Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Almora Farms is stocked at 497 licensed dispensaries across California, with the deepest coverage in Los Angeles, Sacramento, San Diego, Long Beach, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

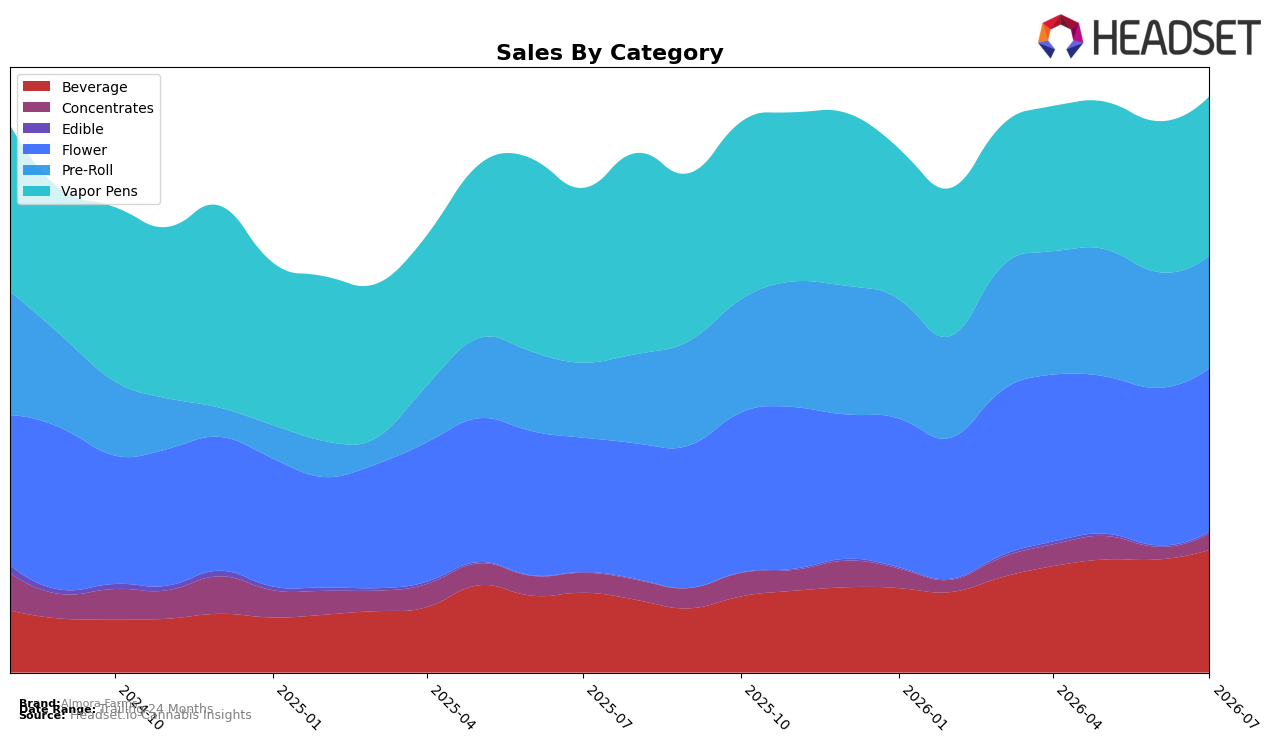

Almora Farms concentrated sales in Flower at 28.19% share with 21.45% year-over-year growth and 3.77% month-over-month, while Vapor Pens held 27.51% share but declined 8.75% year-over-year despite a 5.61% month-over-month lift; Beverage rose to 21.22% share on 52.78% year-over-year and 8.32% month-over-month gains, and Pre-Roll sat at 19.48% share with 49.04% year-over-year but a 2.87% month-over-month dip. Smaller lines diverged as Concentrates fell 15.82% year-over-year but jumped 28.23% month-over-month at 3.07% share, and Edible, though only 0.53% share, grew 49.41% year-over-year and 9.12% month-over-month; paired with an 11.68% year-over-year average price decline to $17.81 and brand-level sales growth of 18.60% year-over-year, July 2026 mix signals volume-led expansion anchored by Flower and Beverage while Vapor Pens lags on an annual basis.

The shift toward Beverage and Pre-Roll, posting 52.78% and 49.04% year-over-year growth respectively alongside Flower’s 21.45%, indicates a portfolio leaning into value-accessible formats as average price down 11.68% year-over-year widens the addressable base; the 5.61% month-over-month lift in Vapor Pens and 28.23% in Concentrates suggest tactical recovery potential without near-term share leadership. With Flower ranked 34 in California and holding the largest internal share at 28.19% versus Vapor Pens at 27.51%, July 2026 positioning implies prioritizing Flower and Beverage to consolidate rank gains while using short-cycle promotions to convert month-over-month momentum in Vapor Pens and Concentrates into sustained share capture.

Competitive Landscape

Almora Farms sits at rank #34 in California Flower in July 2026, improving 8 positions from #42 year over year, but slipping 1 spot from #33 in April 2026; the brand’s peak of #30 in November 2025 further marks a 4-rank retreat from its best point. In contrast, STIIIZY advanced from #2 to #1 with a 59.7% YoY sales increase while Claybourne Co. fell from #3 to #5 alongside a 1.4% YoY sales decline, indicating that Almora Farms’ YoY climb is occurring amid both upward and downward competitor movements. The mixed short-term dip alongside multi-quarter improvement implies Almora Farms is stabilizing in the mid-30s unless near-term execution reverses the slide from its November 2025 peak.

Notable Products

With no SKU posting a month-over-month swing above +50% or below -10% in July 2026, the most material movement came from Indica Pre Ground (28g) rising 21.4% while Sativa Pre Ground (28g) increased 13.1%, and Hybrid Pre Ground (28g) added 3.3%, collectively positioning Flower at ranks 6, 8, and 10. Beverage concentration remains high with four of the top ten occupied by lemonade and soda SKUs, led by Strawberry Live Resin Lemonade (100mg THC,12oz) at rank 1 with +13.2% and OG Classic Live Resin Lemonade (100mg THC, 12oz) at rank 2 with +14.8%, while Pomberry Rose Live Resin Lemonade (100mg THC,12oz) held rank 3 with +3.3%. The coexistence of rising pre-ground Flower alongside entrenched Beverage leaders implies Almora Farms is balancing impulse Beverage velocity with value-driven Flower formats to diversify volume sources and protect shelf share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.