Market Insights Snapshot

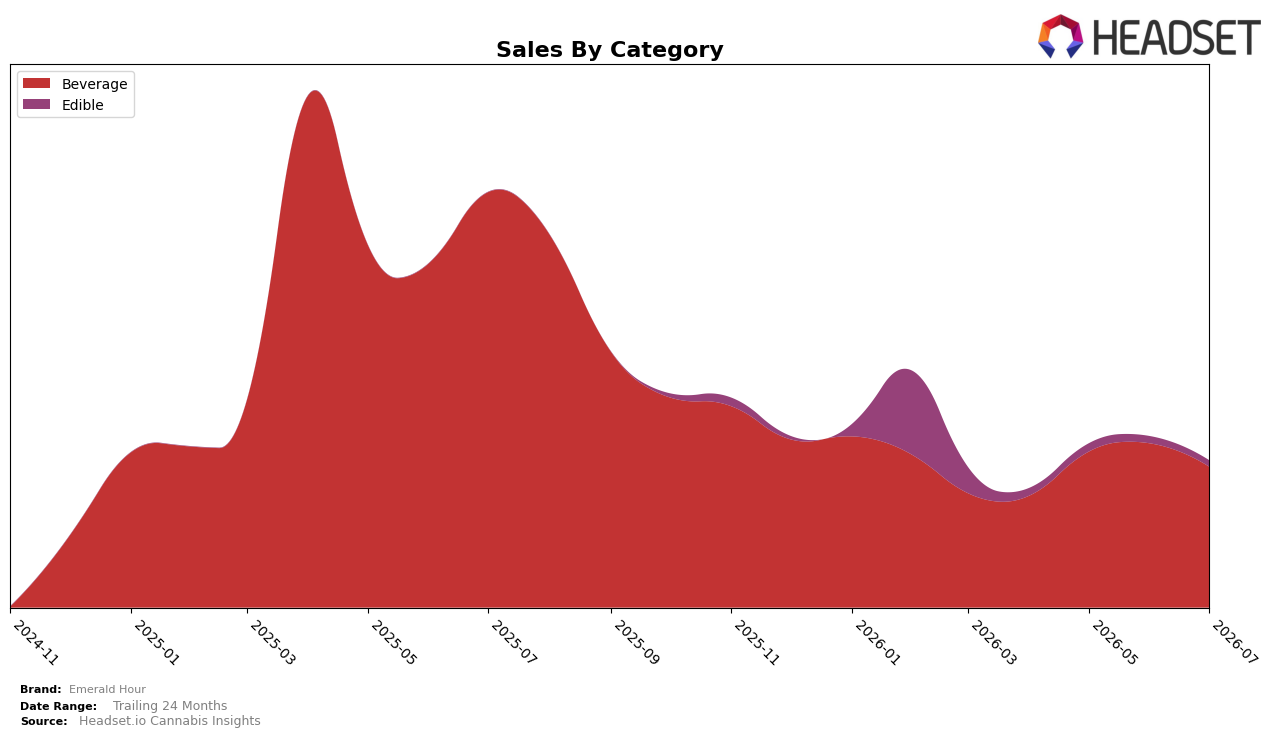

In July 2026, Emerald Hour concentrated 95.88% of sales in Beverage while Edible held 4.12%, marking a category mix that tightened versus prior periods as Beverage declined 14.21% month over month and 66.13% year over year, while Edible fell 11.25% month over month with no year-over-year baseline. The brand’s average price dropped 8.99% year over year to $7.45 as Beverage averaged $7.45 and Edible averaged $7.59, and within the Beverage category Emerald Hour sat at rank 28 in Ontario; the concentration alongside sharper Beverage contraction implies Emerald Hour’s mix amplified exposure to a steeper-downturn segment.

The July 2026 pattern implies Emerald Hour’s positioning is defined by a high Beverage dependency at 95.88% share coupled with a rank of 28 in Ontario, which, combined with a 14.21% month-over-month Beverage decline and an 11.25% month-over-month Edible decline, limits internal hedging. With Beverage down 66.13% year over year and the brand-level sales down 64.68% year over year, the 8.99% average price reduction signals price-led defense rather than mix-driven resilience; the practical implication is a need to diversify beyond a single category footprint while using Edible’s 4.12% share as a test bed for margin-stable extensions.

