Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Divvy is stocked at 18 licensed dispensaries across Michigan and Florida, 12 of them in Michigan, with the deepest coverage in Lansing, Adrian, Bay City, Kalamazoo, and Pontiac. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

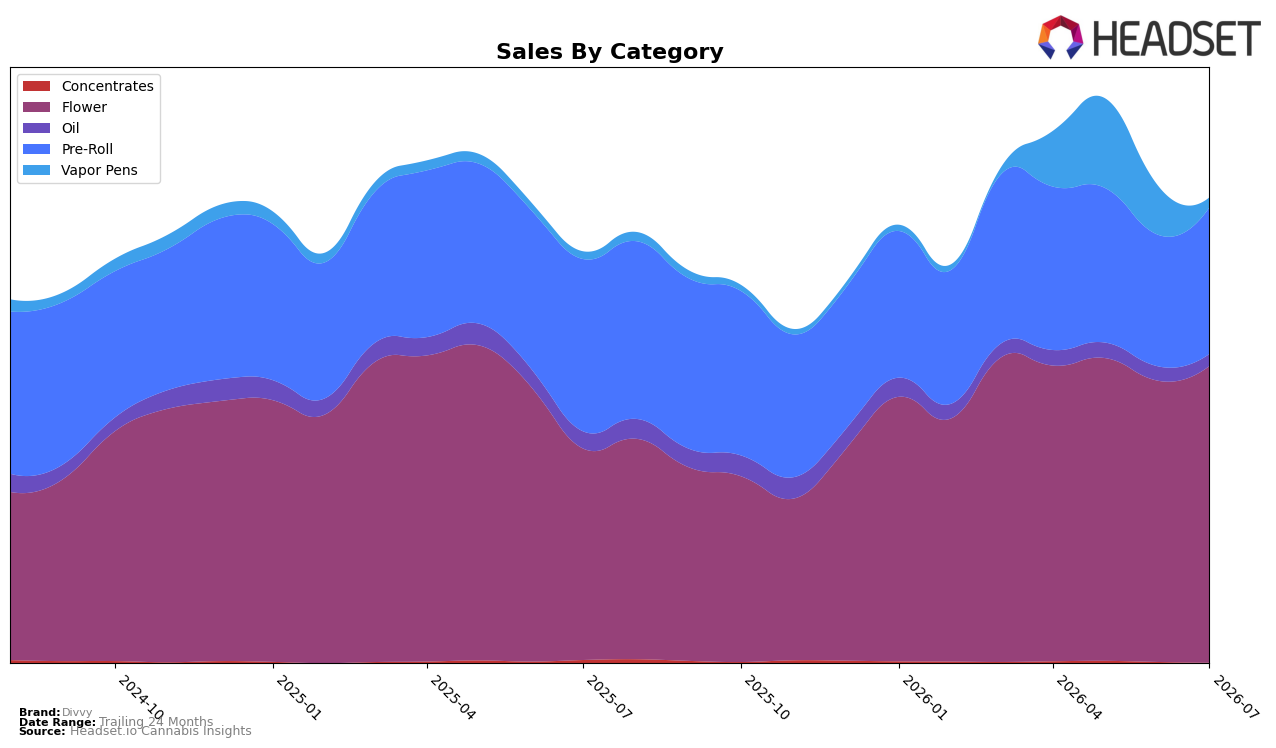

In July 2026, Divvy concentrated 62.93% of sales in Flower with year-over-year growth of 40.06% and month-over-month growth of 5.49%, while Pre-Roll held 31.25% share but declined 14.80% YoY despite an 11.25% MoM lift. Vapor Pens represented 2.45% share with a 24.47% YoY increase but a steep 77.07% MoM drop, and Oil at 2.88% share fell 27.46% YoY and 14.76% MoM; Concentrates at 0.48% share declined 54.63% YoY and 25.62% MoM. Average price fell 22.84% YoY to $16.61 as Flower’s average price sat at 31.34 and Pre-Roll at 8.19, indicating mix-driven volume support even as price compressed; the pattern implies Divvy’s growth is being carried by Flower resilience and a tactical price stance that trades margin for share.

