Market Insights Snapshot

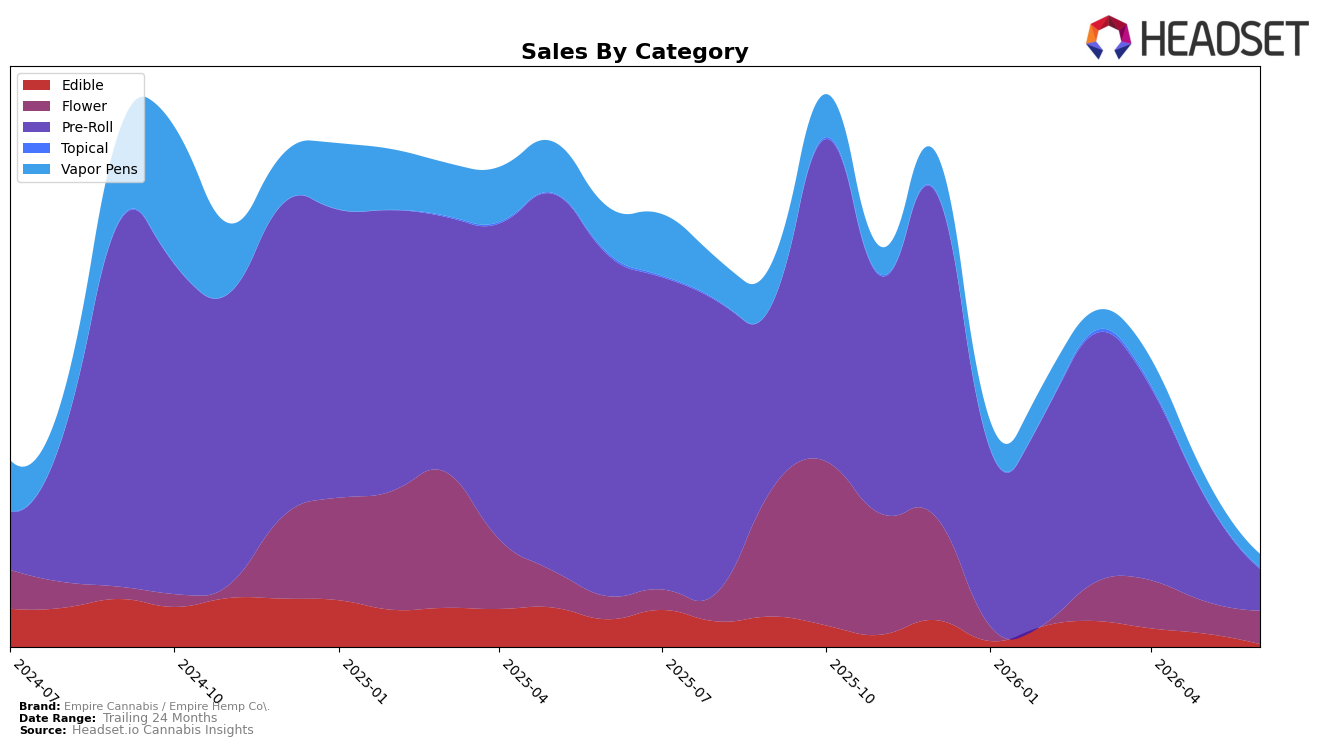

Empire Cannabis / Empire Hemp Co.’s category mix in June 2026 pivoted toward Flower at 36.15% share while Pre-Roll, still the largest slice at 45.10% share, contracted sharply with year-over-year down 87.85% and month-over-month down 60.35%. Flower moved the other way, with year-over-year up 46.53% and month-over-month up 3.47%, while Vapor Pens fell 71.36% year-over-year and 32.47% month-over-month to 14.32% share. Edible dropped 89.48% year-over-year and 78.23% month-over-month to just 3.19% share, whereas Topical, though only 1.24% share, was up 28.79% month-over-month despite a 30.16% year-over-year decline; combined with a 0.19% increase in average price to $26.24, the pattern implies the brand is shedding low-velocity formats and leaning into a smaller, higher-priced core anchored by Flower.

The shifts imply a defensive repositioning toward fewer, clearer roles: Flower as the growth engine (up 46.53% year-over-year and 3.47% month-over-month) and Pre-Roll as a shrinking traffic driver (down 87.85% year-over-year and 60.35% month-over-month) that may require SKU rationalization. With Vapor Pens contracting 71.36% year-over-year and Edible down 89.48% year-over-year while Topical ekes out a 28.79% month-over-month gain off a 1.24% share base, Empire Cannabis / Empire Hemp Co. is consolidating around categories where pricing power can support margin stability, implying a need to reallocate merchandising and inventory in New York toward Flower-led baskets and away from underperforming formats.

