Market Insights Snapshot

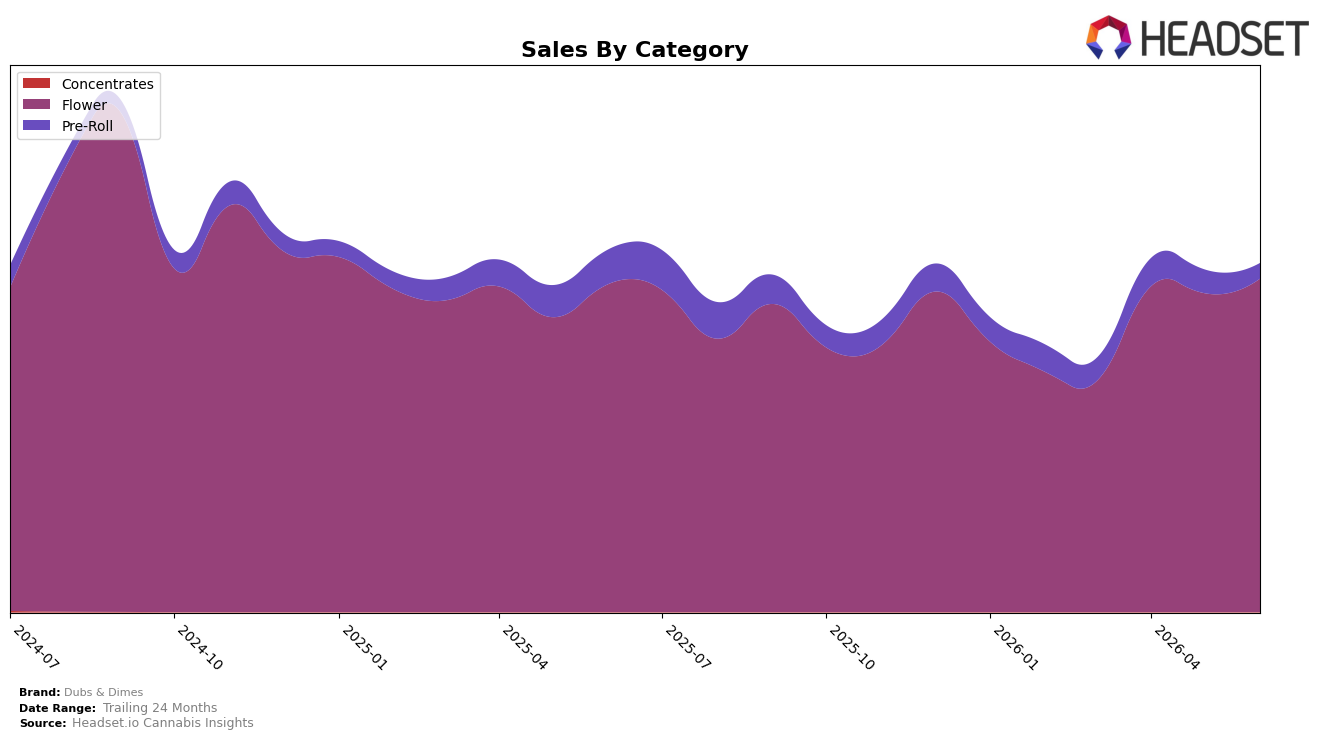

In June 2026, Dubs & Dimes concentrated 95.61% of sales in Flower while Pre-Roll held 4.39%, with Flower up 1.67% YoY and 4.56% MoM versus Pre-Roll down 55.41% YoY and 34.50% MoM. Despite brand-level sales down 3.74% YoY, the category tilt kept overall volume anchored in Flower, as evidenced by an average Flower price of $20.34 alongside a brand-wide average price rising 29.41% YoY; the mix is consolidating into a single growth engine while a shrinking Pre-Roll slice acts as a drag.

At a state-category rank of 19 in Michigan Flower, the 4.56% MoM Flower gain and 1.67% YoY lift suggest the brand is climbing within its core lane even as Pre-Roll contracts 34.50% MoM and 55.41% YoY. With 95.61% of sales tied to Flower and only 4.39% in Pre-Roll, the portfolio is over-indexed to a category where rank progress is plausible but fragile; the implication is that maintaining or improving rank 19 will depend on sustaining Flower’s MoM momentum while either exiting or re-pricing Pre-Roll to prevent further share erosion.

Competitive Landscape

Dubs & Dimes sits at rank #19 in MI Flower in June 2026, improving 1 place year over year from #20 and jumping 12 spots from #31 in March 2026, while still trailing its peak of #12 from September 2024; by contrast, Goodlyfe Farms climbed from #5 to #2 with 44.1% year-over-year sales growth and High Minded held #1 despite a 13.7% sales decline, indicating Dubs & Dimes’ upward rank momentum is recovery-driven relative to top-tier peers maintaining or accelerating share through larger percentage shifts.

Notable Products

MAC 1 (Bulk) posted the standout move in June 2026 with a +46.9% month-over-month lift while holding rank 5, contrasted by Lemon Cherry Gelato (Bulk) dropping -26.2% yet still at rank 2; this split suggests demand is rotating within bulk Flower toward higher-velocity genetics. Apple Fritter (Bulk) rose +20.0% to rank 1 as the top SKU, and with four of the top ten being Bulk Flower SKUs, the assortment is concentrating around bulk formats that can scale volume at a lower unit price point. The top three ranks are all Flower and two are Bulk, and Apple Fritter (Bulk) alone generated $94,458, implying channel buyers are prioritizing dependable bulk throughput over breadth in smaller pack sizes. Together these shifts indicate Dubs & Dimes is leaning into bulk-first momentum to capture share through velocity, even if it means accepting volatility among individual bulk strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.