Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

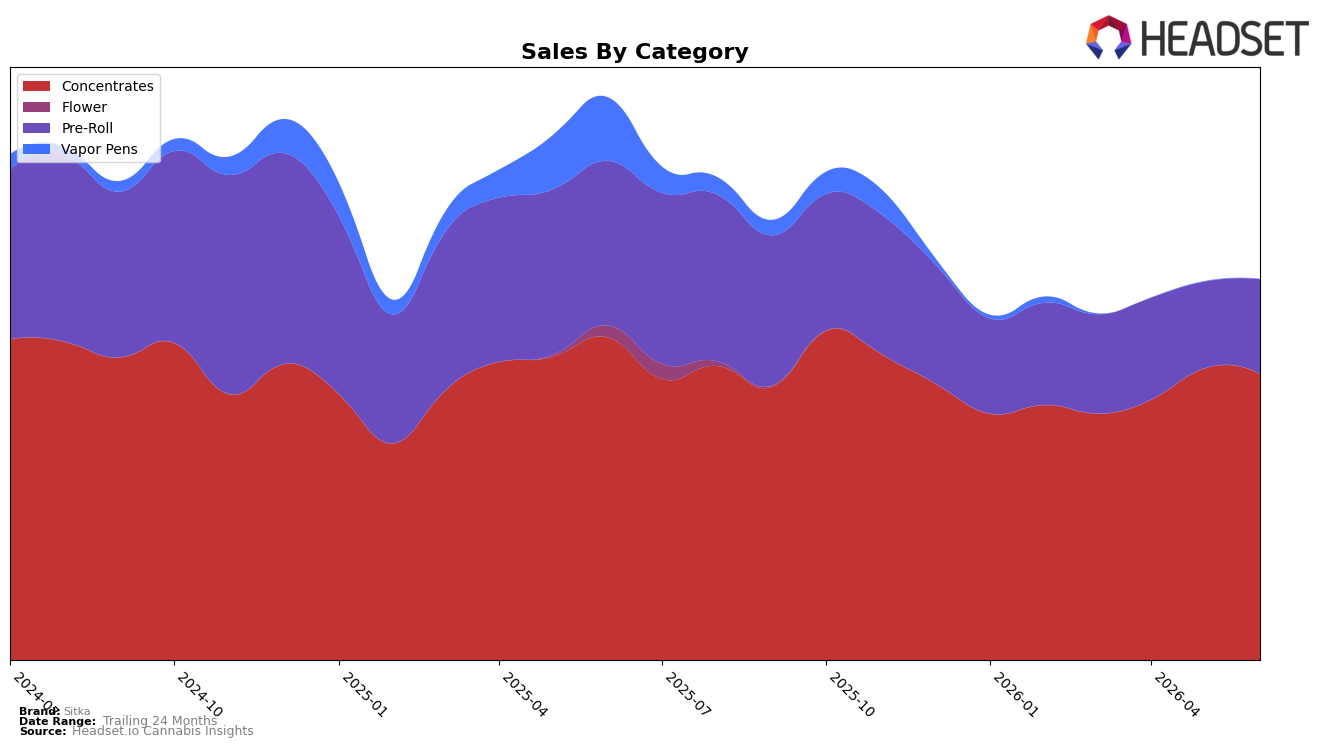

Sitka concentrated its mix in Concentrates at 75.14% share while Pre-Roll accounted for 24.86% in June 2026, with year-over-year declines of 11.37% in Concentrates and 42.47% in Pre-Roll framing an overall brand sales contraction of 32.31%. Month over month, Concentrates dipped 1.97% while Pre-Roll rose 9.51%, and average price fell 8.70% year over year to $17.15, pointing to price pressure alongside a modest Pre-Roll recovery. With Concentrates ranked 25th in Washington, the pattern implies a reliance on a weakening core while a smaller, lower-priced Pre-Roll line is absorbing some demand as price-sensitive customers trade down.

The mix shift suggests Sitka’s positioning skews toward value-seeking consumers: a double-digit year-over-year decline in Concentrates at 11.37% paired with a 42.47% drop in Pre-Roll, but a 9.51% month-over-month lift in Pre-Roll, indicates near-term elasticity where lower price points resonate after an 8.70% brand-wide price decrease. Holding a 75.14% weight in Concentrates while sitting at rank 25 in Washington implies limited headroom without reallocation; the pattern points to a need to either defend Concentrates frequency despite a 1.97% monthly slip or purposefully grow Pre-Roll share from 24.86% as the incremental growth engine.

