Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Find. is stocked at 992 licensed dispensaries across New York, Illinois, and 12 other states, 233 of them in New York, with the deepest coverage in New York, Rochester, Buffalo, Queens, and Albany. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

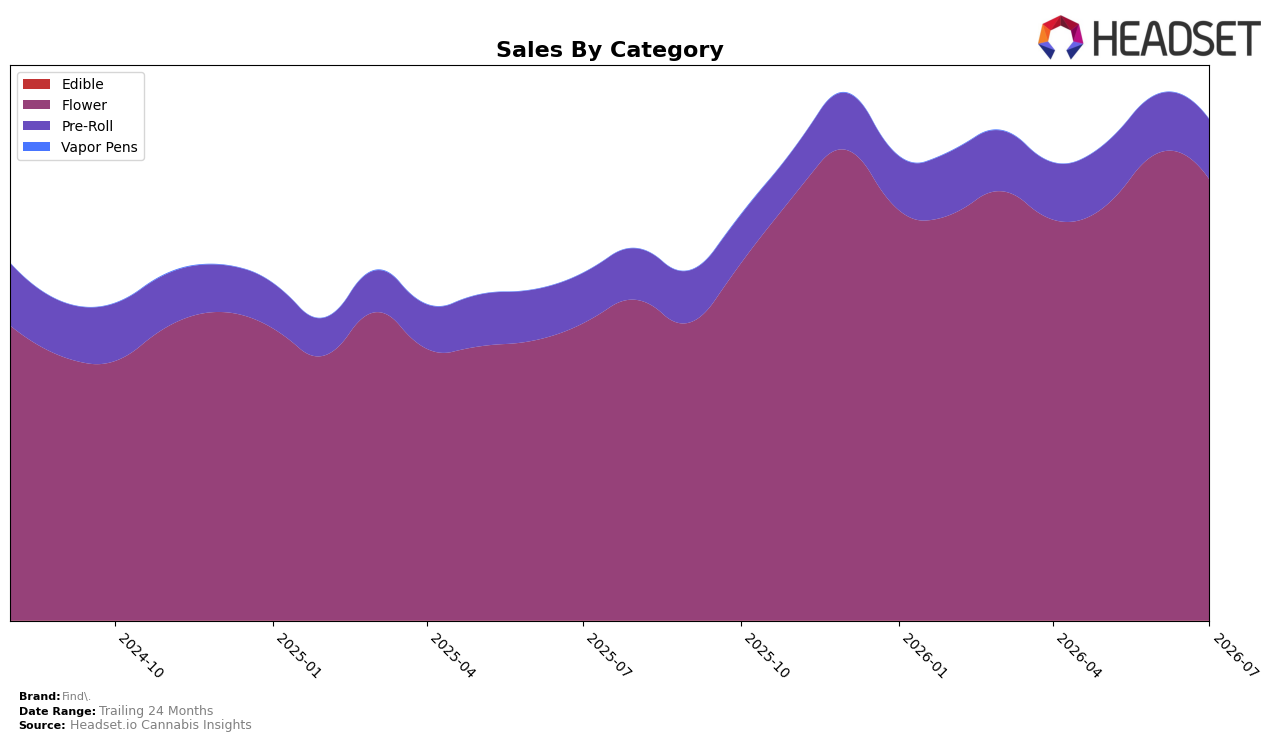

Find.’s mix in July 2026 is concentrated in Flower at 88.08% share with year-over-year growth of 48.41% but a month-over-month decline of 5.66%, while Pre-Roll holds 11.90% share with 19.27% YoY growth and a 1.68% MoM increase. Vapor Pens remain a rounding-error niche at 0.02% share despite a 323.54% YoY spike and a 0.99% MoM lift, indicating scale remains minimal relative to the core. Average price rose 11.40% YoY to $29.01 alongside overall brand sales growth of 44.23% YoY, implying that July 2026 momentum is driven primarily by Flower volume and pricing rather than diversification, and that the small MoM softness in Flower leaves the category mix more exposed to a single pillar.

With Flower ranked 1 in New York and accounting for 88.08% of sales versus Pre-Roll at 11.90%, the brand’s market position is defined by leadership in a single category while secondary formats expand at a slower pace. The 5.66% MoM contraction in Flower against a 1.68% MoM increase in Pre-Roll suggests incremental insulation from mix risk, yet the 48.41% YoY Flower surge paired with a 19.27% YoY lift in Pre-Roll indicates the moat still depends on sustaining Flower throughput and pricing. The pattern implies Find. is optimized for Flower-led share capture now, but future resilience will require translating the July 2026 Vapor Pens growth rate of 323.54% YoY into meaningful share beyond 0.02% so that gains are less sensitive to month-to-month Flower swings.

