Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

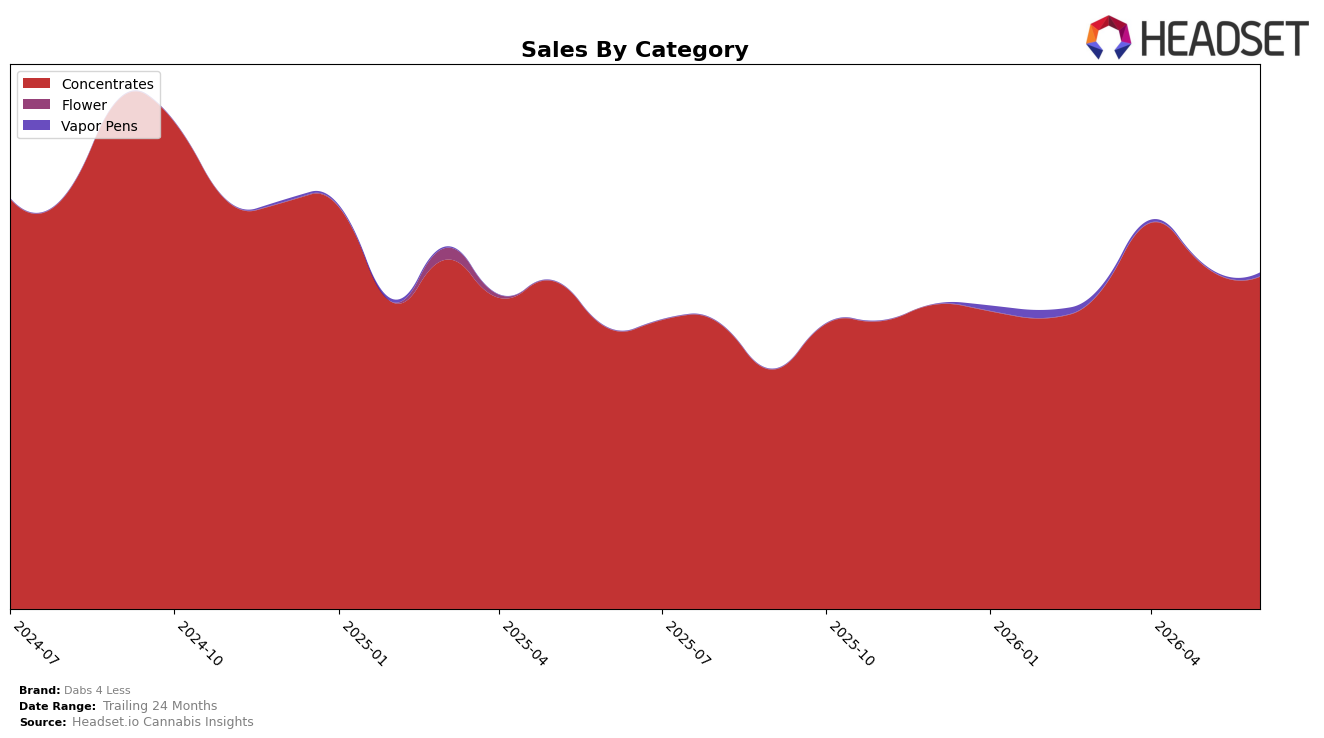

Dabs 4 Less concentrated its June 2026 sales mix in Concentrates at 98.98% share, while Vapor Pens held 1.02%; within those, Concentrates grew 18.43% year over year but slipped 3.05% month over month, and Vapor Pens jumped 388.65% month over month off a small base. The brand’s overall year-over-year sales rose 19.65% even as average price declined 15.45%, and in Washington the brand sat at rank 17 in Concentrates; this combination implies volume-led gains anchored in a single category with early signs of adjacent-category testing that could temper reliance on one segment.

With Concentrates carrying 98.98% share and a month-over-month dip of 3.05% alongside a 388.65% month-over-month surge in Vapor Pens to 1.02% share, the mix shift implies Dabs 4 Less is using lower pricing (average price down 15.45%) to defend rank 17 in Washington Concentrates while probing a small but faster-growing pen position. Given brand sales up 19.65% year over year but down 27.23% over 24 months, the pattern suggests near-term recovery is dependent on sustaining Concentrates volume while selectively scaling Vapor Pens to diversify risk and reduce sensitivity to single-category month-to-month volatility.

