Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

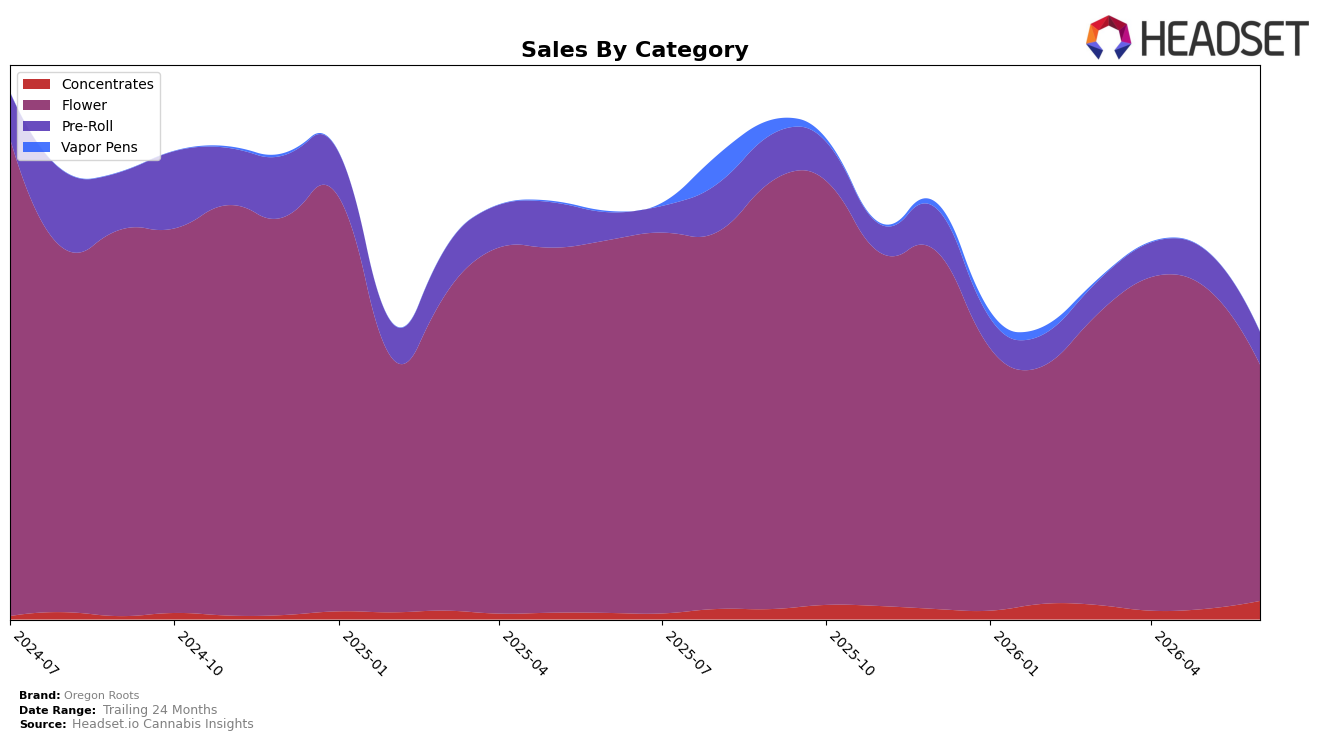

Oregon Roots is concentrated in Flower at 82.37% share, but that anchor shrank with a year-over-year decline of 36.65% and a month-over-month drop of 26.69% in June 2026, while average price across the brand fell 37.78% YoY, indicating volume did not offset price compression. Pre-Roll held 11.29% share with a 17.98% YoY increase yet slipped 12.34% MoM, and Concentrates, at 6.34% share, surged 193.89% YoY and 78.53% MoM, signaling that growth is clustered in smaller formats even as total brand sales were down 29.61% YoY in June 2026. With a Flower rank of 26 in Oregon, the mix tilt and price reset imply the flagship category is losing traction faster than the portfolio can re-balance, and the operational takeaway is to accelerate mix shift where velocity is rising while stabilizing Flower price-pack architecture.

