Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

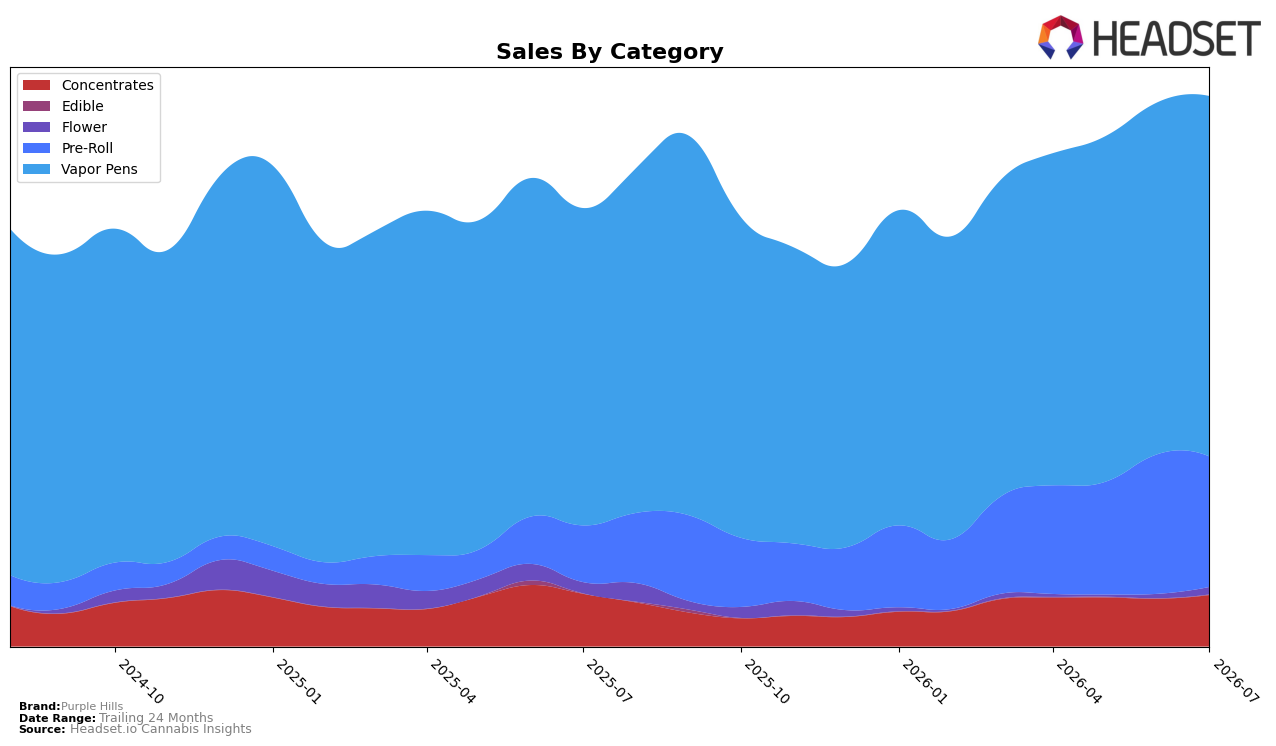

Purple Hills concentrated 65.62% of July 2026 sales in Vapor Pens with year-over-year growth of 13.59% and month-over-month growth of 2.40%, while Pre-Roll expanded to 23.72% share with 130.93% YoY but slipped 6.65% MoM. Concentrates held 9.33% share with a 2.31% YoY decline but a 7.72% MoM gain, and Flower, at 1.29% share, dropped 35.20% YoY yet jumped 75.15% MoM; Edible, though only 0.04% share, surged 987.33% YoY and 138.03% MoM. With an average price down 32.93% YoY to $21.38 and Vapor Pens ranked 13th in Ontario, the category mix points to a volume-led strategy where Pre-Roll and entry-price Edible act as acquisition lanes while Vapor Pens anchor core revenue.

The shift toward Pre-Roll’s 23.72% share alongside Vapor Pens’ 65.62% indicates a barbell positioning: value access via lower-price Pre-Roll (−6.65% MoM suggesting promo saturation) paired with steady Vapor Pen retention (+2.40% MoM). The 75.15% MoM rebound in Flower against a 35.20% YoY decline, plus a 7.72% MoM lift in Concentrates despite a 2.31% YoY dip, implies selective experimentation that can feed trade-up into Vapor Pens where the brand sits at rank 13 in Ontario; the pattern suggests leaning into cross-category bundles and laddering from Pre-Roll and Edible surges toward higher-margin inhalables as price elasticity (−32.93% YoY average price) keeps trial costs low.

