Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Generic AF is stocked at 120 licensed dispensaries across New York, with the deepest coverage in New York, Rochester, Syracuse, Albany, and Queens. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

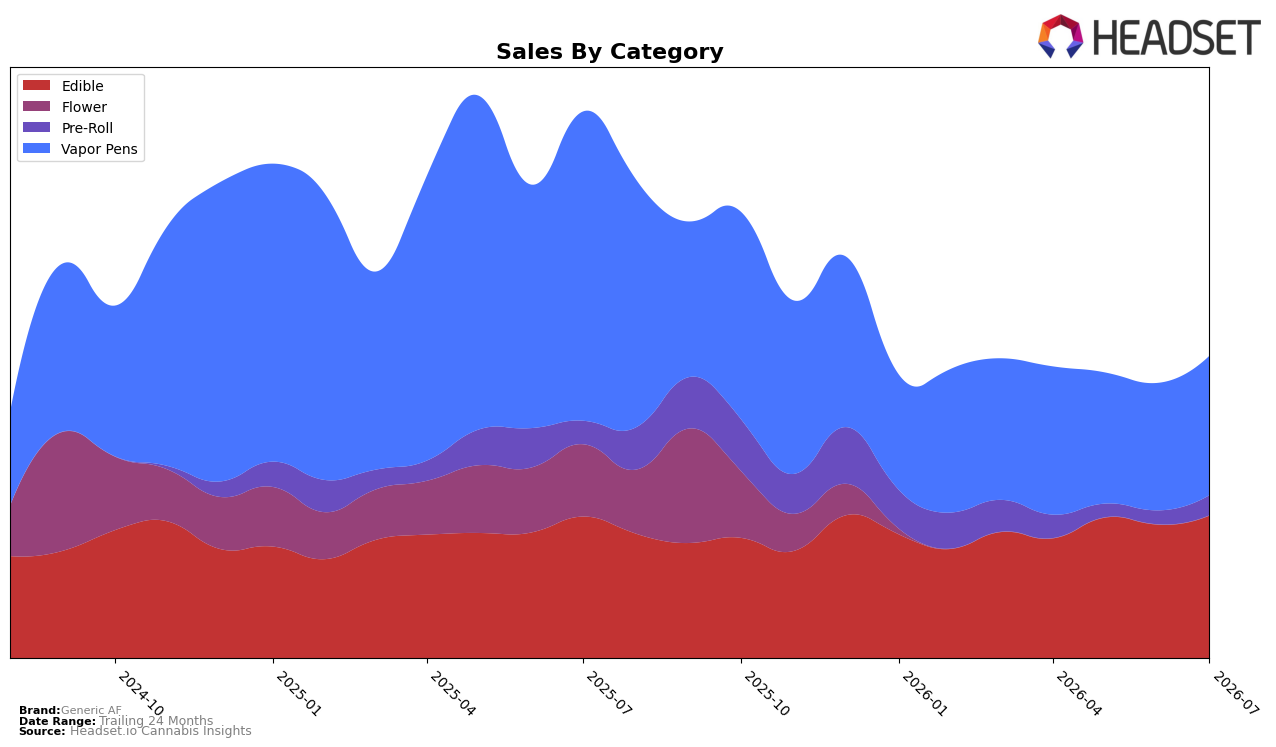

Generic AF’s category mix in July 2026 tilted toward Edible at 47.22% share and rank 19 in Edible in New York, while Vapor Pens held 46.20% share; the divergence is in growth rates, with Edible up 0.65% YoY and 6.77% MoM versus Vapor Pens down 54.98% YoY but up 9.40% MoM. Pre-Roll contributed 6.58% share with a 14.53% YoY decline but a 45.07% MoM jump, and the brand-level YoY sales change of -44.79% contrasts with a 179.34% 24-month gain and a 23.28% YoY drop in average price; the pattern implies the brand is stabilizing mix via month-over-month gains in all three categories while longer-term contraction in Vapor Pens weighs on annual comps.

