Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

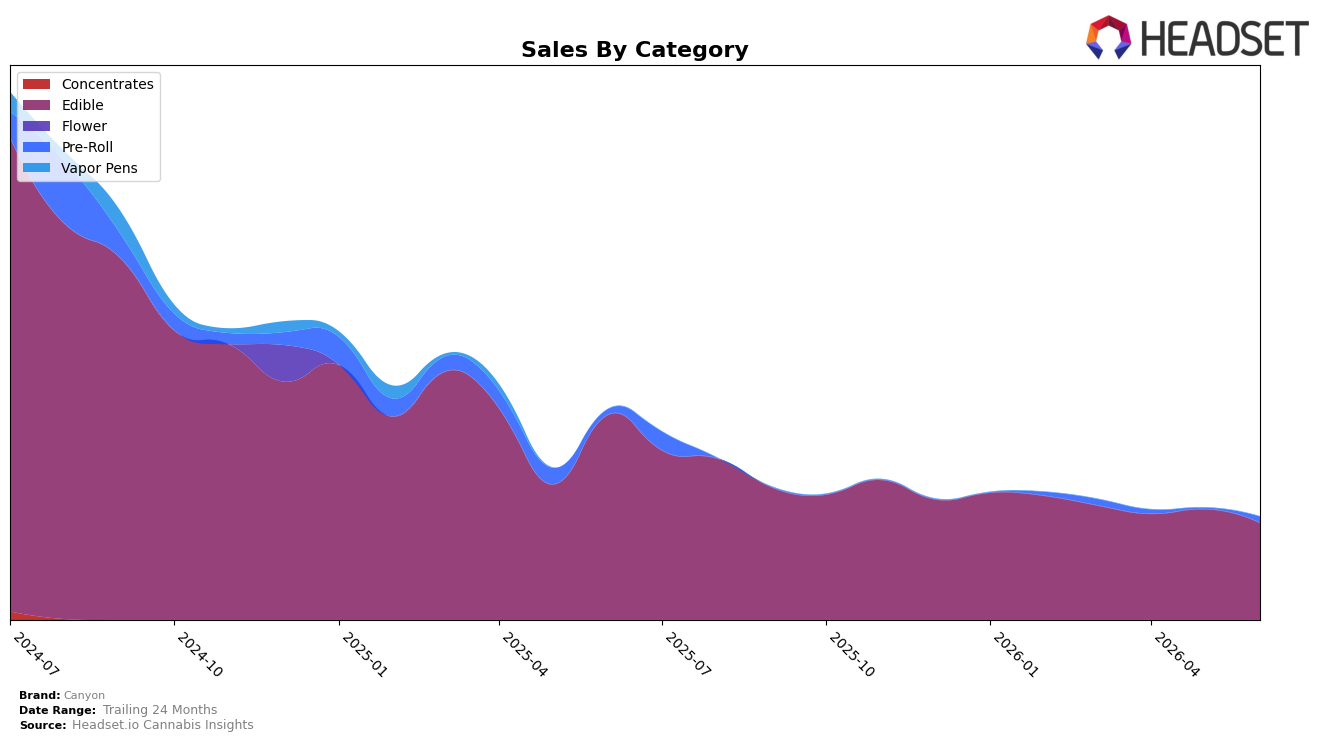

Canyon’s June 2026 mix was concentrated in Edible at 94.41% share while Pre-Roll accounted for 5.59%, a configuration paired with a brand-level year-over-year sales change of -51.34% and a 24-month change of -76.90%. Within categories, Edible declined -52.89% YoY and -12.52% MoM, while Pre-Roll expanded 10.28% YoY and 584.25% MoM, shifting a small but rapidly growing tail against a contracting core; the brand’s average price fell -4.06% YoY to $13.44. In Colorado Edibles, Canyon sat at rank 25, which, combined with a double-digit MoM Edible drop and a Pre-Roll spike, implies that June 2026 performance leaned on a narrowing Edible base with emerging, volatility-driven contribution from Pre-Roll.

