Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ript is stocked at 141 licensed dispensaries across Colorado, with the deepest coverage in Denver, Aurora, Grand Junction, Colorado Springs, and Pueblo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

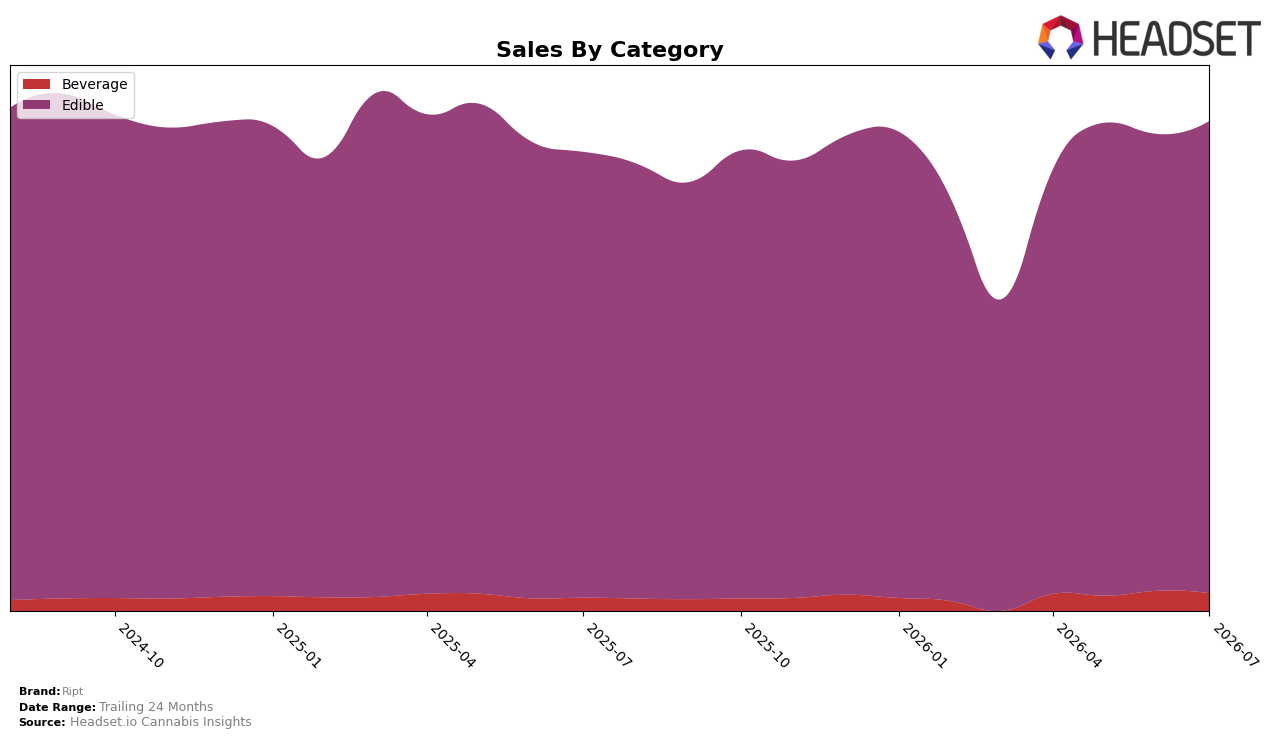

Ript concentrated 96.09% of July 2026 sales in Edible, with Edible up 5.92% year over year and 3.39% month over month, while Beverage held 3.91% share with a 29.95% year-over-year gain but an 11.34% month-over-month decline. Average price fell 11.86% year over year to $7.15, alongside brand sales up 6.69% year over year and down 4.48% over 24 months, and the Edible rank in Colorado sat at 4. The mix indicates a price-led volume strategy anchored in Edible that is maintaining annual growth while near-term Beverage volatility limits diversification.

With a 96.09% Edible skew and a rank of 4 in Colorado Edibles, the brand’s positioning rests on scaling core Edible volumes rather than broadening category breadth, as the 3.39% month-over-month Edible lift offsets an 11.34% Beverage pullback. The 29.95% year-over-year Beverage rise paired with a 3.91% share suggests a testing lane rather than a pillar, and the 11.86% price decline versus 6.69% sales growth implies competitive share defense via affordability that could cap premium trade-up unless accompanied by product tiering.