Competitive Landscape

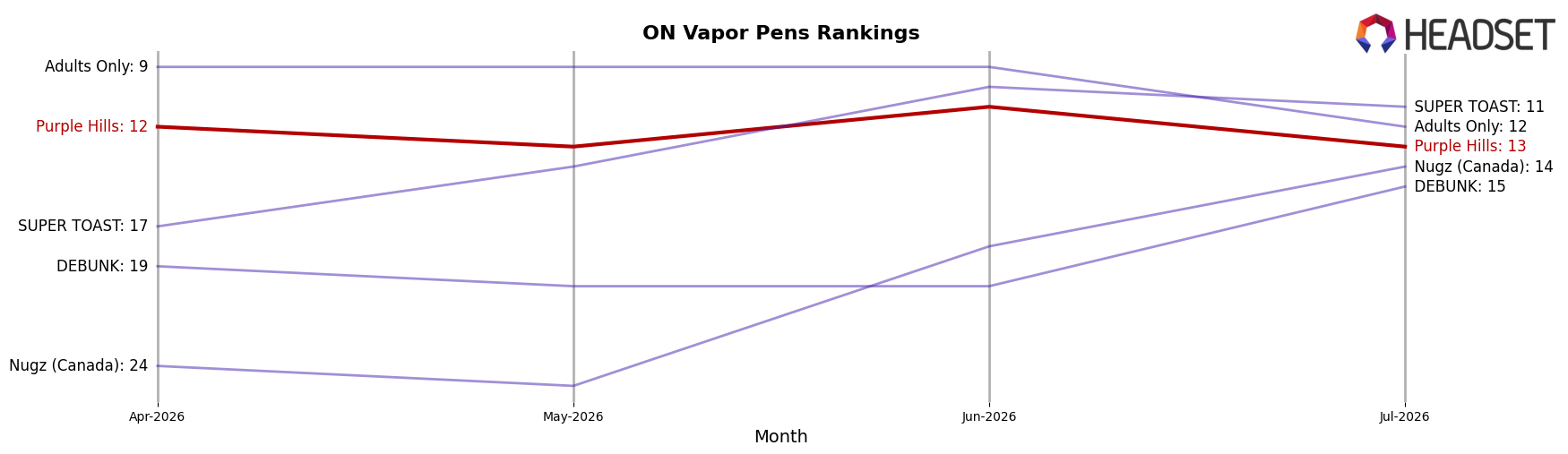

Purple Hills ranks #13 in ON Vapor Pens in July 2026, down 1 position YoY from #12 and slipping 1 place from April 2026’s #12, despite peaking at #11 in June 2026 before retreating 2 ranks month over month. In contrast, Spinach climbed from #4 to #1 with 144.7% YoY sales growth, while BoxHot moved from #2 to #3 alongside a 4.6% YoY sales increase, indicating competitors are either consolidating leadership or holding ground as Purple Hills loses incremental rank share. The pattern implies Purple Hills is oscillating near the edge of the top 10 but failing to convert a June 2026 peak into sustained gains, suggesting short-lived momentum in a market where upward moves by leaders are outpacing its marginal rank changes.

Notable Products

Indica Distillate Cartridge (1g) delivered the headline move in July 2026 with a +531.9% month-over-month surge and jumped to rank 2, while Iced Sangria Pre-Roll (1g) rose +61.2% to hold rank 1. In contrast, Tropical Cooler Pre-Roll 5-Pack (5g) fell -17.4% to rank 6 and Purple Oreoz Pre-Roll 10-Pack (5g) declined -15.5% to rank 8, indicating pressure within multipack Pre-Rolls. With four of the top ten being Pre-Roll SKUs and five in Vapor Pens, the balance tilts toward Vapor Pens on growth velocity as Sativa Distillate Cartridge (1g) added +701.2% MoM at rank 4 and Orangeade Live Resin Cartridge (1g) climbed +35.3% at rank 7. The pattern implies Purple Hills is pivoting toward high-velocity Vapor Pens while trimming underperforming Pre-Roll multipacks, concentrating assortment on fast-rising distillate and live resin offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.