Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

High Falls Canna New York is stocked at 85 licensed dispensaries across New York, with the deepest coverage in New York, Albany, Menands, Airmont, and Arlington. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

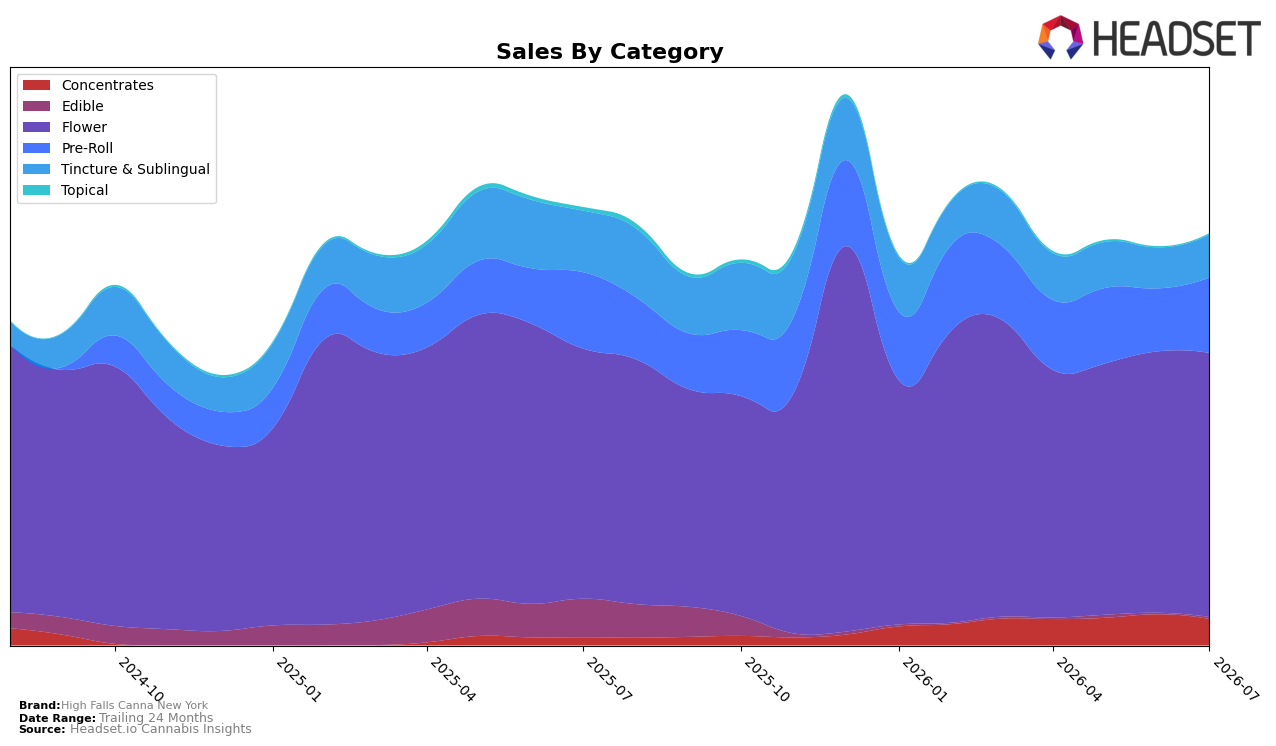

High Falls Canna New York concentrated its July 2026 revenue in Flower at 64.27% share with 5.57% year-over-year growth and a 1.01% month-over-month lift, while Pre-Roll held 18.30% share with a 19.88% month-over-month increase but a 1.22% year-over-year decline. Tincture & Sublingual captured 10.41% share despite a 30.26% year-over-year drop and a 5.22% month-over-month rise, and Concentrates expanded year-over-year by 233.26% but contracted 15.32% month-over-month at a 6.36% share. Minor categories moved at the margins: Edible fell 95.73% year-over-year yet rebounded 43.38% month-over-month to 0.40% share, and Topical declined 67.86% year-over-year with a 14.89% month-over-month uptick to 0.25% share. Taken together, the mix indicates a tilt toward inhalables with Flower stability and Pre-Roll momentum offsetting wellness category erosion, which helps explain a modest brand-level year-over-year sales decline of 5.96% alongside a 5.28% year-over-year drop in average price.