Competitive Landscape

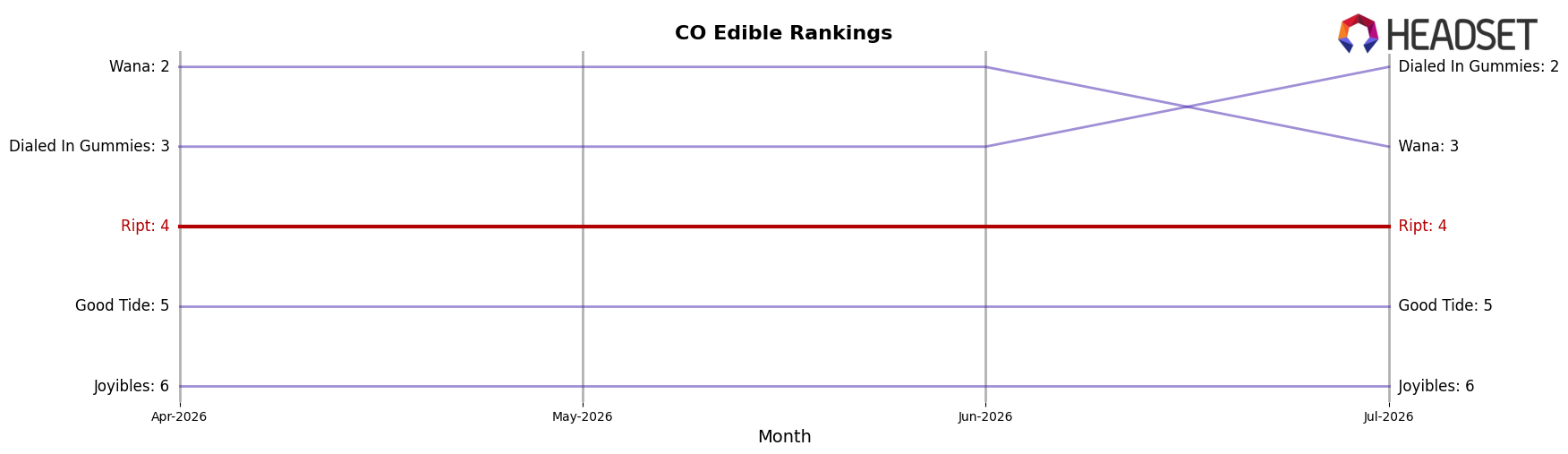

Ript sits at rank #4 in CO Edible in July 2026, unchanged year over year from #4, with its three-month position also holding at #4; meanwhile, Wyld stayed #1 while its sales fell 24.4% year over year and Wana slipped from #2 to #3 alongside a 16.2% sales decline. In contrast, Dialed In Gummies climbed from #3 to #2 with a 15.8% year-over-year sales increase while Good Tide held at #5 with a 14.4% decline, indicating Ript’s static #4 rank coincides with competitor churn above and stability below. The pattern implies that Ript’s flat rank amid leadership contraction and a challenger’s upward move signals a holding pattern that could tip either upward if it captures share from declining leaders or downward if the #2 challenger’s momentum extends.

Notable Products

Sour Pucked Up Peach Gummies 10-Pack (100mg) posted the steepest decline in July 2026 at -23.2% and slid to rank 10, while Quick - Wild Cherry Dissolvable Powder 10-Pack (100mg) fell -11.3% at rank 8; in contrast, CBD/CBN/THC 1:1:2 Knockout Punch Gummies 10-Pack (50mg CBD, 50mg CBN, 100mg THC) rose 17.4% to rank 6. Blazed Blue Raz Gummies 10-Pack (100mg) contracted -50.8% yet held rank 1, and Faded Fruit Punch Gummies 10-Pack (100mg) dipped -2.2% at rank 2; seven of the top ten SKUs are Edibles, concentrating mix in a single category. Baked Apple Gummies 10-Pack (100mg) gained 17.2% at rank 3 alongside a modest 1.4% lift for Plus - CBD/CBG/THC 1:1:1 Strawberry Fieldtrip Gummies 10-Pack (100mg CBD, 100mg CBG, 100mg THC) at rank 9, while Wild Cherry Gummies 10-Pack (100mg) declined -7.4% at rank 7; the category tilt implies Ript is leaning into Edibles despite volatility at the very top. The contrasting surge in functional multi-cannabinoid SKUs and pullback in a leading legacy flavor suggests a pivot toward differentiated formulations rather than flavor-led bets, even as one flagship still generates $189,247.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.