Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

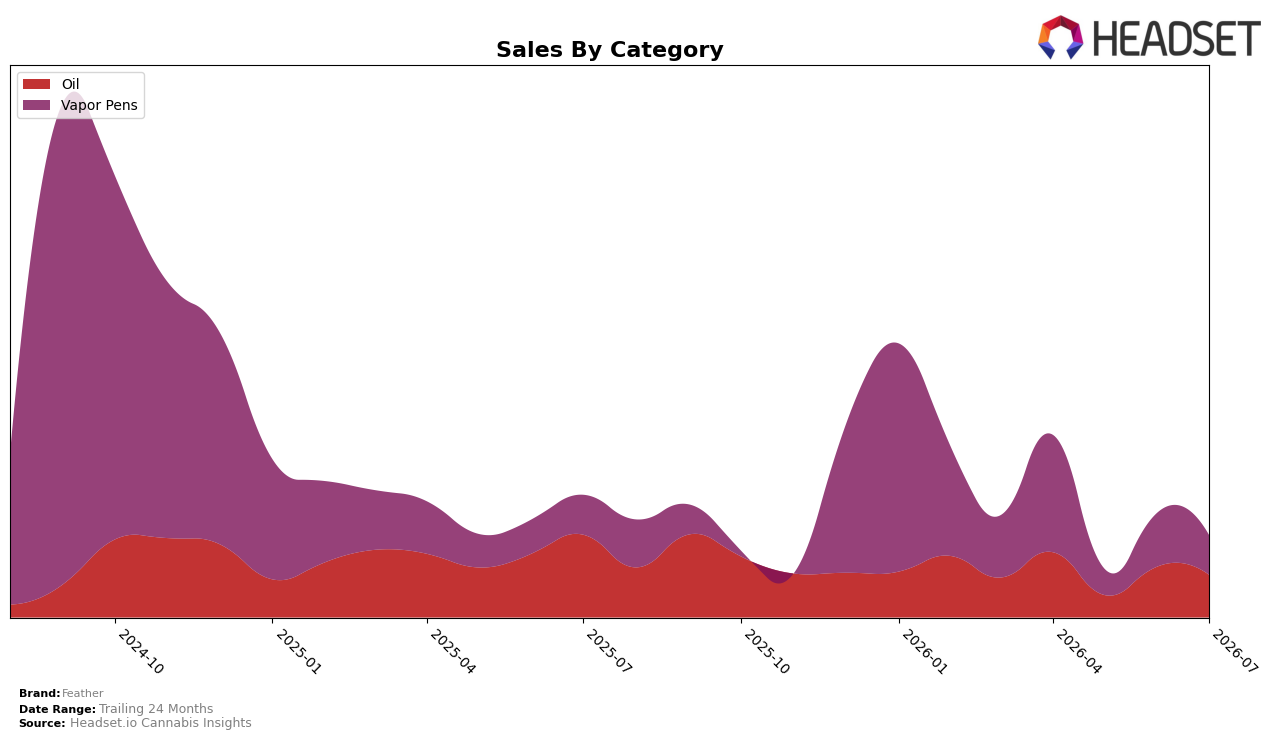

In July 2026, Feather’s mix split nearly evenly between Oil at 51.39% share and Vapor Pens at 48.61% share, but the two moved in opposite ways year over year: Oil fell 42.51% YoY while Vapor Pens slipped just 0.25% YoY. Month over month, both contracted, with Oil down 13.33% MoM and Vapor Pens down 21.81% MoM, indicating a sharper short-term pullback in Vapor Pens despite steadier YoY. With overall brand sales down 27.60% YoY and average price down 8.05% YoY to $33.37, the pattern implies a price-led reset that has not prevented category-level volume erosion, especially in Oil.

The divergence suggests Feather’s positioning remains tied to Oil despite its heavier YoY drag at -42.51% versus -0.25% in Vapor Pens, because Oil still holds the largest share at 51.39% while Vapor Pens’ steeper MoM decline of 21.81% outpaced Oil’s 13.33%. Given Ontario is the top province and the brand’s average price is 10.3% higher in Oil than Vapor Pens ($36.18 vs. $30.84), the mix skews toward a higher-priced but faster-declining pillar, which pressures unit throughput when prices are already 8.05% lower YoY. The implication is that maintaining a majority in Oil without stabilizing its YoY decline, while Vapor Pens experiences sharper MoM volatility, concentrates risk in July 2026 rather than diversifying it.

