Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Crops is stocked at 147 licensed dispensaries across Illinois, New Jersey, and Utah, 76 of them in Illinois, with the deepest coverage in Chicago, East Peoria, Springfield, Peoria, and East Dubuque. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

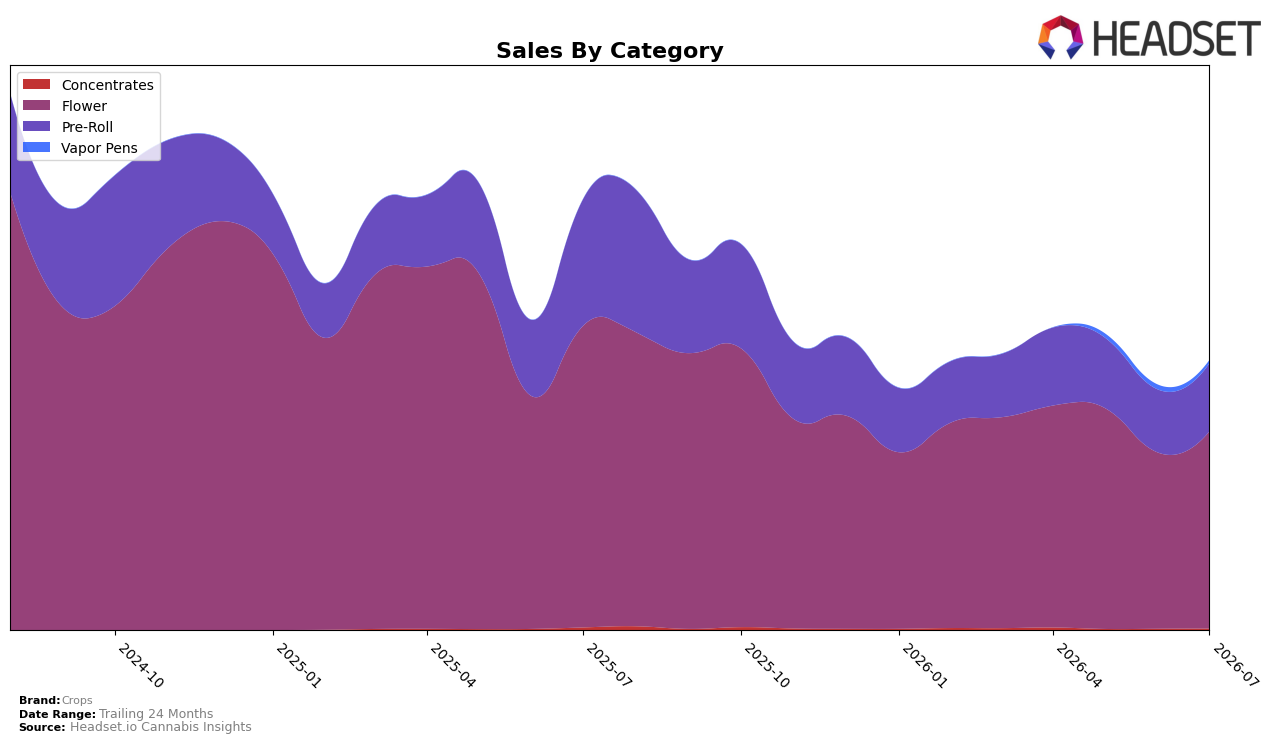

Crops concentrated 73.19% of July 2026 sales in Flower, up 11.93% month over month even as Flower declined 34.68% year over year; Pre-Roll held 25.18% share with an 8.11% MoM uptick but a 46.42% YoY decline, while Vapor Pens slipped 34.95% MoM to 1.09% share and Concentrates rose 14.55% MoM despite a 44.14% YoY drop. Overall brand sales fell 37.50% year over year and average price edged down 1.10%, and within the Flower category Crops ranked 11 in New Jersey; the pattern implies Crops is leaning into Flower-led volume recovery month over month while the category mix remains exposed to year-over-year contraction.

