Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Lagunitas is stocked at 157 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Francisco, Santa Rosa, San Diego, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

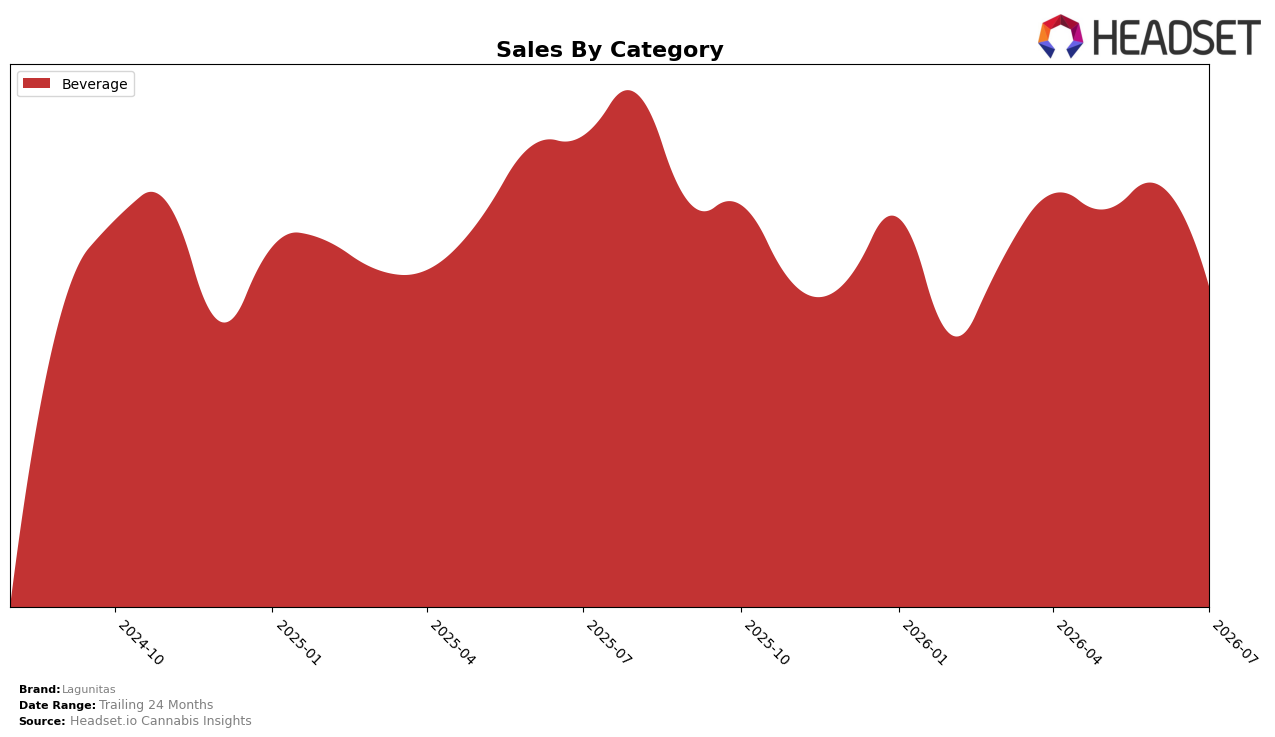

Lagunitas concentrated 100.0% of July 2026 sales in Beverage, with category sales down 26.7% year over year and 19.7% month over month while average price fell 9.0% YoY; within California Beverage, the brand sat at rank 9 during July 2026. With average price at $10.90 alongside a 26.7% YoY sales contraction and a 19.7% MoM pullback, the single-category exposure amplifies volatility, implying that the current mix limits buffer against category downdrafts and signals reliance on price architecture to stabilize volume.

The all-in Beverage focus in July 2026, coupled with a 9-position placement at rank 9 and a 26.7% YoY decline against a 19.7% MoM slide, indicates that Lagunitas is more sensitive to short-term category softness than peers that diversify, and the 9.0% YoY price reduction suggests a tactical move to defend share rather than expand margin. This pattern implies the brand’s positioning is skewed toward volume preservation within California Beverage, where maintaining visibility at rank 9 may require continued price agility and potentially a broadened portfolio to dilute single-category risk.

