Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

#Hash is stocked at 160 licensed dispensaries across New York, California, and 5 other states, 61 of them in New York, with the deepest coverage in New York, Queens, Buffalo, Auburn, and Bronx. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

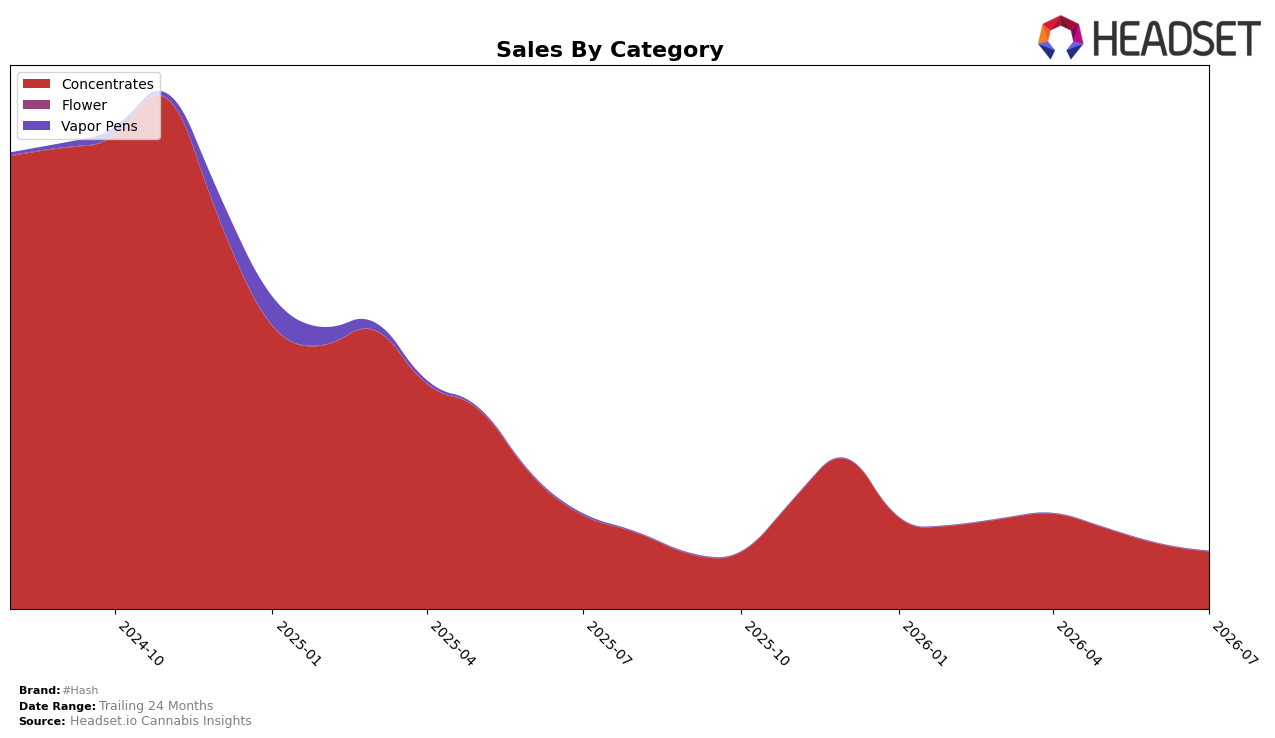

Across categories in July 2026, #Hash concentrated entirely in Concentrates with a 100.0% mix, while sales in the segment declined 38.59% year over year and 11.89% month over month. Average price fell 2.74% YoY to $27.25, coinciding with a brand-level sales decline of 39.32% YoY and an extended 87.50% drop over 24 months; the single-category focus amplified exposure to category-specific headwinds rather than diversifying them.

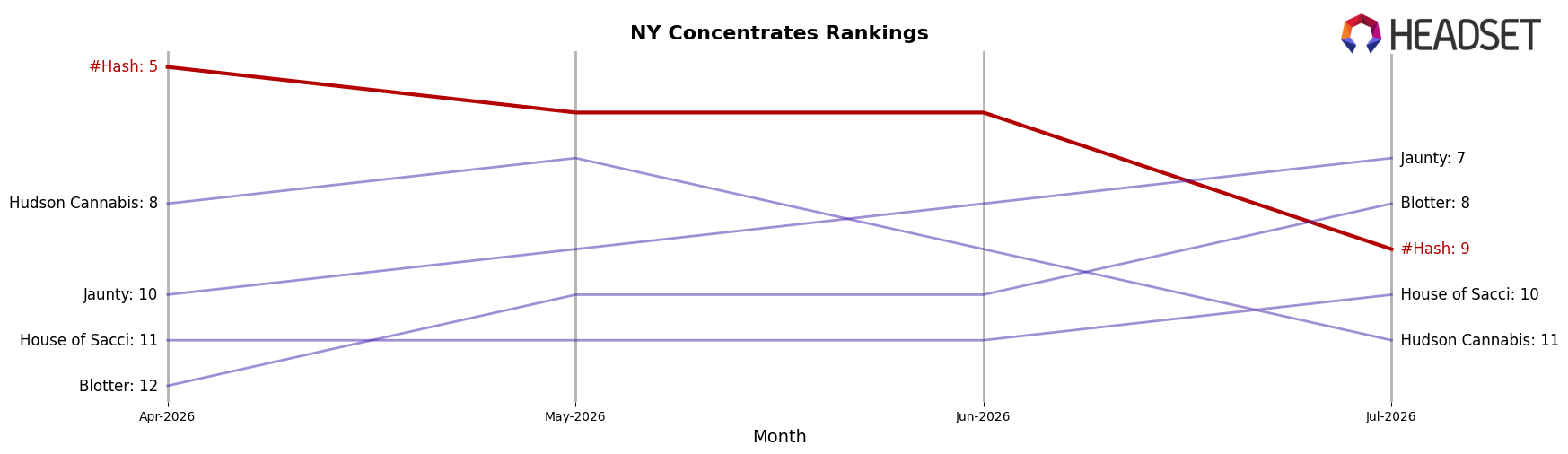

Within New York Concentrates, #Hash held rank 9, which, paired with a 100.0% category dependency and an 11.89% MoM contraction, implies the brand is competing from a mid-tier position that is vulnerable to even small share shifts. The 2.74% YoY price decrease alongside a 38.59% YoY sales contraction suggests price moves are not offsetting demand softness, implying that maintaining rank 9 will require mix or format expansion rather than incremental discounting.

Competitive Landscape

#Hash sits at rank #9 in July 2026, down 1 position year over year from #8 and falling 4 spots from April 2026 when it was #5, while its historical peak was #1 in April 2025; meanwhile, Mfny (Marijuana Farms New York) held #1 with no rank change from last year and Jetpacks climbed from #3 to #2 as UMAMII surged from #27 to #3, indicating that #Hash’s 1-rank YoY slip and 4-rank drop since April 2026 are not just seasonal noise but a share-rotation dynamic where ascending competitors compress mid-tier positions.

Notable Products

Strawberry OG Cookies Budder Wax (1g) set the pace in July 2026 with a +50.6% month-over-month jump to the number 1 rank, while the next largest mover, Sour Fuel Budder Wax (1g), rose +24.4% to rank 9. The only notable pullback near the top was Larry Burger Brittle Sugar Wax (1g) at -9.3% while holding rank 6, contrasted with Orange Cookies Budder Wax (1g) slipping -5.0% at rank 3. With nine of the top ten products in Concentrates and two SKUs tied at rank 3, the pattern points to #Hash leaning into a concentrates-led lineup where rapid winners can be amplified as laggards are pruned.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.