Competitive Landscape

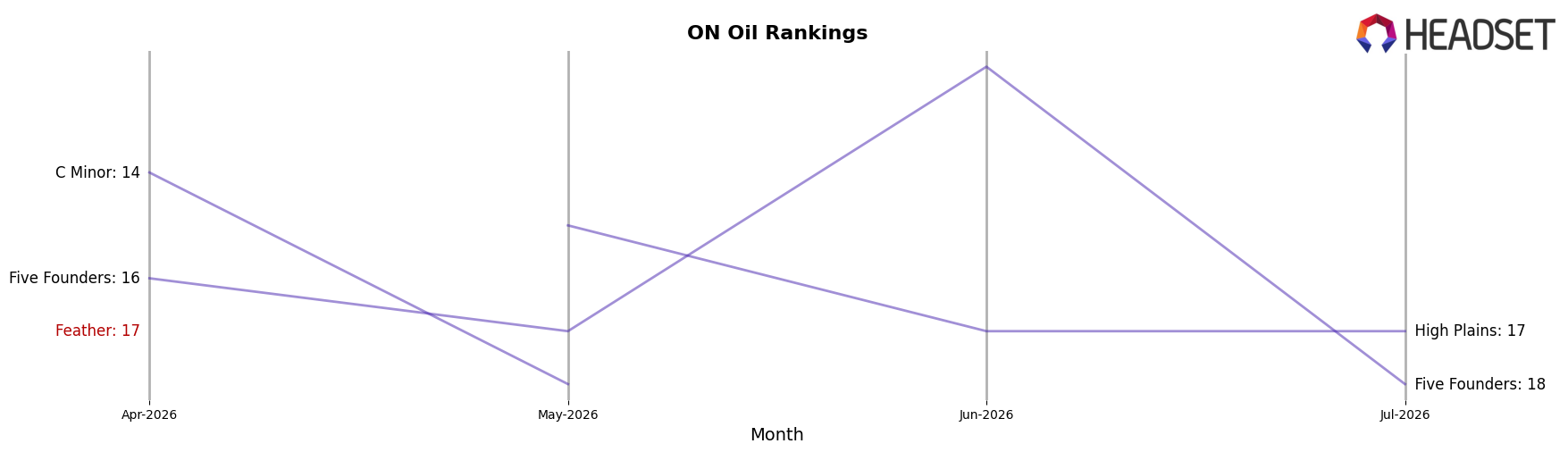

Feather sits at #21 in ON Oil in July 2026, down 3 positions year over year from #18 and 4 spots below its recent #17 placement from April 2026, while still trailing its February 2026 peak of #16; meanwhile, Mod rose from #2 to #1 and Redecan fell from #1 to #2 with a -26.8% YoY sales change, indicating that ladder movement at the top is active even as Feather’s mid-tier position slipped. Against this backdrop, Feather’s 3-position YoY decline to #21 and 5 positions behind the current top three suggest that without a reversal back toward its #16 peak, share will continue to consolidate with leaders and upward movers like ufeelu climbing from #6 to #5; the implication is that Feather’s rank trajectory signals erosion in competitive pull within ON Oil unless it reclaims momentum toward the mid-teens.

Notable Products

Juicy Rouge Distillate Cartridge (1g) posted the largest movement with an 83% month-over-month gain to rank 2 in July 2026, while Blue Mystic Haze Distillate Cartridge (1g) fell 50% to rank 3 and Orange Citrus THC Rapid Spray (8.23ml) declined 55% at rank 4. The top spot remained with THC Dose Control Spray (8.23ml) despite a 5% dip at rank 1, and Hawaiian Smash Distillate Cartridge (1g) dropped 61% to rank 5, indicating volatility concentrated in Vapor Pens where three SKUs sit within ranks 2–5. With four of the top ten as Oil sprays and three as Vapor Pens, the mix shows cartridges are driving swings while Oils anchor share, implying Feather is pivoting toward higher-variance Vapor Pen growth while maintaining an Oil-based floor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.