With Flower growth outpacing the brand’s overall 12.85% YoY sales increase and an Alberta Flower rank of 8, the 5.49% MoM gain in the lead category offsets volatility from Vapor Pens’ 77.07% MoM decline and Oil’s 14.76% MoM pullback. Pre-Roll’s 11.25% MoM rebound alongside a 14.80% YoY decline suggests promotional recovery rather than structural expansion, while Concentrates’ 54.63% YoY and 25.62% MoM declines indicate de-prioritization; together, these shifts imply Divvy is consolidating as a Flower-first value player whose pricing and assortment are tuned to defend rank in core Flower while accepting share leakage in fringe formats.

Competitive Landscape

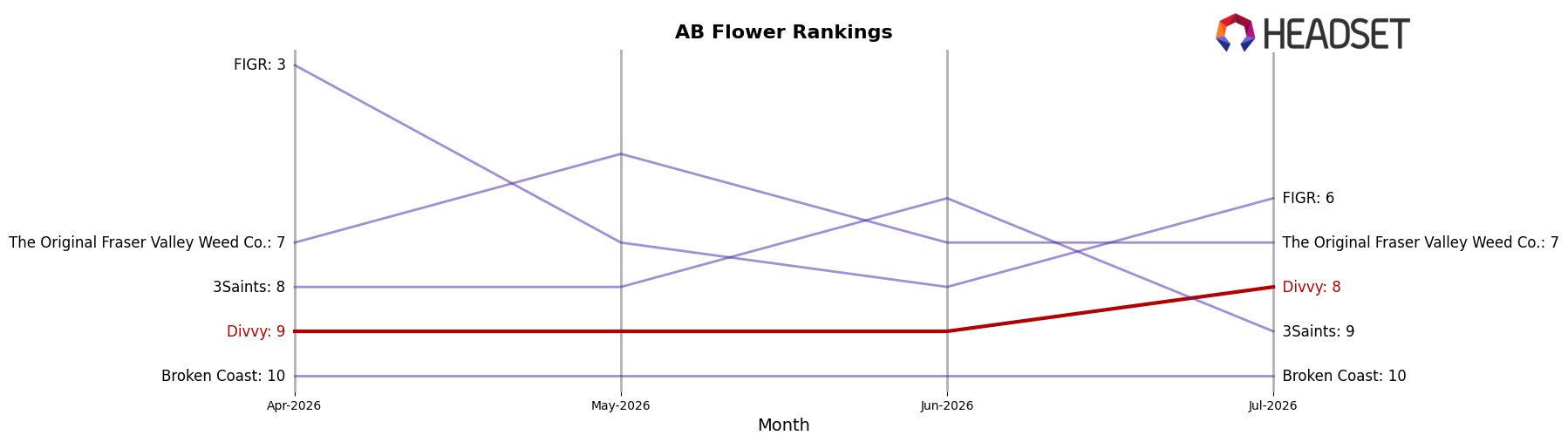

Divvy sits at #8 in AB Flower in July 2026 after rising 5 positions year over year from #13, and edging up 1 place from #9 three months ago; by contrast, Back Forty / Back 40 Cannabis advanced from #2 to #1 while growing sales 11.99%, and Spinach climbed from #7 to #2 with 55.62% YoY sales growth. Divvy’s peak of #7 in March 2026 and current #8, alongside Good Supply sliding from #1 to #5 amid a 43.84% YoY sales decline, indicates Divvy is narrowing gaps in the mid-tier but must outpace faster risers to convert incremental rank gains into durable top-5 presence.

Notable Products

Black Widow Pre-Roll 10-Pack (3.5g) posted the standout movement with a 27.6% month-over-month increase to rank 7, while Roll Up Indica Pre-Roll (1g) climbed 15.7% to rank 2, indicating momentum concentrates within multi- and single-stick pre-rolls rather than shifting toward higher-priced flower. Roll Up Sativa Pre-Roll (0.5g) held rank 1 despite a 2.0% decline, and Roll Up Sativa Pre-Roll (1g) in rank 3 inched up 1.0%, so three of the top five spots are Pre-Roll SKUs, signaling sustained demand density in that format. Flower stayed stable to slightly up — Sour Kush (7g) rose 2.6% at rank 4 and Blueberry (7g) grew 4.2% at rank 6, while Sour Kush (28g) entered at rank 10 with $188,810 — suggesting larger-size flower complements rather than displaces pre-roll strength. The pattern implies Divvy’s near-term mix is tilting toward convenience-led pre-roll units, with value-size flower acting as an anchor rather than the growth engine.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.