Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Haze & Main is stocked at 23 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Mesa, Tucson, Chandler, and Flagstaff. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

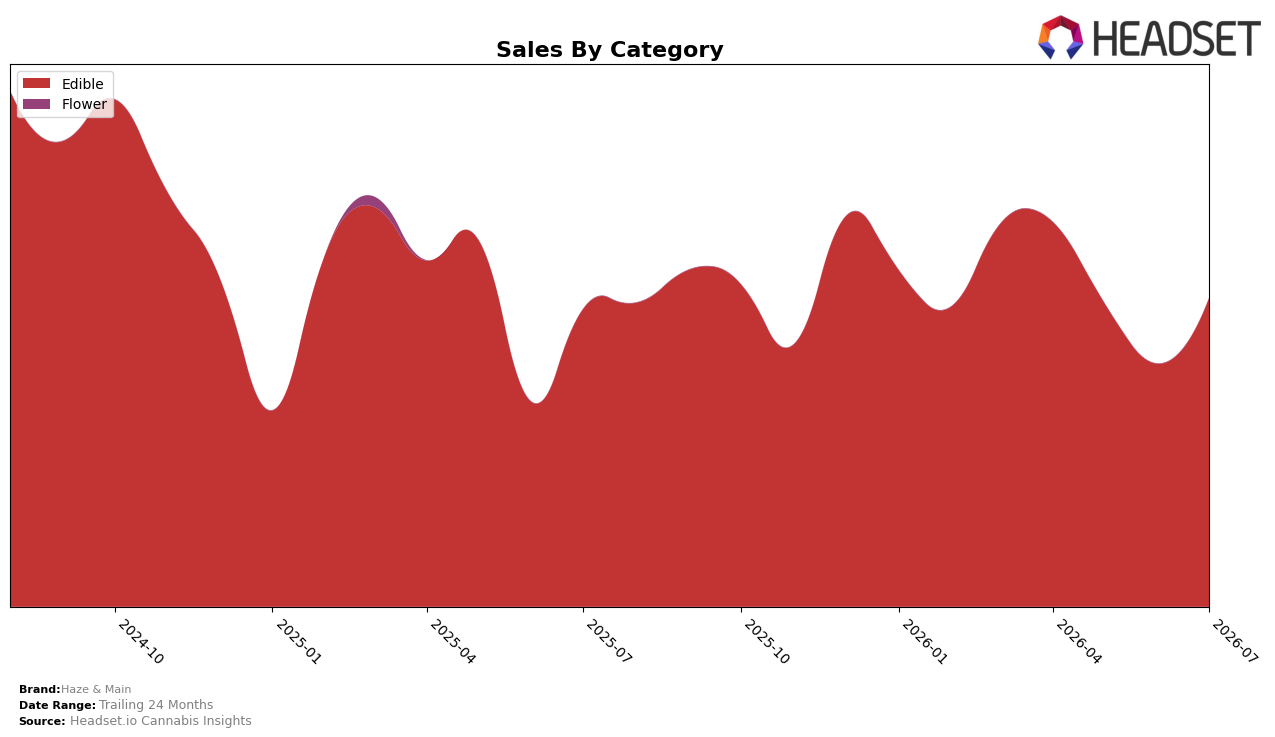

In July 2026, Haze & Main operated as a single-category brand with Edible at 100.0% of sales, pairing a 3.77% year-over-year lift with a 27.09% month-over-month surge while average price fell 25.11% YoY to $14.63. Within Arizona Edibles, the brand sat at rank 24, indicating volume gains were concentrated in one lane rather than spread across formats; the combination of a 100.0% category share and a double-digit MoM upswing implies a tactical pivot to price-led demand capture inside Edibles rather than diversification across categories.

The July 2026 shifts imply Haze & Main is trading mix depth for scale leverage in Edibles: a 27.09% MoM volume acceleration at rank 24 alongside a 25.11% YoY price compression suggests the brand is using price elasticity to climb within Arizona Edibles rather than chasing higher-rank premium tiers. With all sales tied to Edibles and brand sales up 3.77% YoY against a two-year decline of 36.18%, the pattern implies near-term share accumulation via accessible price points, positioning Haze & Main as a value anchor within the Edible set while it rebuilds trajectory from a lower two-year base.