Competitive Landscape

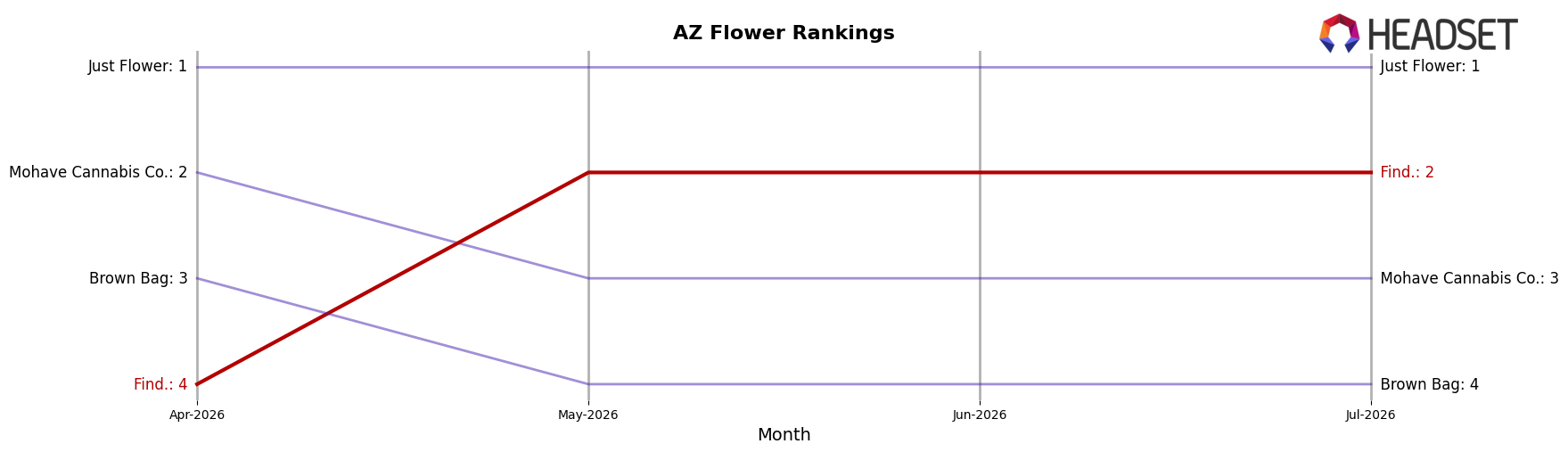

Find. is ranked #2 in AZ Flower in July 2026, unchanged YoY at #2 but improving 2 positions from April 2026 when it sat at #4; the brand’s trajectory contrasts with Just Flower holding #1 with a 21.8% YoY sales increase and Mohave Cannabis Co. at #3 with an 8.9% YoY lift, while Fenix slipped from #4 to #5 alongside a -6.9% YoY decline. Despite peaking at #1 in September 2024 and now sitting one rung lower, the 2-rank climb over the last three months alongside peer churn (e.g., Brown Bag advancing from #5 to #4 with 79.0% YoY growth) implies Find.’s near-term momentum is recovery-driven rather than category-wide lift, setting up a potential but not guaranteed reversion toward its prior #1 peak.

Notable Products

B.A.M. Pre-Roll (1g) delivered the standout movement in July 2026 with a +26.5% month-over-month increase to rank 2, while Jayna's Sunshine Pre-Roll (1g) rose +21.3% and held rank 1, signaling momentum concentrated at the very top of the lineup. Paw Paw Pre-Roll (1g) slipped -3.5% at rank 8 as Atomic Breath Pre-Roll (1g) gained +9.3% at rank 6, and six of the top ten are Pre-Roll SKUs, indicating category density rather than breadth. Nuclear OG (14g) and Hickory Hash (14g) anchored Flower at ranks 4 and 7 with no reported month-over-month change, yet together they set the ceiling on dollar volume with Hickory Hash (14g) at $303,296, suggesting stability in larger-format Flower against faster-moving singles. The pattern implies Find. is skewing toward repeatable Pre-Roll velocity while relying on a few high-cap Flower anchors, a mix that prioritizes traffic and basket starters over expanding variety breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.