Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

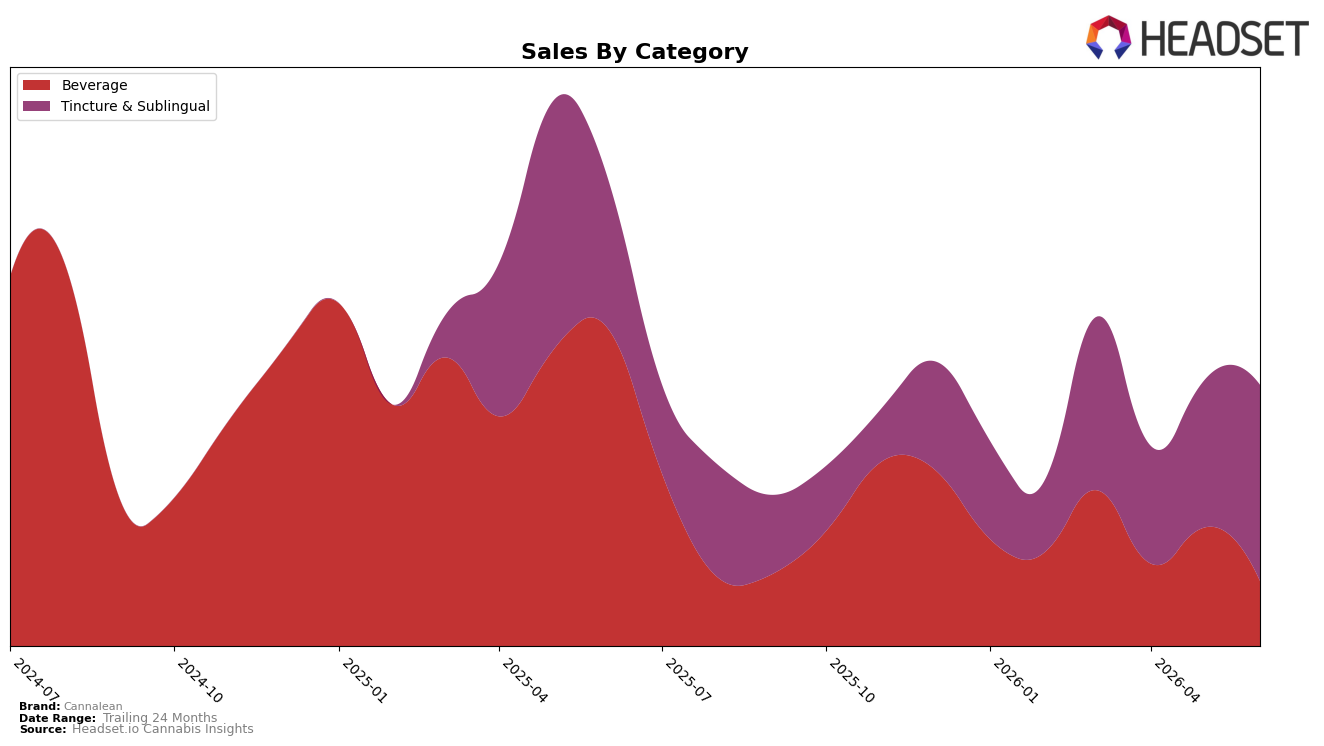

Cannalean’s category mix in June 2026 skewed heavily toward Tincture & Sublingual at 75.1% share, up 32.97% month over month and 31.40% year over year, while Beverage fell to 24.9% share with a 45.14% month-over-month decline and a 79.48% year-over-year drop. Despite total brand sales being down 44.03% year over year, the Tincture & Sublingual rise and a category rank of 18 in California indicate the portfolio is consolidating into a narrower core, and the 8.76% decline in average price alongside a $23.26 current ticket implies volume is being defended via price while Beverage contraction releases share to the higher-velocity tincture line.

The shift concentrates Cannalean’s positioning around Tincture & Sublingual, where double‑digit month-over-month growth of 32.97% and a 31.40% year-over-year gain contrast with Beverage’s 45.14% monthly and 79.48% annual declines, suggesting the brand is pivoting to a category where it can hold rank at 18 rather than distribute effort across weakening Beverage demand. This consolidation implies a strategy to stabilize throughput at lower prices (average price down 8.76% year over year) to recover basket frequency in tinctures, accepting reduced Beverage exposure so the brand competes on depth within a single category rather than breadth across two.

