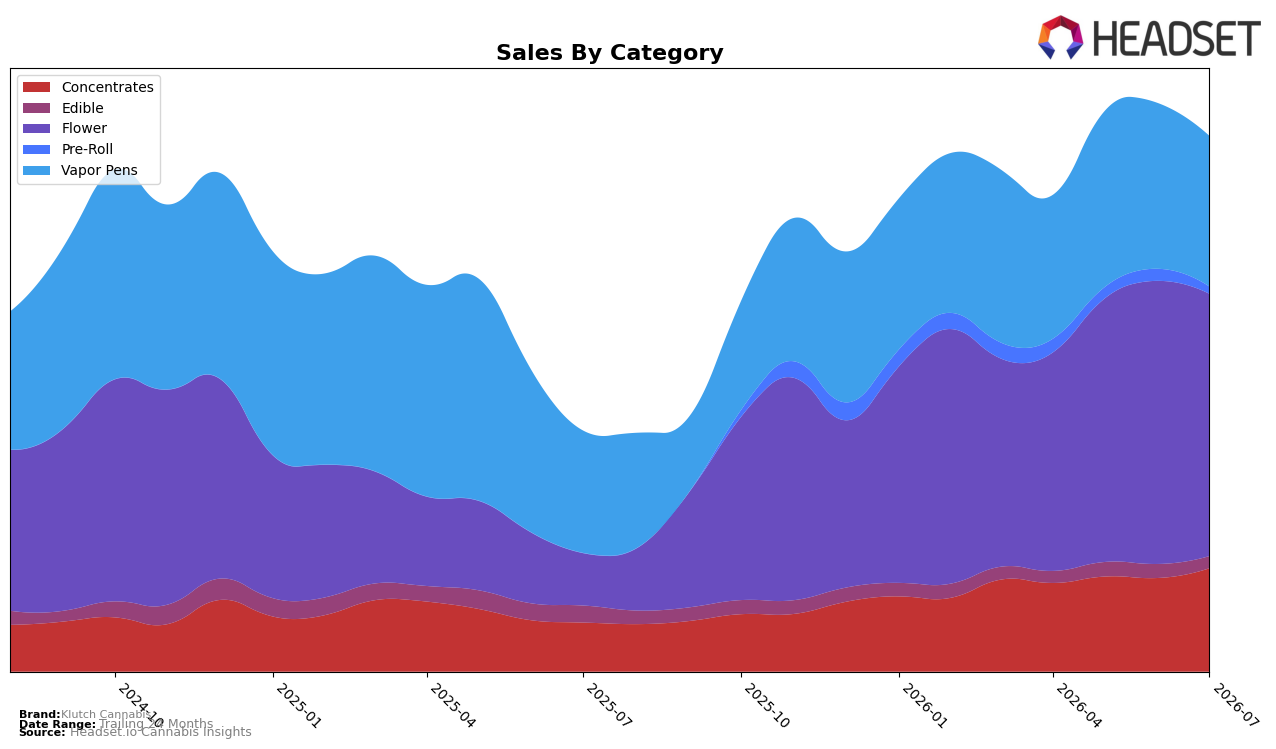

Klutch Cannabis concentrated nearly half of July 2026 sales in Flower at 49.01% share with a 403.04% year-over-year surge, while Vapor Pens held 28.14% share with a 23.22% YoY increase; month over month, Flower slipped 7.37% and Vapor Pens declined 9.09%, contrasted by a 10.42% MoM gain in Concentrates at 19.31% share and a 111.21% YoY rise. Edible contracted to 2.22% share with a 29.19% YoY drop and a 13.47% MoM decline, and Pre-Roll fell 40.69% MoM to 1.31% share with no YoY baseline; paired with a 7.68% YoY increase in average price to $39.41 and a Flower average price of $56.95, the mix implies a deliberate tilt toward higher-price inhalables while trimming underperforming low-share formats.

