Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Earl Baker is stocked at 170 licensed dispensaries across Oregon and Connecticut, 116 of them in Oregon, with the deepest coverage in Portland, Bend, Eugene, Salem, and Ontario. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

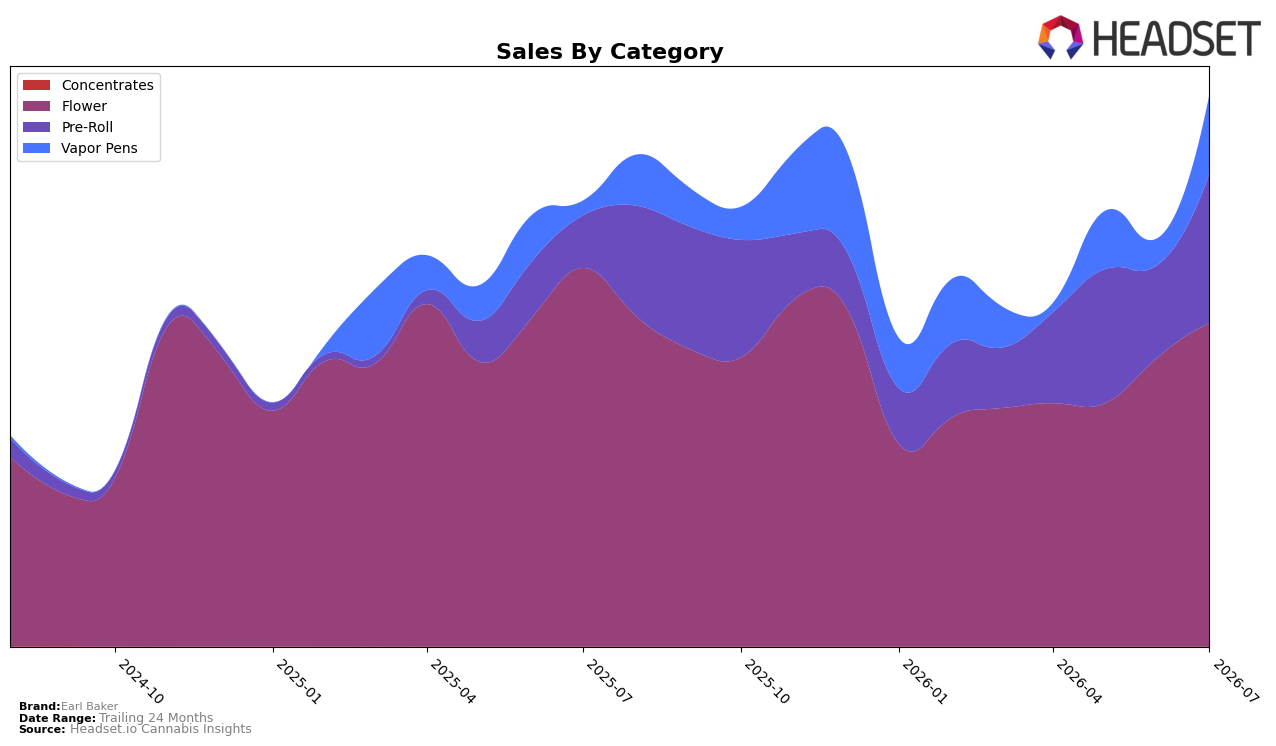

In July 2026, Earl Baker’s mix tilted toward Flower at 58.6% share while holding a rank of 16 in Flower in Connecticut, but category momentum is coming from elsewhere: Pre-Roll expanded 184.7% year over year and 61.8% month over month to 27.1% share, and Vapor Pens surged 445.8% year over year and 198.6% month over month to 14.3% share. By contrast, Flower declined 14.6% year over year even as it grew 11.8% month over month, and the brand’s average price fell 5.2% year over year to $23.44. The pattern implies the brand is reallocating demand toward faster-growth, lower-ticket segments while Flower provides scale but not growth velocity.

The July 2026 shifts signal a repositioning toward accessible entry points and higher-frequency formats: Pre-Roll’s rapid mix gains alongside a 61.8% month-over-month lift point to trial-driven acquisition, while Vapor Pens’ 198.6% month-over-month rise suggests successful pipeline expansion that can diversify revenue away from a Flower base down 14.6% year over year. With overall brand sales up 23.9% year over year and a 24‑month expansion of 195.3%, the implication is that Earl Baker’s growth is increasingly tied to portfolio breadth and price laddering rather than Flower rank strength at 16 in Connecticut.