Competitive Landscape

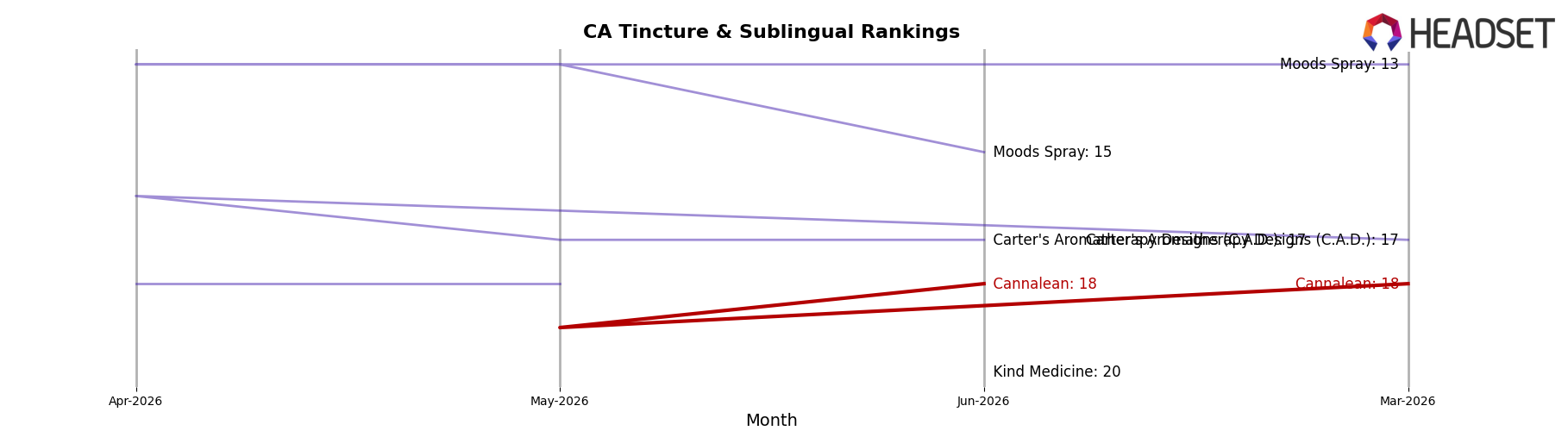

Cannalean sits at rank 18 in CA Tincture & Sublingual for June 2026, improving 1 position from rank 19 year over year, and matching its 3-month position at 18 while reaching a peak rank of 18 in June 2026; this modest upward move contrasts with ABX / AbsoluteXtracts rising from rank 7 to rank 5 and with Papa & Barkley holding rank 1 despite a -9.7% year-over-year sales change. Meanwhile, Yummi Karma stays at rank 2 with a +3.3% sales lift and Care By Design remains at rank 3 despite a -9.6% decline, indicating that Cannalean’s rank stability at 18 is occurring in a tier where leaders are either holding or gaining share despite mixed sales momentum. The pattern implies Cannalean’s incremental rank gain is driven more by relative positioning than category-wide expansion, suggesting limited near-term headroom unless it can outpace mid-tier climbers.

Notable Products

Grape Drink Tincture (1000mg, 60ml) posted the largest month-over-month move at +305.4% to reach rank 1, while Mango Mochi Tincture (1000mg THC, 60ml) fell -19.6% to rank 3, creating a two-rank spread that did not exist in May 2026. Pink Guava Syrup (1000mg THC, 2oz, 60ml) plunged -80.8% and sat at rank 9, and Mango Mochi Syrup (1000mg THC, 60ml, 2oz) dropped -44.2% at rank 6, indicating Beverage SKUs collectively lost share even as Strawberry and Mango variants maintained mid-table positions. With four of the top five in Tincture & Sublingual and Guava Punch Tincture (1000mg THC, 60ml) up +20.1% at rank 2, Tincture weight is concentrating at the top while Syrup volatility deepens. The pattern implies Cannalean is consolidating leadership around higher-potency tinctures and de-emphasizing Syrup formats, a shift likely to steer assortment and pricing toward sublingual use-cases.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.