May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

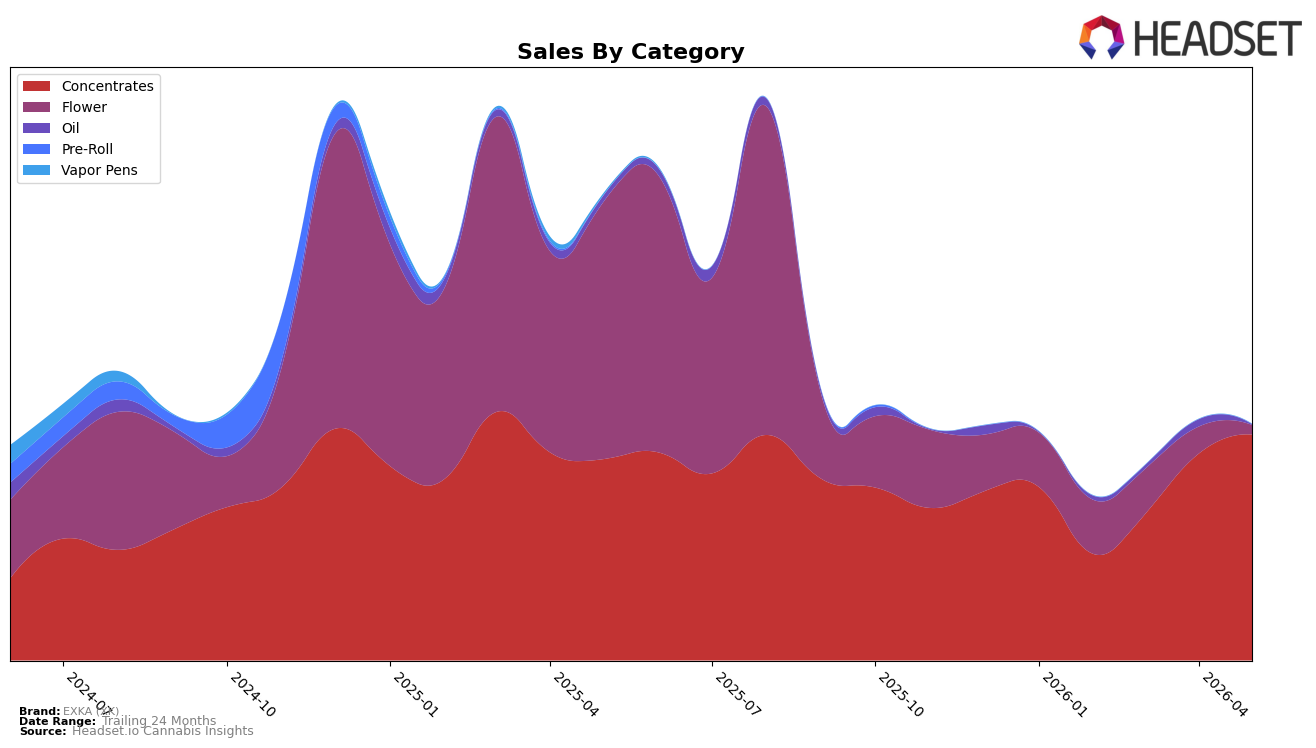

In May 2026, EXKA (XK) concentrated 95.86% of sales in Concentrates, where sales grew 12.20% year over year and 9.25% month over month, while the brand’s average price fell 12.08% YoY and the overall brand sales declined 49.49% YoY. Flower dropped to 3.94% share with a 96.39% YoY contraction and a 65.39% MoM decline, and Oil slid to 0.20% share with a 92.52% YoY decline and a 93.37% MoM fall; the concentration in a single category coincides with a 24-month sales change of -23.15%, implying that diversification erosion is amplifying downside volatility even as the core category posts positive comps.

Within Concentrates, EXKA (XK) sits at rank 30 in Ontario, pairing double-digit category growth of 12.20% YoY with a 9.25% MoM lift, while Flower and Oil’s steep declines of 96.39% YoY and 92.52% YoY respectively indicate intentional de-emphasis rather than transient weakness. This pattern suggests the brand is trading margin for volume via a 12.08% YoY price reduction and leaning into a single-category identity; the implication is a positioning bet on depth over breadth, which can support share defense at rank 30 but leaves limited buffer if Concentrates demand normalizes or price elasticity tightens.

Competitive Landscape

EXKA (XK) sits at rank #30 in ON Concentrates in May 2026, unchanged year over year from rank #30, but up 15 positions versus three months ago from #45, while still trailing its historical peak of #28 from March 2025; in contrast, Pura Vida advanced from #4 to #2 alongside a 30.8% YoY sales increase, and Endgame slid from #2 to #5 with a 49.7% YoY sales decline, indicating EXKA (XK)’s flat YoY rank masks near-term momentum that, if sustained, positions it to re-enter the high-20s tier.

Notable Products

Happy Hour (3.5g) posted the largest movement in May 2026 with a month-over-month gain of 110.97% and climbed to rank 5, while Happy Hour (7g) fell 78.85% to rank 4, indicating a trade-down within the same family toward smaller pack sizes. Haschtag Premium Hash (2g) rose 79.82% to rank 2 as Haschtag - Strwaberry Hash (2g) declined 13.79% yet held rank 1, implying mix shift toward premium within concentrates rather than a category exit. With Concentrates occupying ranks 1–3 and Flower split between a +110.97% upswing and a -78.85% drop, four of the top ten cluster in Concentrates and Flower, suggesting EXKA (XK) is consolidating demand around hash-based SKUs while right-sizing Flower formats. The pattern implies EXKA (XK) is leaning into premium hash while pivoting Flower toward value-oriented smaller sizes to stabilize share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.