Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Tasty Terps is stocked at 107 licensed dispensaries across Washington and California, 106 of them in Washington, with the deepest coverage in Tacoma, Spokane, Everett, Olympia, and Lacey. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

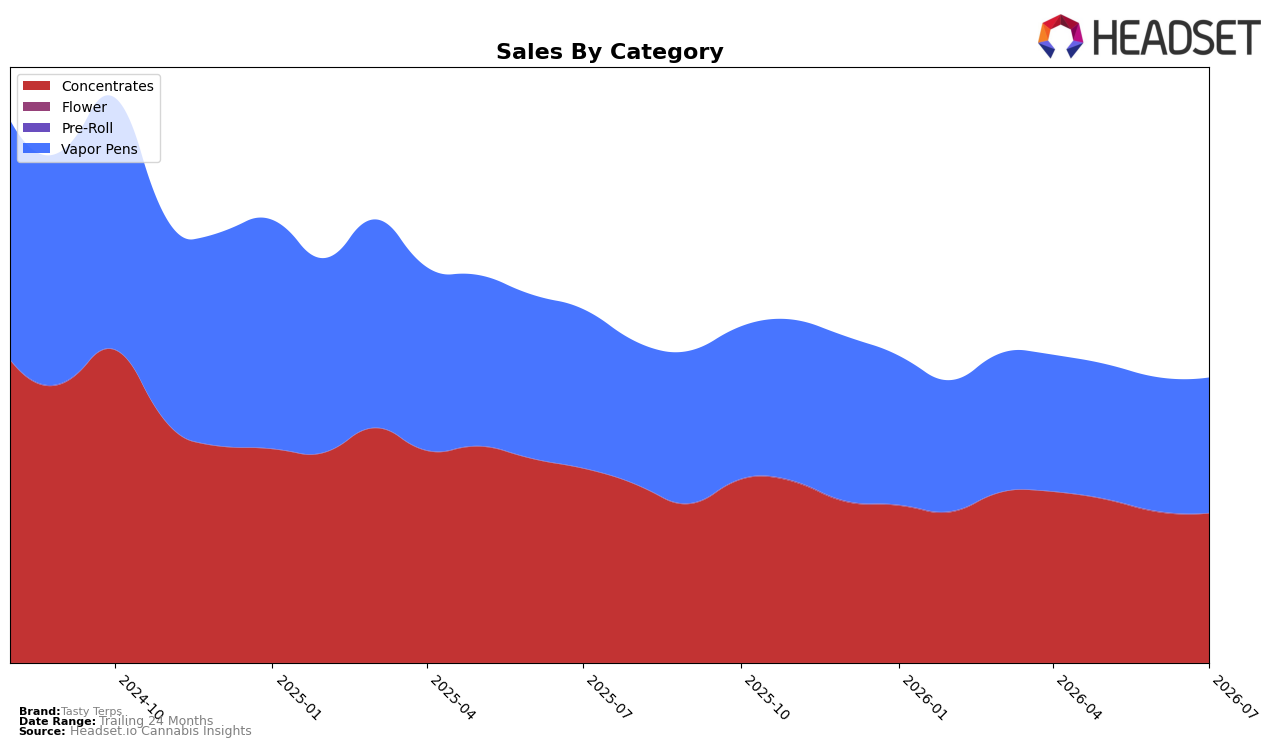

In July 2026, Tasty Terps concentrated its mix in Concentrates at 52.49% share while Vapor Pens held 47.51%, with Concentrates down 23.13% year over year and 0.85% month over month, and Vapor Pens down 14.86% year over year but up 1.09% month over month. The brand’s average price fell 1.90% year over year to $11.43, with category-level pricing at $10.53 in Concentrates and $12.64 in Vapor Pens, indicating a price ladder aligned with the mix. The pattern implies near-term volume is leaning on Vapor Pens’ month-over-month uptick to offset deeper year-over-year contraction in Concentrates, but the overall brand sales decline of 19.41% year over year suggests the current mix is not yet stabilizing total demand.

Tasty Terps sits at rank 14 in Concentrates in Washington, pairing a 52.49% mix weight with a 23.13% year-over-year decline, while the brand’s 24-month sales contraction of 44.99% frames a longer slide that pricing tweaks of −1.90% have not reversed. Given Vapor Pens’ 1.09% month-over-month gain against a 14.86% year-over-year dip and a higher price point at $12.64, the brand’s positioning is tilting toward margin preservation in pens while Concentrates drives scale at a lower $10.53, implying that share defense in Concentrates requires mix rebalancing or product tiering rather than further price compression.

