Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Dabtastic is stocked at 45 licensed dispensaries across Washington, with the deepest coverage in Spokane, Tacoma, Seattle, Olympia, and Vancouver. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

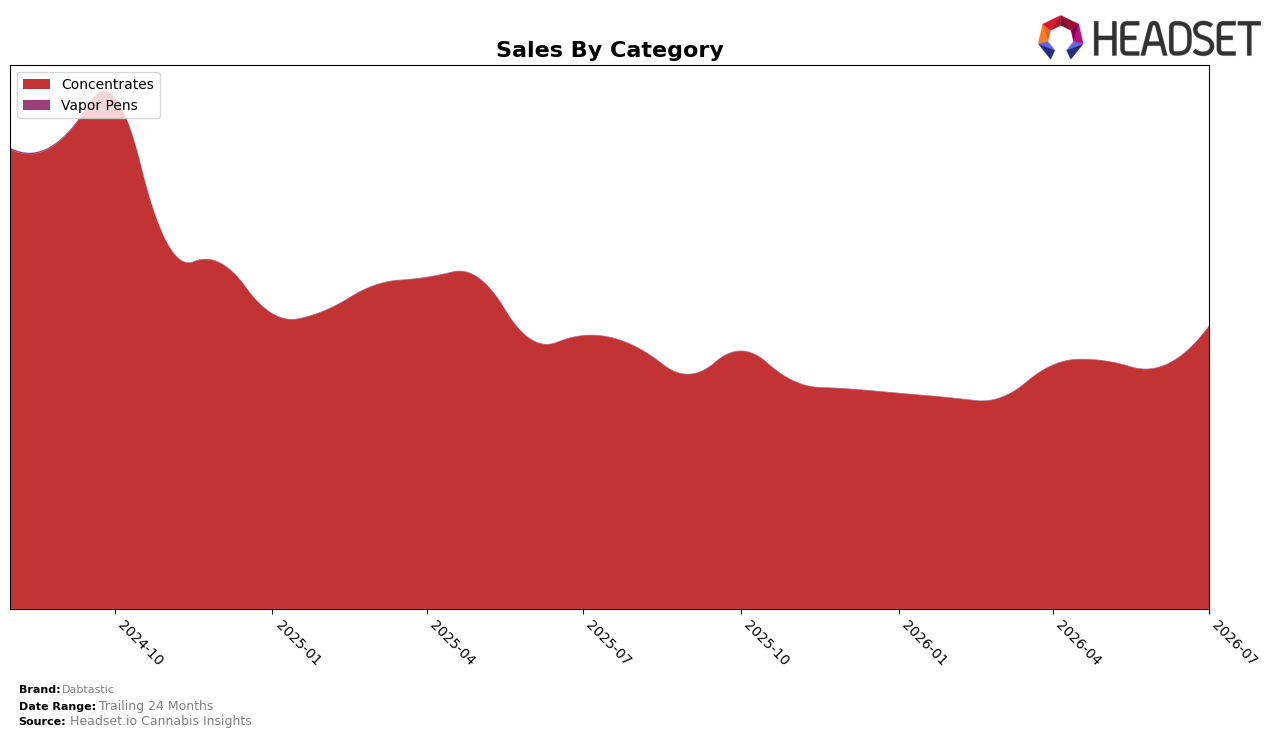

Dabtastic operated as a single-category brand in July 2026, with Concentrates accounting for 100.0% of sales and rising 3.57% year over year and 17.29% month over month; the average item price increased 6.93% YoY while total brand sales also climbed 3.57% YoY. In Washington, the brand sat at rank 11 within Concentrates, a position that suggests room to gain share given the double-digit MoM velocity; the 24‑month sales change of -25.45% contrasts with current MoM momentum of 17.29%. The pattern implies Dabtastic is consolidating around a single category and leveraging recent demand spikes to stabilize after a two‑year contraction.

The combination of a 100.0% Concentrates mix and a 6.93% YoY price increase alongside a 3.57% YoY sales lift indicates the brand is leaning on price to support revenue while volume lags that price change, and the 17.29% MoM growth points to short‑term elasticity within the segment. Holding rank 11 in Washington while posting a 3.57% YoY sales gain suggests mid‑tier positioning where incremental share wins depend on sustaining MoM demand without further price‑led growth; the -25.45% 24‑month trend underscores the need for mix or format extensions if Concentrates momentum decelerates. The implication is that Dabtastic’s near‑term path to climb from rank 11 relies on converting July 2026’s MoM surge into repeat volume rather than additional price moves, given price already outpaced sales growth by 3.36 percentage points.