Competitive Landscape

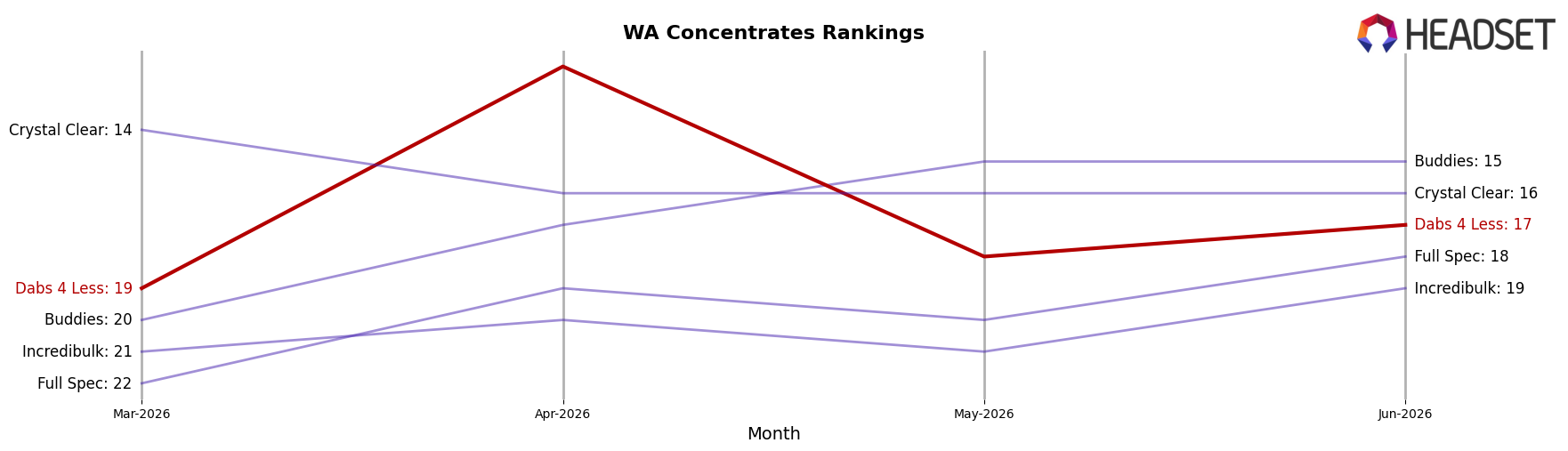

Dabs 4 Less sits at rank #17 in June 2026 in WA Concentrates, a 4-place improvement from #21 year over year and a 2-place slide from #15 in March 2026, with the brand still trailing its peak of #11 reached in September 2024; meanwhile, Constellation Cannabis advanced from #7 to #3 alongside a 44.1% YoY sales increase, and Dabstract moved from #5 to #4 with 23.5% YoY growth, indicating that mid-tier share is consolidating upward while Dabs 4 Less is gaining rank more slowly than faster-rising peers. With category leaders stable at the top—Ooowee remained #1 despite a 6.8% YoY sales decline and Delectable Dabs held #2 with a 1.4% YoY dip—Dabs 4 Less’s YoY climb of 4 ranks but quarter-over-quarter softness of 2 ranks implies a path of incremental recovery that risks being outpaced by competitors accelerating into the top 10.

Notable Products

Gelato 45 BHO Wax (1g) posted the standout movement in June 2026 with a +61% month-over-month surge to rank 5, while Grape Gas Wax (1g) fell -50% to rank 6, signaling a sharp redistribution of demand within the lineup. At the top, Honey Bananas Wax (1g) in rank 1 inched up +3.8% as Sour Diesel BHO Wax (1g) slid -11.6% into rank 2, indicating the lead SKU is steady even as a key runner-up softens. Nine of the top ten are Concentrates, and two Gelato variants appear in the top seven, implying a tilt toward flavor-led waxes with headroom for premiumized Gelato extensions. The pattern implies Dabs 4 Less is consolidating around a few high-momentum Concentrates while pruning or repositioning SKUs with double-digit declines to sustain mix efficiency.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.