Competitive Landscape

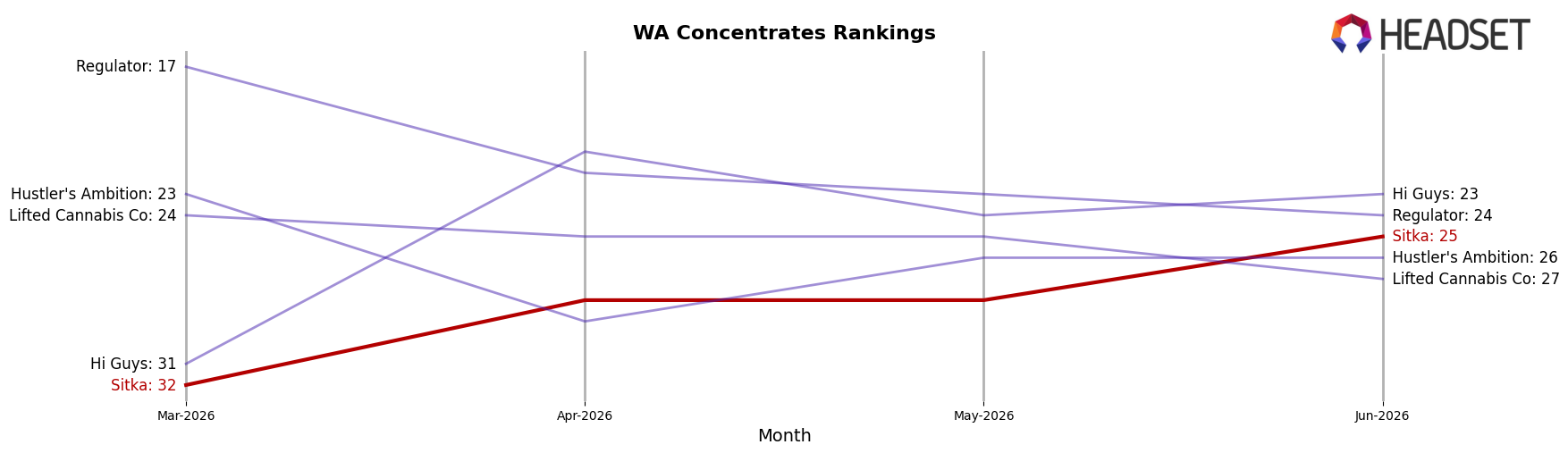

Sitka ranks #25 in Washington Concentrates in June 2026, slipping 2 positions from #23 year over year, but climbing 7 spots from #32 in March 2026; this places the brand 6 ranks below its peak of #19 from August 2025 and 24 places behind category leader Ooowee, which held #1 both this year and last while its sales declined 6.8%. Meanwhile, Constellation Cannabis advanced from #7 to #3 with 44.1% YoY sales growth, and Dabstract improved from #5 to #4 alongside 23.5% YoY growth, underscoring that upward rank mobility is occurring among rising mid‑tier rivals even as top‑ranked incumbents contract slightly. The pattern implies Sitka’s recent quarter-on-quarter rebound is recovery-driven rather than momentum-driven, and the two-position YoY decline suggests share is being reallocated toward faster‑growing competitors unless Sitka converts the short-term rank lift into sustained gains.

Notable Products

Classic - Cascade Cream Hash (1g) posted the steepest decline at -25.7% and slid to rank 5, while Classic - Lebanese Red Hash (1g) grew 9.0% to hold rank 1; this split suggests consumer preference is consolidating around legacy Lebanese profiles over newer variants. Lebanese Red Dry Sift Hash (1g) advanced 9.8% at rank 2, and Lebanese Gold Hash (1g) added 6.1% at rank 3, meaning three of the top five are Concentrates from the Lebanese family, pointing to a concentrated demand footprint. On the Pre-Roll side, Cascade Cream Infused Pre-Roll (1g) jumped 40.4% at rank 7 and the Lebanese Red Hash Infused Pre-Roll 5-Pack (2g) rose 34.0% at rank 6, while Classic - Lebanese Gold Hash Infused Pre-Roll 5-Pack (2g) fell -28.5% at rank 8, indicating format experiments are volatile around a stable flavor core. Overall, with Concentrates holding ranks 1–3 and Pre-Rolls scattered across ranks 4–10 despite mixed MoM swings, Sitka’s product mix implies near-term commercial focus should favor Lebanese Concentrates as anchor SKUs while using selective Pre-Roll extensions to test price-pack and format without diluting the core.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.