Competitive Landscape

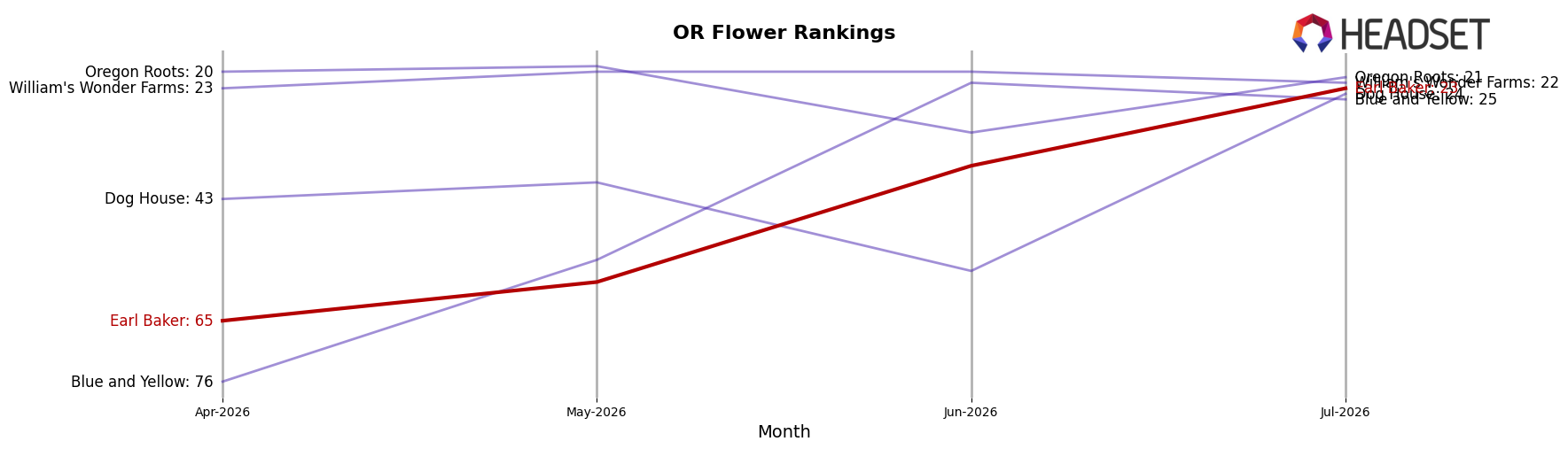

Earl Baker sits at rank #23 in July 2026, unchanged year over year from #23, after rebounding 42 ranks since April 2026 when it was #65; this stability contrasts with Grown Rogue climbing from #3 to #2 with a 53.47% YoY sales increase and Bald Peak sliding from #2 to #5 with a -15.47% YoY sales decline. The current position is four spots below Earl Baker’s peak at #19 in February 2025 and lags the category leaders where PRUF Cultivar / PRŪF Cultivar holds #1 with a 50.69% YoY sales gain and Otis Garden jumped from #12 to #4 with an 86.22% YoY lift; the pattern implies Earl Baker has regained distribution or assortment share recently but is not converting it into category-advancing momentum relative to faster-rising peers.

Notable Products

Frozen Bag Pre-Roll 2-Pack (1g) posted a 209.8% month-over-month surge to rank 2, while Periwinkle Pez Pre-Roll (1g) fell 19.6% at rank 5; this divergence within the same format suggests the pre-roll lineup is polarizing around value and format. Private Party Pre-Roll 2-Pack (1g) also rose 78.9% at rank 8, and four of the top ten are Pre-Roll SKUs, indicating mix is tilting toward multi-pack and value pre-rolls over single sticks. Chem XL (3.5g) held rank 1 with $61,787 and no reported month-over-month rate, while Flower holds ranks 1, 3, 4, 6, and 9, pointing to a split where flagship Flower anchors share as Pre-Roll growth supplies incremental velocity. The pattern implies Earl Baker is migrating demand toward bundled Pre-Roll offerings while relying on a single Flower halo SKU to stabilize rankings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.