Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Olio is stocked at 418 licensed dispensaries across Colorado, New York, and 2 other states, 171 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Boulder, Aurora, and Grand Junction. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

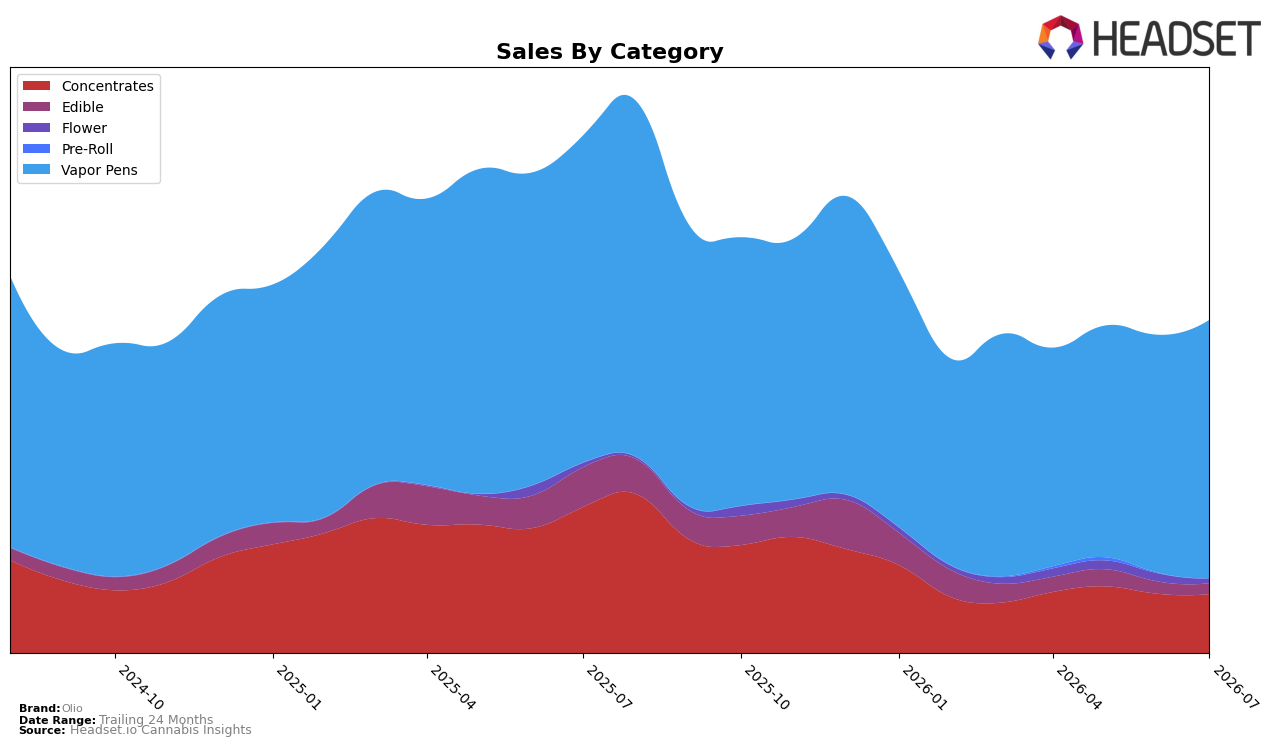

In July 2026, Olio concentrated 77.73% of sales in Vapor Pens, where category sales rose 8.56% month over month but fell 21.12% year over year, while Concentrates held 17.72% share with a 0.56% MoM decline and a 59.72% YoY drop; Edible slipped to 3.20% share with an 11.30% MoM contraction and a 73.04% YoY decline. Flower was 1.26% of mix with a 46.94% MoM decline offset by a 1.95% YoY uptick, and Pre-Roll remained marginal at 0.09% share with a 14.60% MoM decrease; against this backdrop, average price rose 7.54% YoY as total brand sales contracted 35.75% YoY, implying the brand has leaned into higher-price formats while shedding lower-volume, faster-declining segments.

With Vapor Pens anchoring nearly four-fifths of revenue and Colorado rank at 12 in Vapor Pens, the 8.56% MoM lift alongside a 21.12% YoY decline suggests reliance on tactical month-level gains rather than structural category growth, while the 59.72% YoY contraction in Concentrates and 73.04% YoY decline in Edible indicate reduced breadth. Given average price up 7.54% YoY and Flower’s 46.94% MoM pullback despite a 1.95% YoY rise, Olio’s positioning skews toward premiumized pen offerings over multi-category scale, implying near-term share defense within Vapor Pens at the expense of diversification that could limit resilience if pen demand softens further.

Competitive Landscape

Olio sits at rank #12 in CO Vapor Pens in July 2026, down 5 positions from #7 year over year and up 4 positions from #16 since April 2026; versus its historical context, the brand is 5 spots below its peak rank of #7 reached in August 2025 while the category leader mix tightened as Spherex held #1 year over year and Jetty Extracts climbed from #19 to #5 alongside a 181.4% YoY sales lift. With PAX moving up from #3 to #2 on 21.7% YoY growth while Olio slipped 5 ranks YoY but recovered 4 ranks quarter-over-quarter, the pattern implies Olio is stabilizing mid-pack but ceding headroom to faster-movers at the top, making sustained share regain contingent on reversing the year-over-year rank slide.

Notable Products

White Truffle Live Rosin Cartridge (0.5g) posted the standout movement in July 2026 with a +41.8% month-over-month gain while holding rank 1, and Fresh Squeeze Live Resin Cartridge (1g) advanced +29.2% at rank 5, indicating momentum centered in Vapor Pens. Vapor Pens captured six of the top ten SKUs including ranks 1, 2, 5, 6, 7, and 9, and Lemon Head Delight Live Rosin Cartridge (0.5g) sat at rank 2 with $24,422 in sales, signaling that inhalable formats are concentrating share at the top of the lineup. Edibles were steadier but secondary as Sour Cranberry Live Rosin Gummies 10-Pack (100mg) rose +7.5% at rank 3 and Sour Grape Live Rosin Gummies 10-Pack (100mg) increased +11.3% at rank 4, reinforcing that gummies contribute consistency while not altering rank leadership. The pattern implies Olio’s commercial direction is tilting toward premium live rosin and live resin Vapor Pens as the primary growth engine, with gummies acting as a stabilizing second pillar rather than the pace setter.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.