Competitive Landscape

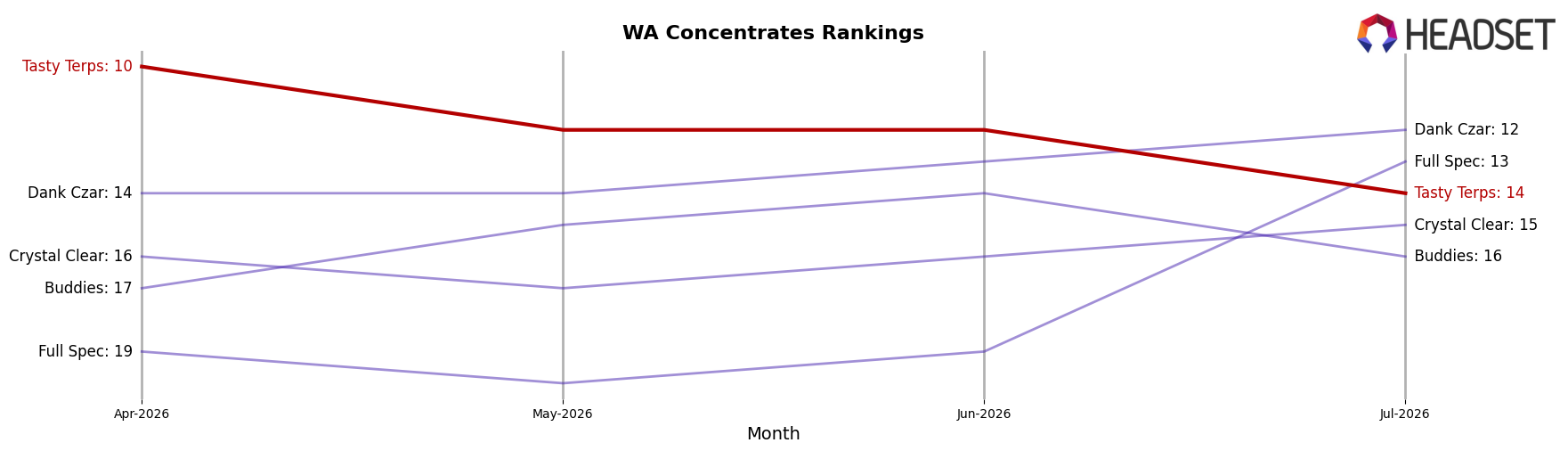

Tasty Terps sits at rank #14 in WA Concentrates for July 2026, down 5 positions year over year from #9, and 4 positions below its April 2026 mark of #10; the brand is also 8 spots beneath its October 2024 peak at #6, while category leaders shifted unevenly as Ooowee held #1 with a −6.9% YoY sales change and Dabstract climbed from #4 to #3 with a 5.2% YoY increase. In the same window, Constellation Cannabis advanced from #7 to #4 alongside an 18.9% YoY sales gain, while Oleum Extracts (Oleum Labs) stayed at #5 despite a −8.0% YoY decline, indicating that Tasty Terps’ slide from #10 in April 2026 to #14 in July 2026 is less about broad market contraction and more about lagging momentum against upward movers, implying the brand’s rank trajectory points toward further share pressure unless it reverses relative performance.

Notable Products

Gummy Bears Distillate Cartridge (1g) held rank 1 in July 2026 but slipped by 5.16% month over month, while Fruit Snax Distillate Cartridge (1g) fell 8.48% at rank 9, implying softening depth in Vapor Pens even as the flagship still leads. Gummy Bears BHO Wax (1g) rose 36.35% to rank 2 and Red Zkittlez BHO Wax (1g) climbed 20.82% to rank 3, and four of the top ten are Vapor Pens while four are Concentrates, indicating a split demand profile with Concentrates gaining momentum. Strawberry Kiwi Dum Dum Melted Diamond Cartridge (1g) advanced 20.15% at rank 4, but three other Vapor Pen SKUs at ranks 6–8 carry no prior-month baseline, so their contribution is directional but unquantified despite a combined $18,489 in sales. The pattern implies Tasty Terps is tilting from a single-SKU Vapor Pen anchor toward a two-pillar mix where Concentrates absorb growth while the pen portfolio diversifies to protect share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.