The mix shift implies Canyon is over-indexed to a declining Edible segment while testing or reactivating Pre-Roll as a secondary lever, with rank 25 in Colorado Edibles and a -12.52% MoM Edible slide indicating weaker near-term velocity versus category peers and a need to diversify away from a -52.89% YoY Edible contraction. The 584.25% MoM surge and 10.28% YoY growth in Pre-Roll, despite only 5.59% share, signals early elasticity where small absolute gains can offset part of the Edible drag, and the -4.06% YoY price decrease alongside a $13.44 average suggests price is being used more defensively than expansively; together, these dynamics imply Canyon’s positioning is shifting from an Edible-centric strategy toward a broader portfolio hedge that relies on maintaining Edible presence while scaling Pre-Roll to stabilize share and rank.

Competitive Landscape

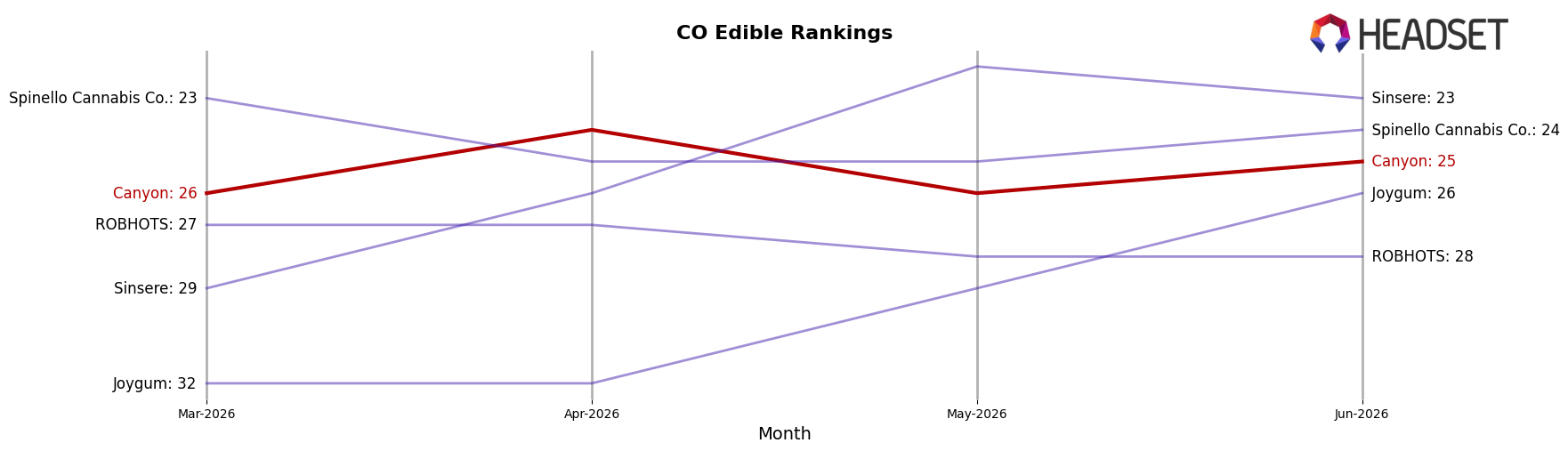

Canyon sits at rank #25 in Colorado Edible for June 2026, improving 4 positions from #29 year over year, yet slipping 1 spot from #26 in March 2026; its peak at #19 in July 2024 marks a 6-rank drop from that high. Meanwhile, Wyld held #1 with a -16.6% year-over-year sales change while staying flat at the top, and Dialed In Gummies remained #3 with a 3.7% year-over-year sales increase, indicating Canyon’s modest rank lift is occurring as the category’s leader softens and a challenger grows. The pattern implies Canyon’s trajectory is stabilizing rather than accelerating, with incremental gains constrained by entrenched leaders and rising mid-tier pressure.

Notable Products

Lick It - Orange Raspberry Lollipop (10mg) posted the month’s outsized move with a 664.3% MoM surge to rank 5, while Suck It - Sativa Strawberry Lemonade Hard Candy 40-Pack (100mg) climbed 52.6% to rank 2. In contrast, Chew It - Blue Raspberry Rosin Gummies 20-Pack (100mg) fell 57.1% as Chew It - CBD/THC 1:1 Sour Lemonade Gummies 40-Pack (100mg CBD, 100mg THC) slid 37.8% but still held rank 1 and the brand’s top dollar contribution at $5,616. With eight of the top ten in Edibles and multiple Chew It SKUs declining 26.1% to 57.1% while Suck It and Lick It formats rose triple digits, the mix implies a pivot toward value-sized or novelty single-dose candy driving trial over legacy gummy multipacks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.