Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Dialed In Gummies is stocked at 696 licensed dispensaries across Colorado, Missouri, and 4 other states, 302 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Aurora, Boulder, and Longmont. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

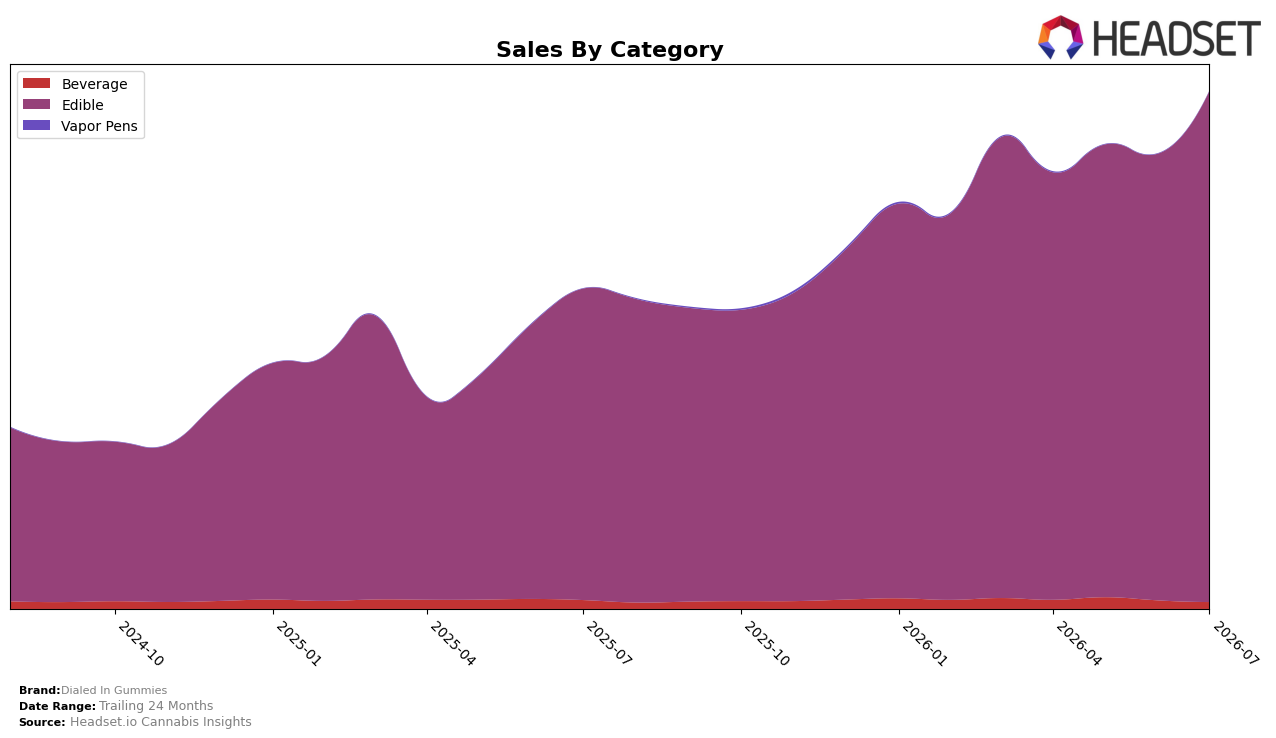

In July 2026, Dialed In Gummies concentrated 98.75% of sales in Edible, with Beverage at 1.24% and Vapor Pens at 0.01%, signaling tighter category focus as Edible grew 64.20% year over year and 14.43% month over month while Beverage fell 23.66% YoY and 20.80% MoM. The brand’s overall sales rose 61.90% YoY against a 6.54% YoY decline in average price, indicating volume-led gains within Edible where average prices sit at $21.03. Edible’s dominance coincides with a rank of #2 in Edible in Colorado, while Vapor Pens contracted 43.07% MoM off a negligible 0.01% share, implying deliberate pruning of peripheral bets to reinforce the Edible core.

The mix shift implies strategic pricing and assortment that trade lower average price for higher unit throughput, as evidenced by a 6.54% YoY price decrease alongside 14.43% MoM and 64.20% YoY Edible growth. With 98.75% share anchored in Edible and a #2 category rank in Colorado, the brand is positioned as a scale-first Edible specialist, while the 20.80% MoM and 23.66% YoY declines in Beverage indicate deprioritization of adjacency categories. The pattern points to sustained share defense via velocity in Edible and selective retrenchment in non-core lines to preserve price-to-volume balance.