Competitive Landscape

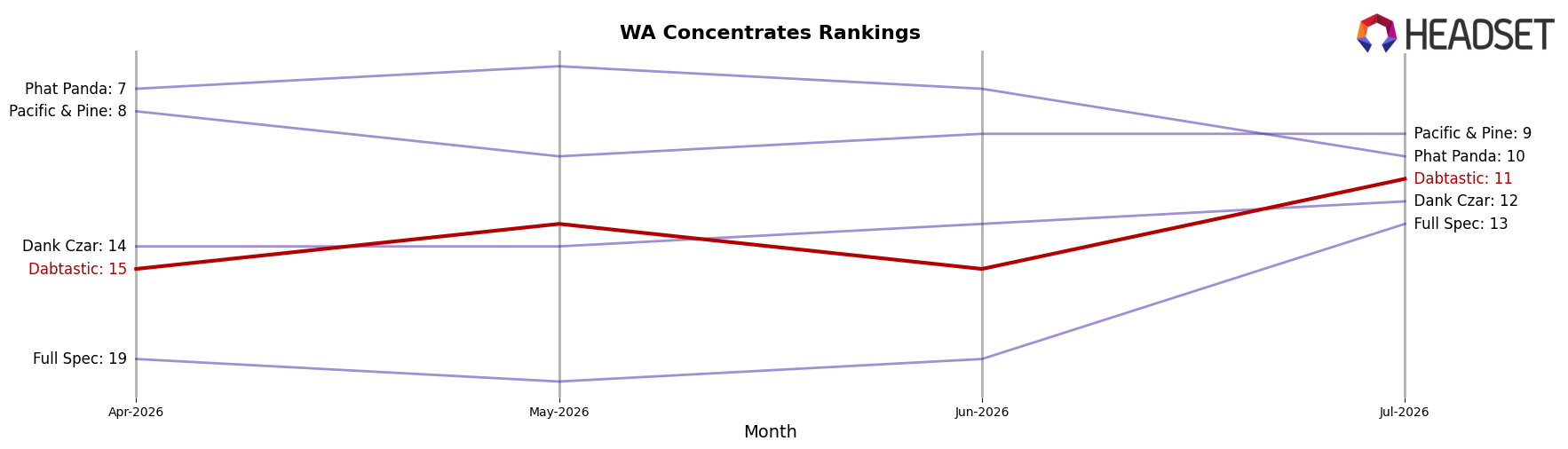

Dabtastic is ranked #11 in Washington Concentrates in July 2026, improving 1 rank position year over year from #12, and up 4 spots versus April 2026 when it sat at #15; despite that upward drift from a three-month trough, the brand remains below its peak #7 from October 2024, indicating recovery but not a return to prior competitiveness. In contrast, Ooowee held #1 with a -6.9% year-over-year sales change, while Constellation Cannabis advanced from #7 to #4 with an 18.9% year-over-year gain, and Dabstract rose from #4 to #3 with 5.2% growth, pointing to share consolidation among higher-ranked competitors. The pattern implies Dabtastic’s modest rank lift is cyclical catch-up rather than structural share capture, and without a step-change that closes the gap to top-5 contenders its July 2026 trajectory suggests stabilization near the low teens rather than reattainment of the October 2024 peak.

Notable Products

Pink Certz Wax (1g) posted the steepest decline in July 2026, dropping 18.4% while sitting at rank 10, and Goofiez Sugar Wax (1g) fell 11.4% at rank 9; this simultaneous contraction at the lower end indicates weakening depth in single‑gram offerings even as upper‑tier items gain momentum. At the top, Sativa Wax 3-Pack (3g) rose 25.4% to rank 1 and Indica Wax 3-Pack (3g) climbed 25.1% at rank 2, together pointing to multi-pack wax leading demand concentration, with four of the top ten being 3‑pack wax SKUs; one raw figure applies here as Sativa Wax 3-Pack (3g) reached $69,912. Hybrid Wax 3-Pack (3g) advanced 18.2% at rank 4 while First Class Funk Wax (1g) slipped 7.2% at rank 6, a split that suggests trade-up from single-gram to value-oriented bundles. The pattern implies Dabtastic is skewing toward volume-driven 3‑pack formats in Concentrates, signaling a portfolio tilt toward bundle value over breadth in 1g varietals.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.