The rapid Concentrates acceleration of 78.53% MoM and 193.89% YoY, combined with Pre-Roll’s 17.98% YoY but 12.34% MoM pullback, points to a portfolio pivot opportunity: lean into formats with momentum while using Flower’s 82.37% base and rank 26 in Oregon to trial trade-up tiers or value packs that can arrest the 26.69% MoM decline. Given the brand’s average price is down 37.78% YoY against a 29.61% YoY sales contraction, price elasticity is unfavorable in Flower relative to Concentrates’ growth, implying that Oregon Roots should treat Concentrates as a margin recapture wedge and reposition Flower to defend share without further diluting price.

Competitive Landscape

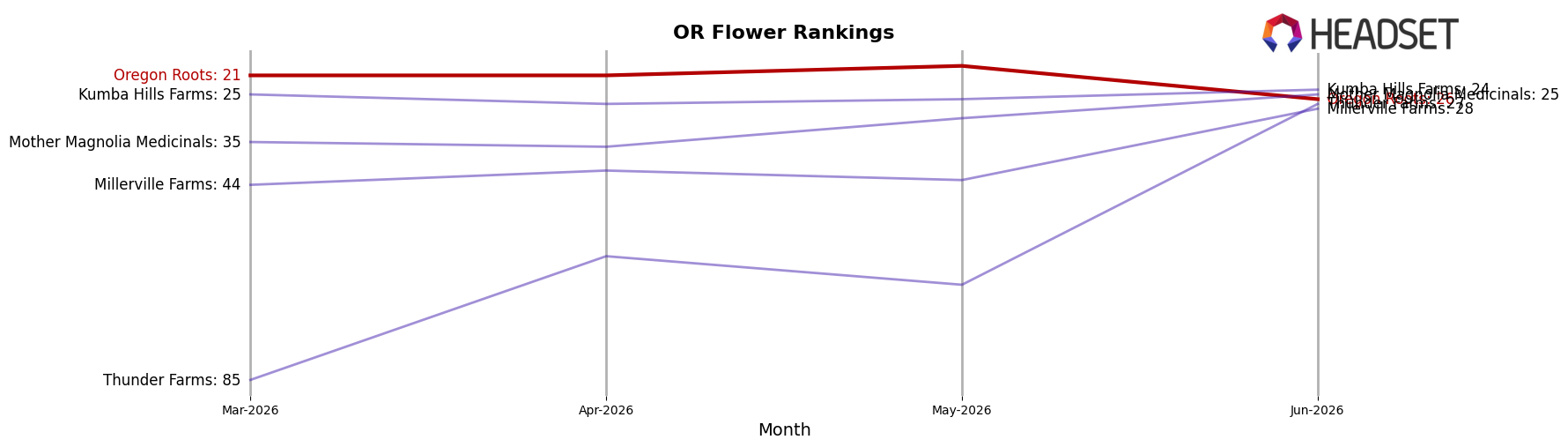

Oregon Roots sits at rank #26 in Oregon Flower in June 2026, down 10 places year over year from #16, and 5 places lower than its March 2026 position of #21; this follows a broader slide from a peak of #8 in July 2024 to outside the top 25. In contrast, Grown Rogue rose from #6 to #2 alongside a 123.97% year-over-year sales increase, while PRUF Cultivar / PRŪF Cultivar held #1 year over year at #1 with 18.71% sales growth, indicating share consolidation at the top as Oregon Roots lost rank share. With rank deterioration of 10 spots year over year and a 5-spot drop versus three months prior, the trajectory implies Oregon Roots is ceding competitive position to faster-advancing leaders unless mix, distribution, or pricing levers reverse the trend.

Notable Products

Strawberry OG (Bulk) posted the standout move with a 197.2% month-over-month surge to $23,992 and entered June 2026 at rank 3, while Blue Dream (Bulk) climbed 69.3% to rank 9. In contrast, Mo'Bama (Bulk) fell 42.7% to rank 10 and Grape Snow Train (7g) dropped 16.8% at rank 5, as Mo'Bama (1g) rose 24.7% to hold rank 1. With eight of the top ten SKUs in Flower, the pattern implies a pivot toward bulk Flower momentum anchored by a few high-velocity strains while single-gram Flower and mid-size packs absorb volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.