Competitive Landscape

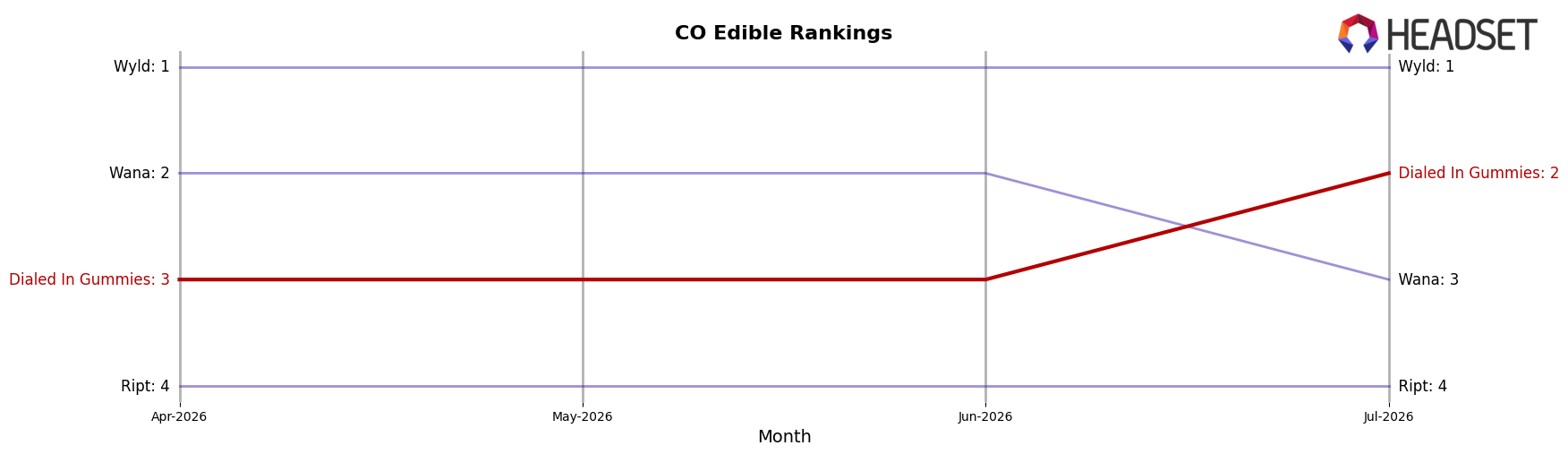

Dialed In Gummies holds rank #2 in CO Edible in July 2026, up 1 place from #3 year over year, and up 1 place from #3 in April 2026, while peaking at #2 in July 2026; in contrast, Wyld stayed flat at #1 year over year as its sales fell 24.4% YoY, and Wana slipped from #2 to #3 alongside a 16.2% YoY sales decline, indicating Dialed In Gummies is advancing in rank against incumbents that are contracting and is positioned to challenge the top spot if these trajectories persist.

Notable Products

Hybrid Live Rosin Gummies 10-Pack (100mg) posted the steepest decline in July 2026 at -7.9% and slid to rank 7, while CBD/THC/CBN 1:1:1 Acai Berry Sleep Rosin Gummies 10-Pack (100mg CBD, 100mg THC, 100mg CBN) rose 18.1% to hold rank 1, indicating a tilt toward function-led formulations over generic hybrids. CBG/THC 2:1 Pomegranate Rosin Gummies 10-Pack (200mg CBG, 100mg THC) jumped 48.2% to rank 2 and CBD/THC 5:1 Rocket Berry Live Rosin Relax Gummies 10-Pack (500mg CBD, 100mg THC) climbed 38.8% to rank 3, while Focus - THCV/CBC/THC 1:1:1 Blood Orange Rosin Gummies 20-Pack (100mg THCV, 100mg CBC, 100mg THC) was flat at +0.4% in rank 5, pointing to stronger pull for CBD-anchored ratio SKUs than niche stimulant blends. With all top-ten items in Edible and four in functional sleep/relax or ratio-led families, the mix concentrates demand in targeted effect SKUs, implying Dialed In Gummies is consolidating around benefit-forward gummies rather than flavor-first core hybrids.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.