The shifts suggest Generic AF is pivoting toward categories less exposed to YoY volatility, with Edible’s 0.65% YoY increase and 6.77% MoM lift supporting the brand’s highest-share position at 47.22%, while Vapor Pens’ 54.98% YoY decline against a 9.40% MoM rise signals rebound potential but a weaker baseline. With Pre-Roll’s 45.07% MoM surge off a 14.53% YoY decline and average price down 23.28% YoY to approximately $21.39, the implication is that price-led accessibility is fueling near-term unit momentum, and maintaining rank 19 in Edible within New York will likely depend on leaning into Edible mix while treating Vapor Pens as a tactical recovery lane rather than a core growth engine.

Competitive Landscape

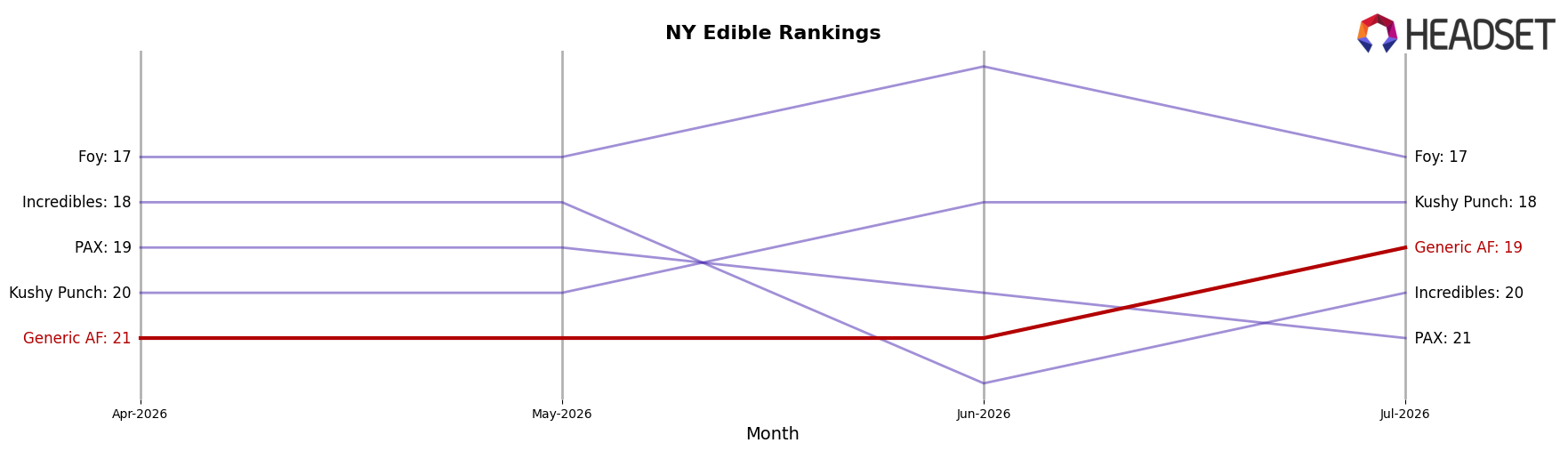

Generic AF sits at rank #19 in NY Edible for July 2026, down 2 spots year over year from #17 while improving 2 positions versus April 2026’s #21, and still below its peak of #14 from October 2024; meanwhile, Off Hours slid from #1 to #2 with a -10.4% YoY sales change as Wyld held steady at #3 with +7.4% YoY sales, signaling that Generic AF’s mid-pack drift is more about lost relative velocity than a market-wide contraction and implying its current trajectory risks further share erosion without a shift that converts the recent 2-rank rebound into sustained gains.

Notable Products

Blue Dream Pre-Roll 5-Pack (2.5g) posted the standout move in July 2026 with a 68.3% month-over-month surge, jumping into rank 7, while Blue Dream Distillate Cartridge (1g) rose 53.7% to secure rank 1; in contrast, Blue Raspberry Gummies 20-Pack (100mg) fell 11.0% to rank 2 and Maui Waui Distillate Cartridge (1g) slipped 9.4% to rank 10. Three Vapor Pens landed in the top ten at ranks 1, 3, and 4, whereas five Edibles clustered at ranks 2, 5, 6, 8, and 9, indicating a portfolio split where rapid gains in inhalables offset Edible softness and point to a tilt toward inhalable-led velocity in the near term.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.