Positioning-wise in New York, the 64.27% Flower weight paired with a rank of 48 in Flower suggests reliance on a large but competitively stratified segment, where a 1.01% month-over-month gain must counteract pricing pressure from a 5.28% brand average price decline year-over-year. The 19.88% month-over-month surge in Pre-Roll provides short-cycle volume insurance against Tincture & Sublingual’s 30.26% year-over-year contraction, but the 15.32% month-over-month dip in Concentrates after a 233.26% year-over-year jump signals volatility that limits dependable contribution. The implication is a near-term need to deepen share in core Flower while converting Pre-Roll’s month-over-month growth into sustained share gains, using selective price architecture to mitigate the brand’s 5.96% year-over-year sales contraction without overexposing lower-growth wellness formats.

Competitive Landscape

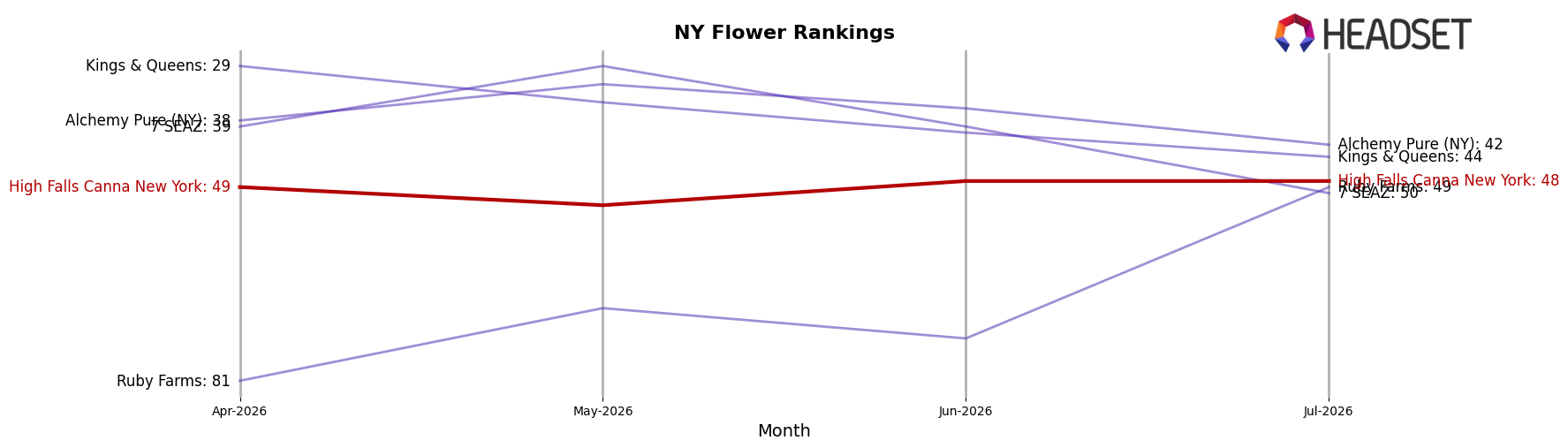

High Falls Canna New York sits at rank #48 in NY Flower in July 2026, improving 2 positions from #50 year over year and edging up 1 spot from #49 in April 2026, yet still well below its peak rank of #28 from July 2024; by contrast, Find. advanced from #8 to #1 with a 46.7% year-over-year sales increase while Grassroots jumped from #15 to #5 on 79.8% growth, indicating that High Falls Canna New York’s marginal rank gains are being outpaced by competitors’ larger climbs and implying its trajectory points to stabilization rather than a return toward prior peak positioning.

Notable Products

OG Kush Pre-Roll 2-Pack (1g) posted the largest move in July 2026 with a +52.2% month-over-month surge, climbing to rank 4, while Sour Diesel x OG Kush (3.5g) slid -10.3% to rank 9; this split implies consumer trading up within Pre-Rolls even as one legacy Flower SKU loses momentum. Girl Scout Cookies X (3.5g) held rank 1 with +6.0% growth, and Killer Queen HV (3.5g) advanced +25.5% to rank 7, while three infused or value-forward Pre-Roll SKUs clustered at ranks 4–6 with +45.3% to +52.2% gains, indicating a concentration of demand in the Pre-Roll format. With five of the top ten in Flower but a contiguous block of high-growth Pre-Rolls, the product mix suggests a pivot toward faster-turn, lower-gram formats that can stabilize share while flagship Flower anchors dollar volume at $31,303.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.