Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CannaPunch is stocked at 60 licensed dispensaries across Colorado, with the deepest coverage in Denver, Fort Collins, Golden, Pagosa Springs, and Aurora. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

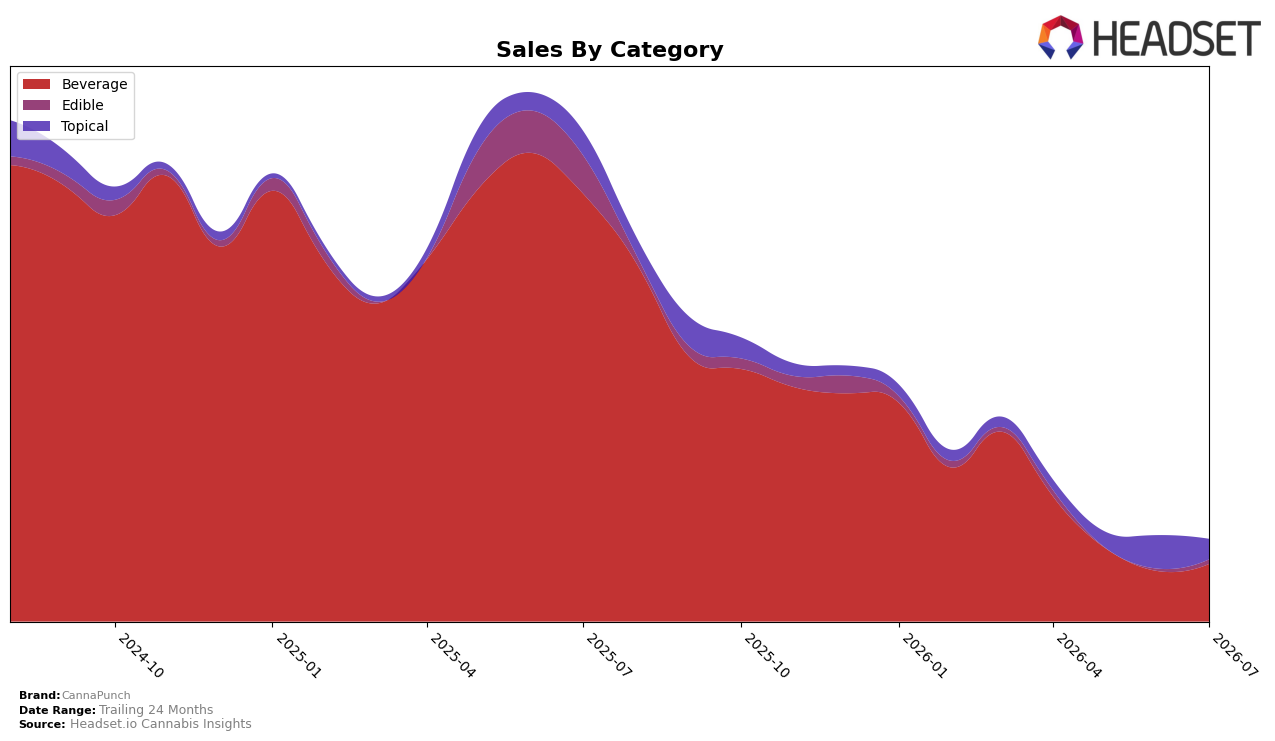

In July 2026, CannaPunch concentrated 70.20% of sales in Beverage, with Beverage down 86.63% year over year but up 14.16% month over month, while Topical held 24.72% share with a 16.30% year-over-year decline and a 39.13% month-over-month drop. Edible represented 5.09% share with a 89.06% year-over-year decline yet a 111.02% month-over-month surge, and the brand-level average price rose 16.62% year over year to $17.07. With Beverage still the anchor and Topical retreating sharply month over month, the pattern implies CannaPunch is leaning back into its Beverage core while experimenting at the edges via Edible volatility.

The mix shift suggests a price-led, Beverage-first posture in Colorado, where the lack of a listed Beverage rank indicates limited shelf traction despite a 14.16% month-over-month Beverage lift and a 86.63% year-over-year Beverage pullback. The Edible spike of 111.02% month over month against a 89.06% year-over-year decline, combined with Topical’s 39.13% month-over-month contraction and 16.30% year-over-year fall, implies tactical reallocation: CannaPunch is prioritizing faster-turn Beverage SKUs while using selective Edible pushes to probe incremental occasions, accepting reduced Topical presence as an offset.