Competitive Landscape

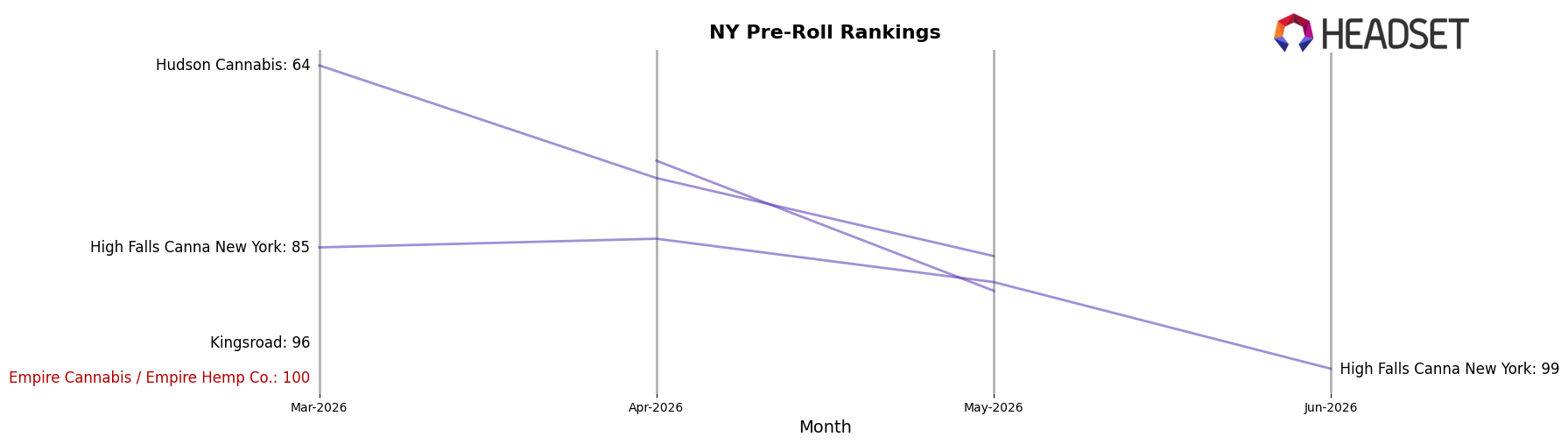

Empire Cannabis / Empire Hemp Co. sits at rank 211 in NY Pre-Roll for June 2026, down 132 positions year over year from rank 79, and off 111 positions versus March 2026 when it held rank 100; relative to its peak rank of 56 in September 2024, the brand is 155 places lower, indicating a sustained retreat. In contrast, Ruby Farms holds rank 1 with a 15.6% year-over-year sales increase while Anthem advanced to rank 3 from rank 40 alongside an 852.1% year-over-year sales surge, and Heady Tree rose to rank 4 from rank 8 with 125.5% sales growth; even Jetpacks slipped modestly from rank 3 to rank 5 with an 8.6% sales decline, yet still sits 206 places above Empire Cannabis / Empire Hemp Co. The pattern implies share is consolidating among top-tier movers while Empire Cannabis / Empire Hemp Co.’s drop from rank 79 to 211 signals fading shelf presence that, without a reversal, will keep the brand outside the competitive set that is gaining velocity.

Notable Products

Stank Breath Rosin Infused Pre-Roll (2g) posted the standout movement in June 2026 with a +320.4% month-over-month surge to rank 3, while Cherry Galaxy Infused Pre-Roll (2g) collapsed by -96.6% to rank 8. Big Bush Kush Infused Pre-Roll (2g) slid -23.0% yet held rank 1, and Dream Diamond Infused Flower (3.5g) grew +3.5% at rank 2. The juxtaposition of a tripling gain alongside a near-wipeout within infused pre-rolls implies volatile consumer trial concentrated in a few SKUs rather than stable franchise depth.

Vapor Pens contracted broadly with Wedding Cake Distillate Cartridge (0.5g) down -50.6% at co-rank 5 and Berry White Distillate Cartridge (0.5g) down -41.7% at rank 6, while Strawberry Cough Distillate Cartridge (0.5g) declined -11.1% at rank 4. With three Vapor Pens in the top 10 all posting double-digit or worse drops and only one Flower SKU posting a +3.5% gain, the category mix points to a pivot away from cartridges toward higher-variance infused pre-rolls that are intermittently spiking volume, likely stressing inventory planning even as headline ranks remain concentrated at the top.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.