Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

High Grade concentrated 89.82% of June 2026 sales in Flower, where year-over-year declined 27.23% and month-over-month fell 30.98%, while Pre-Roll held 6.78% with a 42.46% YoY drop and a 7.64% MoM decline; Concentrates accounted for 3.40% with a 75.41% YoY decrease and a 36.48% MoM contraction. The brand’s average price fell 21.59% YoY to $15.77 alongside a total brand sales YoY decline of 33.81%, and in Arizona Flower the brand sat at rank 23; taken together, the data imply a product mix concentrated in a single category that is shrinking faster MoM than the rest of the portfolio, amplifying overall volatility.

With Flower at 89.82% share and ranked 23 in Arizona, the 30.98% MoM decline in that pillar outpaced the 7.64% MoM dip in Pre-Roll and the 36.48% drop in Concentrates, indicating that near-term performance is chiefly tied to Flower swings rather than diversified buffers. The 27.23% YoY contraction in Flower against a 42.46% YoY decline in Pre-Roll and a 75.41% YoY decline in Concentrates signals a positioning narrowed toward mid-price Flower despite a 21.59% YoY price decrease, implying the brand is competing on price in its core while ceding breadth, which raises exposure to rank pressure at 23 if category headwinds persist.

Competitive Landscape

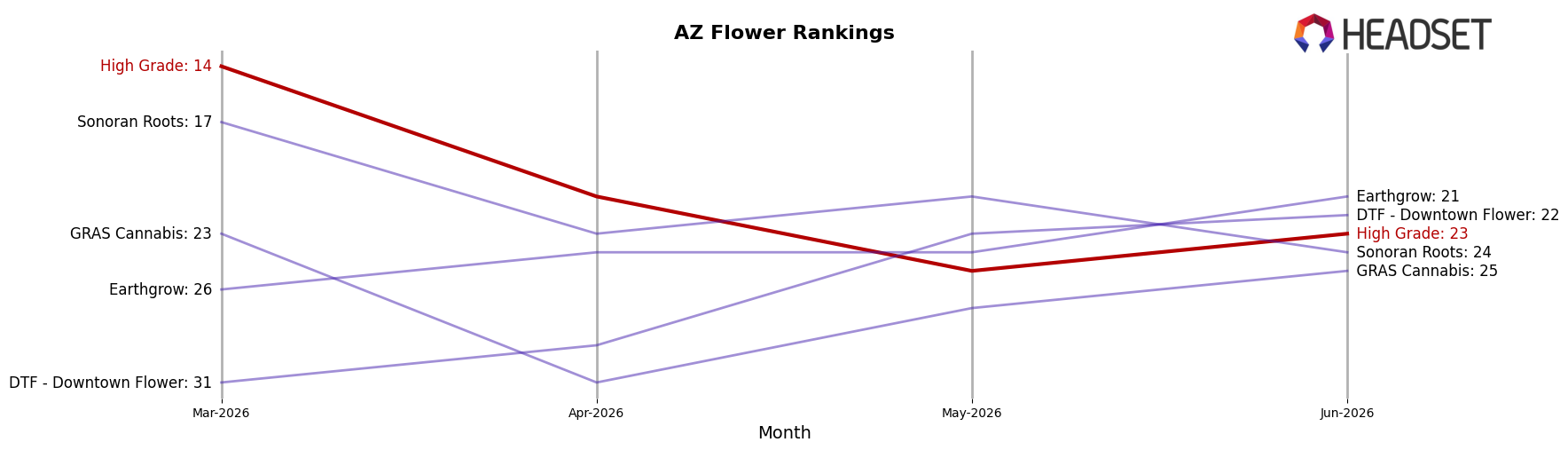

High Grade sits at rank #23 in AZ Flower, down 15 spots year over year from #8, and 9 places below its March 2026 position of #14, even though it once peaked at #3 in June 2024; meanwhile, Just Flower holds #1 with a +13.0% YoY sales change as The Pharm advanced from #5 to #4 on +44.1% YoY sales, indicating that High Grade’s rank trajectory points to share being ceded to faster-rising leaders rather than a temporary dip.

Notable Products

Han Solo Burger Smalls (1g) posted the steepest decline at -62.1% MoM while sliding to rank 6, and Purple Gushers Smalls (3.5g) fell -56.4% MoM at rank 9, signaling acute pressure on smalls. At the top, Astro Kush (3.5g) still held rank 1 despite a -22.8% MoM drop, and Sticky Buns Smalls (Bulk) at rank 2 contracted -15.4% MoM, together indicating leadership is being maintained through share rather than growth. With eight of the top ten coming from Flower and both rank 1 and rank 2 declining, the mix points to over-reliance on Flower smalls that are losing velocity, implying High Grade needs to rebalance toward formats with steadier month-over-month demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.