Market Insights Snapshot

Dro concentrated 99.38% of June 2026 sales in Flower with a 151.53% year-over-year gain and an 18.96% month-over-month lift, while Pre-Roll contracted to 0.62% share with a -62.63% month-over-month change and no year-over-year basis. The brand’s average price rose 38.27% year over year to $37.96 alongside a Flower average price of $39.12, indicating mix-driven price elevation as Flower scaled. The net effect is a portfolio narrowed toward a single category and higher realized pricing, which implies dependence on Flower volume and pricing to sustain the 153.09% brand-level year-over-year growth.

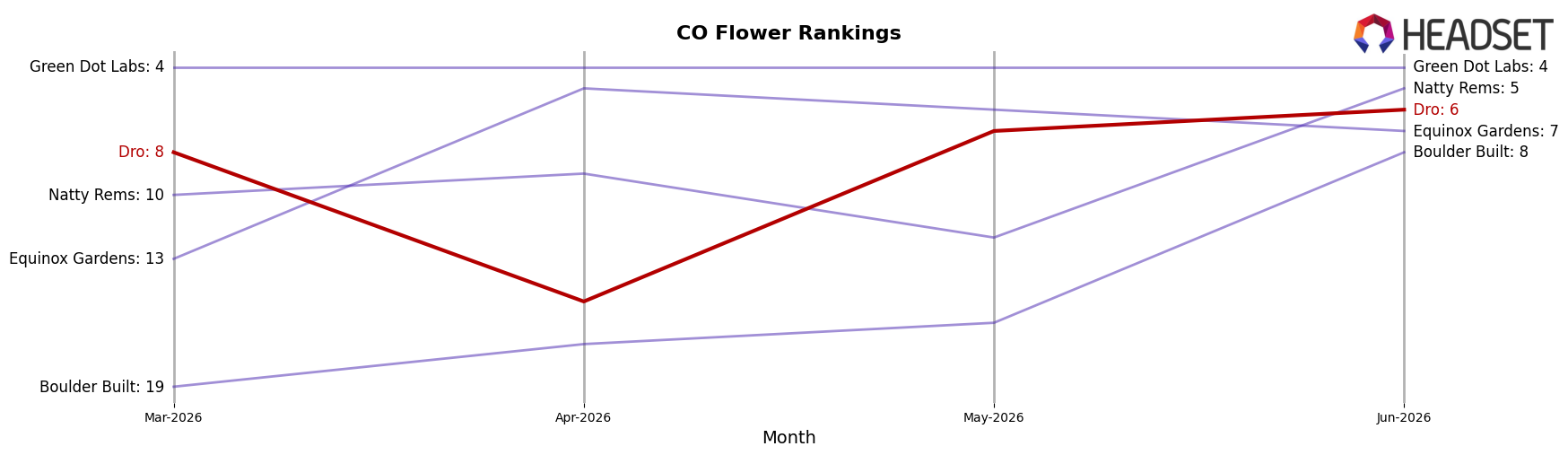

In Colorado Flower, Dro sat at rank 6 in June 2026, pairing a 151.53% Flower year-over-year increase with an 18.96% month-over-month uptick while Pre-Roll fell -62.63% month over month and held only 0.62% share. With 99.38% of mix in Flower and a 38.27% brand price increase, the positioning is oriented toward premiumized Flower velocity rather than breadth, meaning share gains will hinge more on sustaining rank 6 momentum within Flower than on diversifying into Pre-Roll.

Competitive Landscape

Dro ranks #6 in Colorado Flower in June 2026, rising 13 positions from #19 year over year, and edging up 2 spots from #8 three months ago; this coincides with a peak rank of #6 in June 2026 while Seed & Strain Cannabis Co. advanced from #2 to #1 and Natty Rems leapt from #28 to #5 on 220.97% YoY sales growth, indicating Dro is gaining placement but still ceding relative momentum to faster-climbing incumbents and challengers, which implies the trajectory is upward yet vulnerable to displacement without further share capture.

Notable Products

Moonbow (Bulk) led the narrative in June 2026 with a -66.2% month-over-month drop while holding rank 8, which, alongside Honeydew (7g) slipping 4.5% at rank 6, indicates bulk and mid-pack formats are ceding velocity even as top ranks stay concentrated. Lemonade Bacio (7g) rose 47.8% to rank 4 while Honey Banana (7g) and Gas Fruit (7g) occupied ranks 1 and 2, and with nine of the top ten being Flower SKUs the portfolio is tightly clustered in one category. The $2,182 result for Moonbow (Bulk) juxtaposed with a dual rank 9 tie among Blue Nerds (7g) and Cadillac Rainbows (7g) points to SKU proliferation at the bottom of the leaderboard without proportional volume. The pattern implies Dro is consolidating around 7g Flower winners while bulk experimentation is being deprioritized, concentrating share in a few high-velocity flower formats rather than spreading demand across pack sizes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.