Competitive Landscape

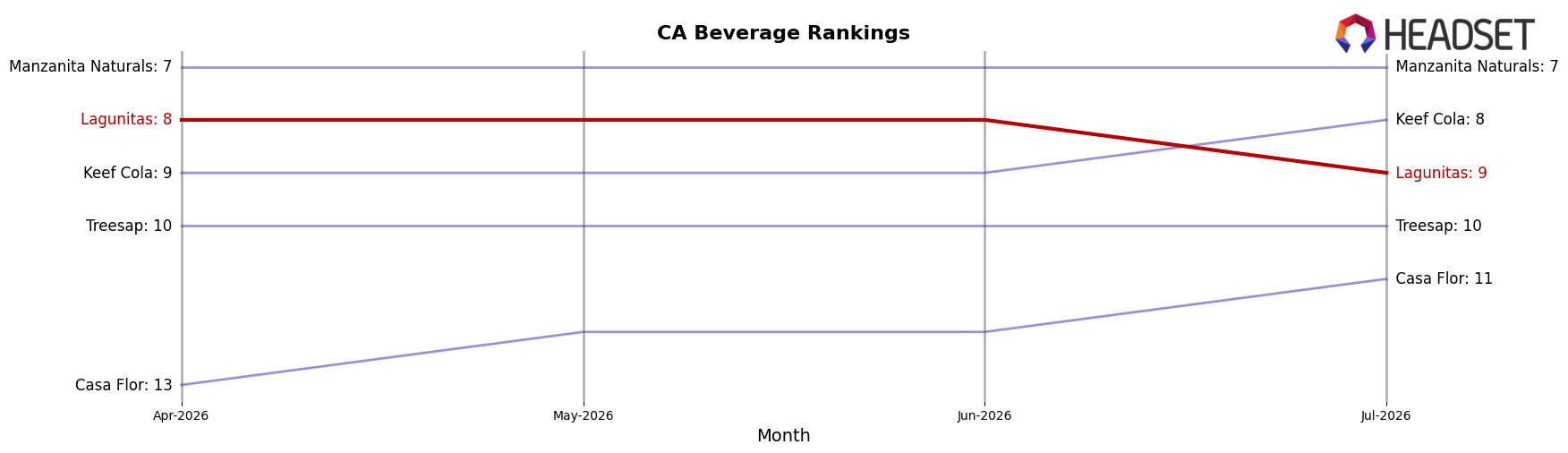

Lagunitas sits at #9 in CA Beverage in July 2026, slipping 1 rank position year over year from #8, and holding flat versus three months ago at #8 to #9, while its peak of #7 in September 2025 now looks further away. Competitive pressure intensified as Almora Farms climbed from #5 to #4 while posting a 52.8% YoY sales gain, and CANN Social Tonics advanced from #7 to #5 alongside a 65.0% YoY sales increase; meanwhile category leaders St Ides held #1 with 17.2% YoY growth and Uncle Arnie's maintained #2 with 33.5% YoY growth, indicating Lagunitas’ -1 rank change is being outpaced by faster risers. The pattern implies Lagunitas’ trajectory—down 1 place YoY and unchanged quarter-on-quarter—risks further share erosion unless it counters competitors gaining 1–2 rank positions with 17%–65% YoY growth.

Notable Products

Lagunitas’s steepest drop came from Hi-Fi Sessions - CBD/THC 1:1 Hoppy Balance Infused Sparkling Water (5mg CBD, 5mg THC, 12oz), down 62.4% month over month while sitting outside the top five at rank 7, as the 10-Pack of Hoppy Chill fell 43.6% to rank 6, indicating multipacks and CBD-blended formats are losing traction relative to singles. At the same time, Hi-Fi Sessions - Hoppy Chill Sparkling Water (10mg THC, 12oz, 355ml) jumped 36.3% to rank 2 and Hi-Fi Sessions - Cloudberry Sparkling Water (10mg THC, 12oz, 355ml) rose 32.3% to rank 3, while the lead SKU HiFi Sessions - Mango Sparkling Water (10mg THC, 12oz, 355ml) slid 27.2% but still held rank 1, pointing to momentum consolidating in core 10mg singles rather than higher-count packs. Four of the top ten are 4-Pack or 10-Pack variants, yet two of those packs declined between 6.4% and 43.6% even as the HiFi Sessions - Mango Sparkling Water 4-Pack (40mg, 12oz, 355ml) grew 40.5%, implying a mixed read on value sizing where only flavor-led packs keep pace.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.