Competitive Landscape

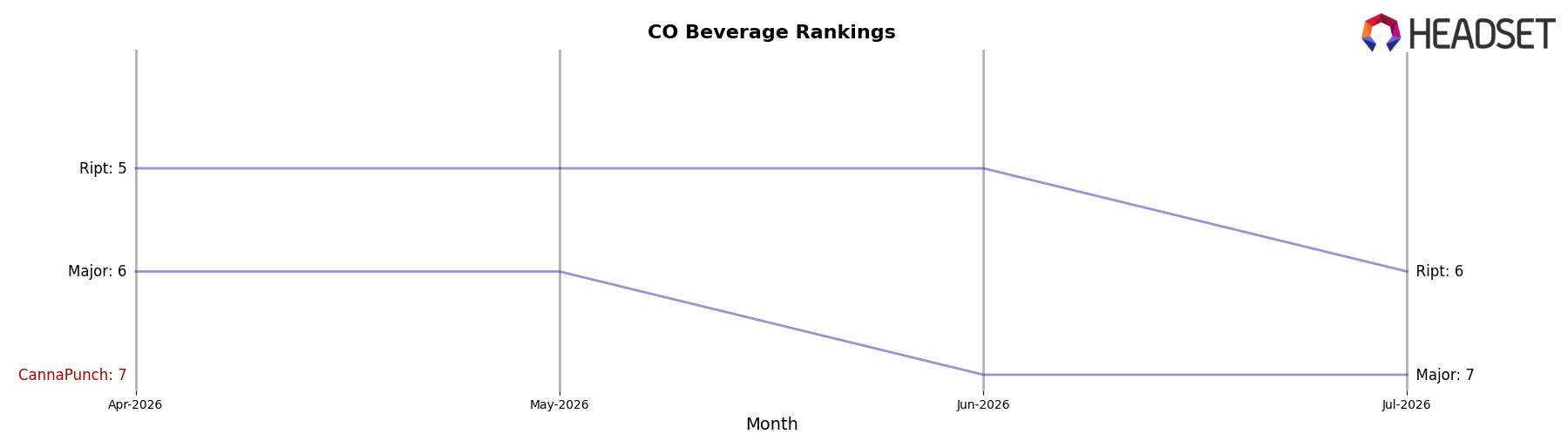

CannaPunch ranks #8 in CO Beverage in July 2026, down 4 positions year over year from #4, and down 1 spot from #7 in April 2026; the brand’s peak was #4 in September 2025, marking a 4-rank slide from that high. Meanwhile, Keef Cola holds #1 while posting a -30.8% YoY sales change, and Ripple (formerly Stillwater Brands) sits at #3 with a -20.0% YoY change, indicating that CannaPunch’s rank erosion amid double-digit declines at leaders implies share is being ceded to mid-pack movers rather than purely to top incumbents.

Notable Products

Blue Raspberry Punch Drink (100mg, 2oz, 59ml) posted the largest month-over-month gain at +171.5% and climbed to rank 5, while Grand Daddy Grape Punch Drink (100mg, 2oz, 59ml) plunged -86.1% to rank 10, indicating a sharp reshuffle within the flavor lineup. Pineapple Papaya Drink (100mg, 2oz, 59ml) jumped +86.9% to rank 2 as Strawberry Melon Punch Drink (100mg, 2oz, 59ml) held rank 1 with +10.2%, and five of the top ten are Beverage SKUs, concentrating momentum in drinks. Offsetting this, CBD:THC 1:1 Wrangler Body Balm (250mg CBD, 250mg THC) slipped -11.6% at rank 3 and Grape Drink (100mg, 2oz, 59ml) fell -13.4% at rank 4, even as Blue Raspberry Gummy (100mg) rose +109.7% at rank 7. The mix implies CannaPunch is pivoting toward Blue Raspberry and tropical Beverage-led velocity, with Edibles as a secondary growth lane and legacy grape profiles de-prioritized.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.