With Flower ranked 3rd in Ohio and holding 49.01% of brand sales as Concentrates accelerate 111.21% YoY and 10.42% MoM, Klutch Cannabis is consolidating strength in premium inhalables even as Vapor Pens contract 9.09% MoM and Edible shrinks 29.19% YoY. The pattern indicates risk concentration: maintaining a high-price Flower core while building a faster-growing Concentrates second pillar diversifies within inhalables, but falling Pen and Edible shares signal exposure to format volatility that could pressure future rank if the 7.37% MoM Flower dip persists.

Competitive Landscape

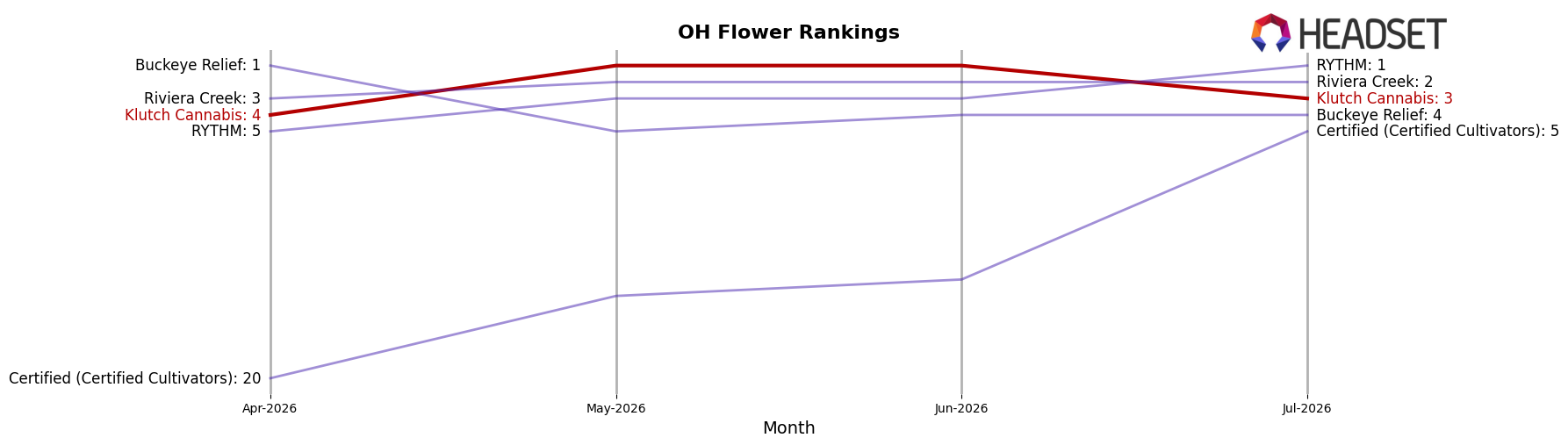

Klutch Cannabis sits at rank #3 in OH Flower in July 2026, improving 18 positions year over year from #21 to #3, and edging up 1 spot since April 2026 from #4 to #3, while also coming off a peak at #1 in June 2026; in parallel, RYTHM holds #1 with a 6-place YoY climb and roughly 75% YoY sales growth, and Riviera Creek sits at #2 with a 1-place YoY improvement despite about a 16% YoY sales decline, indicating Klutch Cannabis is gaining rank amid mixed competitor momentum and its June 2026 peak suggests near-term volatility rather than a locked-in leadership position.

Notable Products

Orange 43 (3.5g) posted the largest month-over-month increase at 76.2% and rose to rank 3 in July 2026, while The Citizen - Orange 43 Full Spectrum Live Resin iKrusher Disposable (1g) fell 16.6% yet still held rank 1. Ice Cream Cake Smalls (14.15g) climbed 55.7% to rank 2, whereas The Citizen - Orange 43 Smalls (14.15g) dropped 44.6% to rank 4. With vapor pens occupying four of the top ten ranks and flower taking three of the top four, the mix points to Klutch Cannabis shifting momentum toward premium flower growth while defending disposable pen leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.