The mix skews toward higher-ticket inhalables (42.38 average price in Flower and 58.34 in Concentrates) while Pre-Roll contributes lower-price velocity at 16.14, and the MoM rebound in Flower (+11.93%) paired with Pre-Roll (+8.11%) suggests near-term share defense via core inhalables despite Vapor Pens’ drag (-34.95% MoM). With a 73.19% Flower dependence and an 11th-place rank in New Jersey, the implication is that Crops must either expand beyond Flower and Pre-Roll, or drive trading up within those segments, because the double-digit YoY declines in Flower (-34.68%) and Pre-Roll (-46.42%) indicate the current mix is amplifying category downtrends rather than offsetting them.

Competitive Landscape

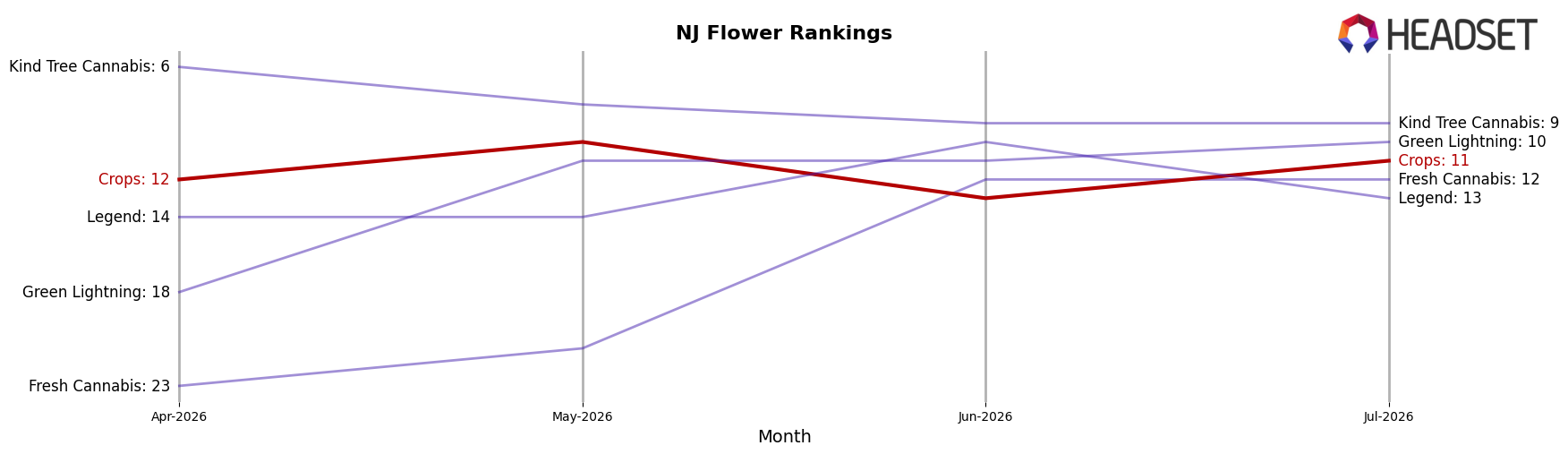

Crops ranks #11 in New Jersey Flower in July 2026, down 3 positions year over year from #8 and up 1 place versus April 2026’s #12, signaling a mild recovery after a longer slide from a peak at #4 in April 2025. Competitively, Ozone sits at #1 after a year-over-year rise from #2 while its sales fell 13.1%, and Find. climbed from #10 to #2 with 129.0% sales growth, indicating that Crops’ rank erosion coincided with share being absorbed by faster-moving rivals even as the category leader contracted. With Crops losing 3 rank positions year over year but inching up 1 spot over three months, the trajectory implies stabilization without momentum against competitors accelerating up the table.

Notable Products

Super Boof Ground Shake (14g) posted the standout surge in July 2026 with +164% month over month, vaulting into rank 3, while Jon Woo Pre-Roll (1g) slid 39% MoM yet still held rank 1; this split implies volume is consolidating into value Flower even as a legacy Pre-Roll anchor softens. Rainbow Runtz Pre-Roll (1g) jumped 64% MoM into rank 4, and four of the top ten are Pre-Roll SKUs versus five in Flower, indicating a tilt toward mixed-format demand where Flower’s higher growth rates outpace Pre-Roll’s rank stability; Super Boof Ground Shake (14g) alone accounts for $60,101, reinforcing the shift toward larger-size value packs. The pattern implies Crops is pivoting toward scale-oriented Flower formats that can win share through price-pack architecture while maintaining Pre-Roll visibility at the top of the chart.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.