Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

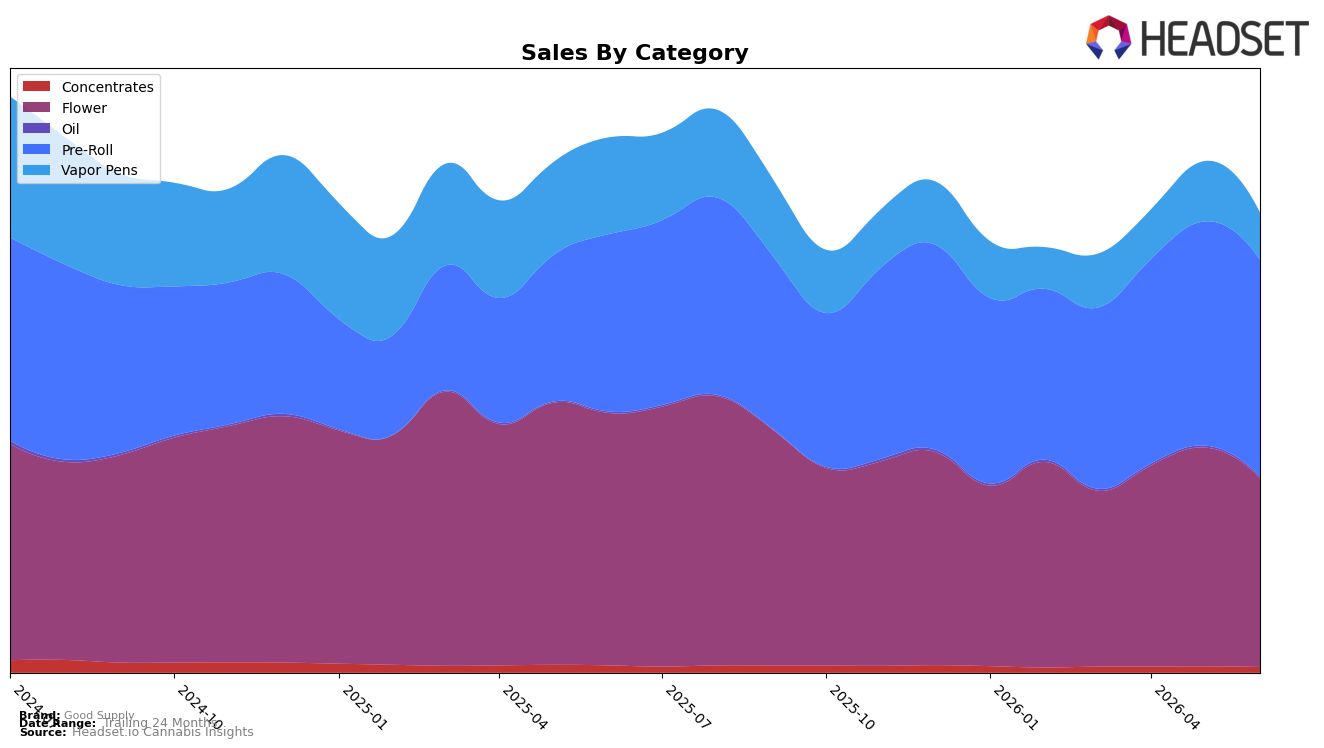

In June 2026, Good Supply concentrated 46.66% of sales in Pre-Roll, where category sales rose 22.22% year over year but slipped 3.20% month over month, while Flower held 40.60% share with a 25.16% year-over-year decline and a 13.73% month-over-month drop. Vapor Pens contracted to 10.41% share with a 50.43% year-over-year fall and a 21.33% month-over-month decline, as Concentrates at 1.60% decreased 17.32% year over year and 7.38% month over month; Oil remained a niche at 0.73% share, growing 9.64% year over year but easing 3.40% month over month. Despite total brand sales down 13.81% year over year and average price down 17.96%, the Pre-Roll mix and positive Pre-Roll growth indicate a pivot toward value-led volume in core formats while premium and device-adjacent segments retrench.

The mix shift lifts Good Supply’s emphasis on Pre-Roll competitiveness—reinforced by a rank of 5 in Pre-Roll in British Columbia—but the simultaneous 25.16% Flower decline and 50.43% Vapor Pens drop signal reduced breadth in higher-ticket or hardware-reliant segments. With June 2026 month-over-month declines in four of five categories, including 13.73% in Flower and 21.33% in Vapor Pens, the brand’s pricing-led strategy likely trades margin for share within Pre-Roll while ceding consideration where differentiation relies on potency, device ecosystem, or format innovation; this implies positioning that prioritizes accessible Pre-Roll scale over premiumization across adjacent categories.

Competitive Landscape

Good Supply sits at rank #7 in ON Pre-Roll for June 2026, unchanged year over year at #7 while slipping 1 position from #6 in March 2026, and its peak of #5 in January 2026 marks a 2-rank decline since that high; meanwhile, Back Forty / Back 40 Cannabis climbed from #3 to #1 with 74.6% YoY sales growth and Jeeter fell from #2 to #4 alongside a 48.5% YoY sales drop, indicating that Good Supply’s flat YoY rank combined with recent quarter slippage implies a hold on mid-tier placement while faster-moving rivals are reshuffling the top positions.

Notable Products

Berry Blurry Distillate Cartridge (1g) posted the steepest decline in June 2026 with a -29.8% MoM drop while slipping to rank 9, as Double Dutchies - Double Up Pre-Roll 2-Pack (2g) held rank 1 with a -1.7% MoM dip and Double Dutchies - Double Down Pre-Roll 2-Pack (2g) climbed 16.5% at rank 2. Four of the top ten are Pre-Roll SKUs, including Jean Guy Pre-Roll 14-Pack (7g) down -9.1% at rank 4 versus Jean Guy Pre-Roll (1g) up 6.9% at rank 3, implying the mix is tilting toward smaller pack formats and away from non-Pre-Roll options.

Ice Cream Rntz (7g) fell -9.1% at rank 8 while Jean Guy (3.5g) rose 7.6% at rank 5, and The Score Pre-Roll 20-Pack (10g) entered the list at rank 7 with $341,616 despite no MoM baseline. With top positions anchored by Pre-Rolls at ranks 1–4 while Vapor Pens sit at rank 9 with a double-digit decline, the pattern points to Good Supply concentrating demand in value-oriented Pre-Roll formats and reducing reliance on vapes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.