Competitive Landscape

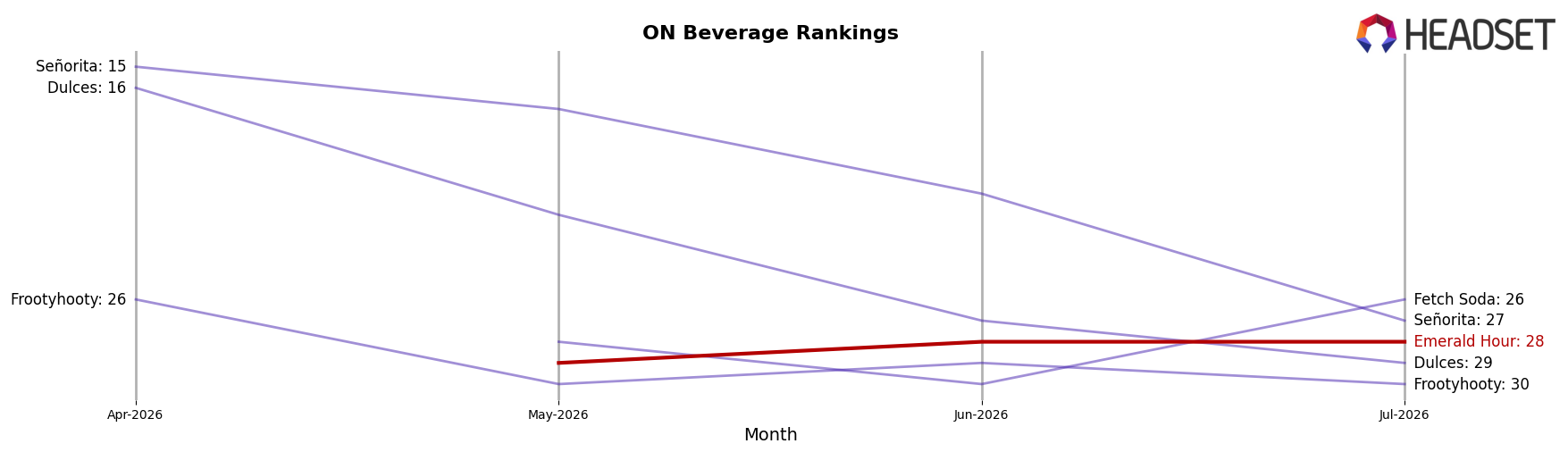

Emerald Hour sits at #28 in ON Beverage in July 2026, down 7 ranks year over year from #21, but up 6 positions versus three months ago from #34, indicating a mid-year rebound after a longer slide since its peak at #21 in July 2025. Against leaders, Versus advanced from #3 to #1 with 18.1% year-over-year sales growth while XMG fell from #1 to #2 with a 37.2% sales decline, and Mollo eased from #2 to #3 with a 1.1% dip, positioning Emerald Hour’s #28 standing as exposed to a consolidating top tier and suggesting its rank trajectory implies stabilization is possible but only if the recent 6-rank quarter-on-quarter climb can outpace entrenched leaders’ gains.

Notable Products

Lime Mint Soda (10mg THC , 222ml, 7.5oz) led July 2026 with a month-over-month surge of 156.2% while jumping into a shared rank of 4, contrasting with Agave Lime Sea Salt Live Rosin Soda (10mg THC, 222ml) sliding 38.9% to rank 2. Cranberry Citrus Live Rosin Soda (10mg THC, 222ml) held rank 1 with a 1.9% dip, and Ginger Lime Soda (10mg THC, 222ml) rose 28.6% at rank 4 as four of the top five SKUs were Beverages. Peach White Grape Live Rosin Gummies 2-Pack (10mg) fell 11.3% at rank 3 despite $626 in sales, indicating non-beverage trial is lagging even as beverage variety broadens. Overall, the outsized beverage rebound alongside concentrated top-five beverage presence implies Emerald Hour is consolidating around drinkables and testing flavor extensions to drive velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.