Competitive Landscape

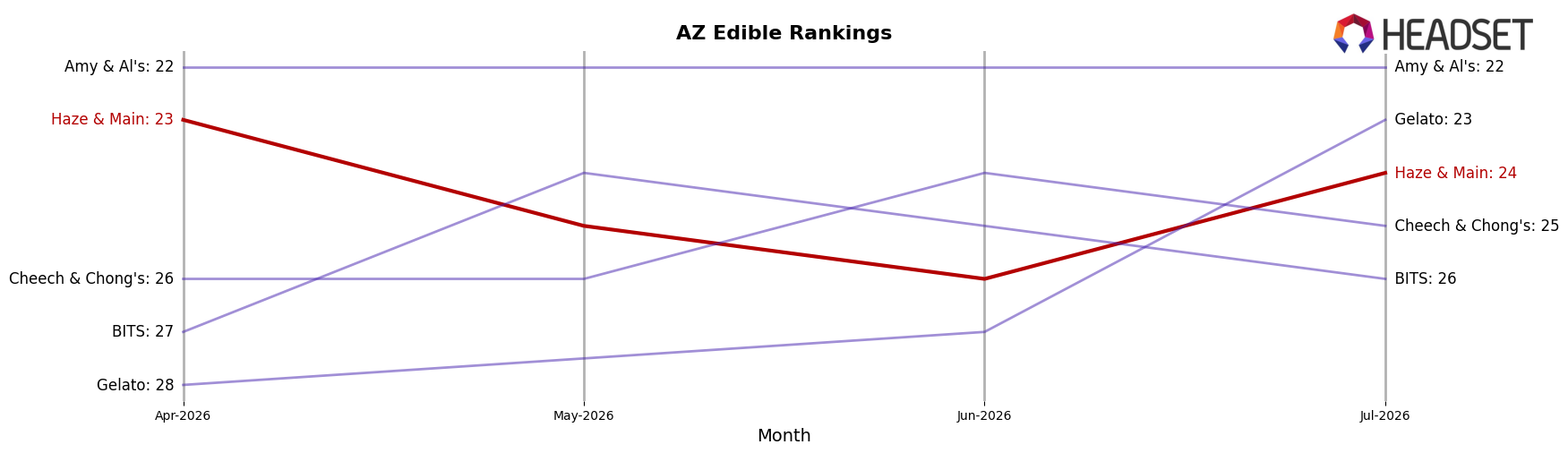

Haze & Main ranks #24 in AZ Edible for July 2026, sliding 2 positions from #22 year over year and down 1 spot from #23 in April 2026, while still 7 places below its peak of #17 from July 2024; meanwhile, Wyld held #1 both year over year and in July 2026 despite a 9.98% sales decline, and Baked Bros climbed from #4 to #3 alongside a 27.68% sales increase, indicating that Haze & Main’s downward rank drift amid a mix of competitor contraction and gains points to share pressure that is unlikely to ease without a change in velocity or distribution.

Notable Products

Milk Chocolate Cacao Fubar Bar 10-Pack (1000mg) posted the largest movement in July 2026 with a +288.9% month-over-month surge to $3,632 and climbed into rank 8, while Dark Chocolate 10-Pack (100mg) fell -28.7% to rank 6 and Dark Plain Chocolate Bar 10-Pack (500mg) dropped -76.1% to rank 9. At the top, Milk Plain Chocolate (100mg) rose +44.5% to hold rank 1 and Milk Plain Chocolate Bar (1000mg) advanced +44.7% at rank 3, whereas Dark Chocolate Fubar Bar 10-Pack (1000mg) declined -16.5% at rank 5. With nine of the top ten rooted in Edible chocolate formats and both 100mg and 1000mg milk SKUs outpacing dark counterparts, the mix indicates a pivot toward higher-dose milk chocolate value packs as momentum carriers and away from multipack dark variants that are ceding rank.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.