Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

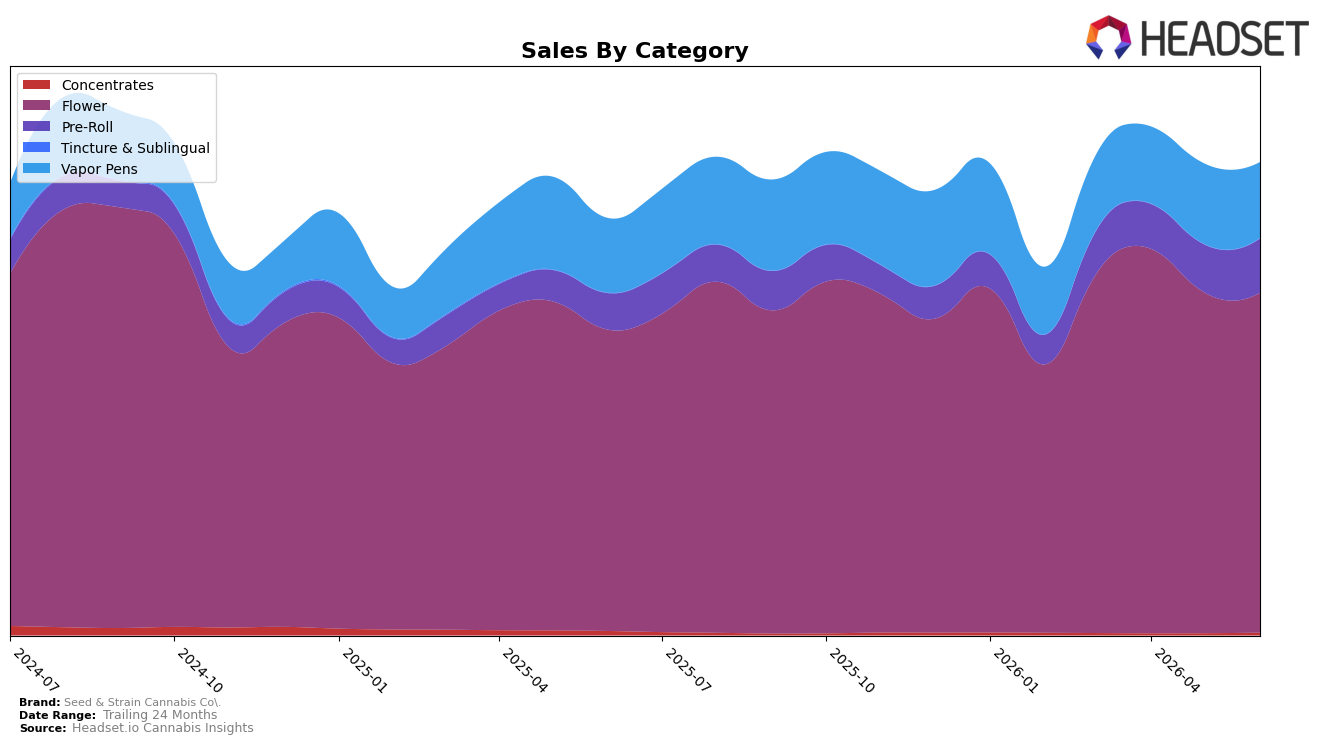

In June 2026, Seed & Strain Cannabis Co. concentrated 72.01% of sales in Flower with year-over-year growth of 12.85% but a month-over-month slip of 0.19%, while Pre-Roll climbed to 11.44% share on 49.23% YoY and 13.29% MoM growth; Vapor Pens held 16.02% share with 1.72% YoY and a 5.79% MoM decline, and Concentrates remained a 0.52% niche despite a 27.04% MoM rebound and a 40.90% YoY drop. With Flower ranked 1 in Colorado and average price down 11.48% YoY to $23.17, the mix points to a price-led volume strategy anchored in Flower dominance and a tactical tilt toward faster-turning Pre-Rolls.

The shift toward Pre-Roll growth at 13.29% MoM alongside a 5.79% MoM pullback in Vapor Pens implies merchandising and promotional emphasis favoring value-forward inhalables, reinforced by an 11.48% YoY price reduction that widens reach without eroding Flower’s leadership. Given 13.49% brand-level YoY growth and 34.28% growth over 24 months, sustaining the Flower lead while nurturing Pre-Rolls as the second engine suggests a positioning built on everyday-price accessibility and basket-entry formats, with Concentrates’ 27.04% MoM uptick serving as a test bed rather than a scale priority.

Competitive Landscape

Seed & Strain Cannabis Co. sits at rank #1 in CO Flower in June 2026 after improving 1 position year over year from #2, and it sustained a top-spot streak versus March 2026 where it also held #1, indicating peak rank persistence. In the same month, Triple Seven (777) is #2 after rising from #3 year over year while posting a 32.8% YoY sales increase, whereas Good Chemistry Nurseries sits at #3 after falling from #1 year over year with a 2.8% YoY sales decline; further back, Natty Rems advanced to #5 from #28 with 221.0% YoY growth, outpacing Green Dot Labs at #4 and 4.1% YoY growth. The pattern implies Seed & Strain Cannabis Co.’s #1 rank is being defended against faster-rising challengers, so maintaining share leadership will hinge on converting rank stability into velocity as competitors close gaps with double- and triple-digit YoY growth.

Notable Products

Pink Lemonade Distillate Cartridge (1g) posted the steepest movement in June 2026 with a -18.6% month-over-month slide while holding rank 3, and Cannalope Haze Distillate Cartridge (1g) fell -20.7% at rank 4, indicating pressure within Vapor Pens despite Kiwi Berry Distillate Cartridge (1g) rising +1.7% to rank 1. Vapor Pens account for three of the top five ranks (1, 3, and 4), yet Pre-Rolls occupy ranks 6 through 10 with two 10-packs inside the top 10, signaling a mix shift toward multi-pack and value-driven formats even as a single premium cart drives the top line. Kiwi Berry Distillate Cartridge (1g) led with $167,352 and outperformed the category peers by more than 20 percentage points on MoM basis, while Cherry Pie Distillate Cartridge (1g) grew +14.8% at rank 5, pointing to polarization between a few winning SKUs and broader softness.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.