Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

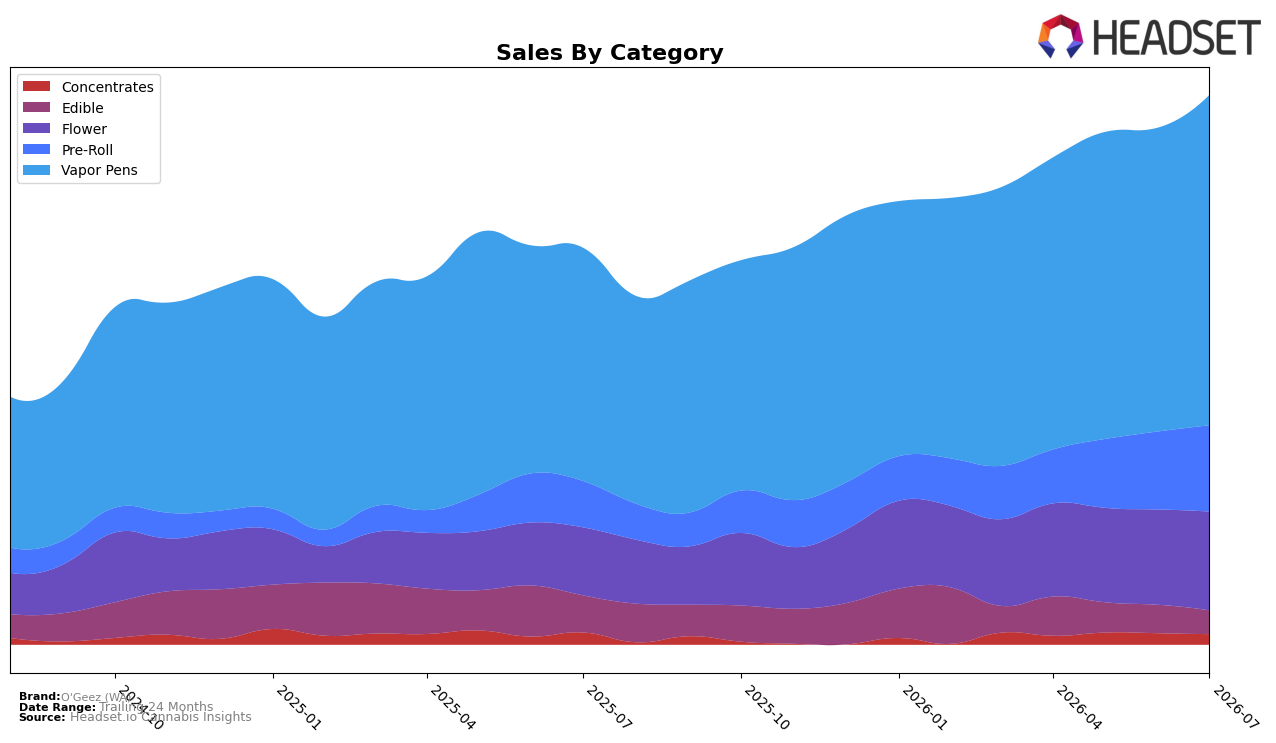

In July 2026, O'Geez (WA) concentrated 53.94% of sales in Vapor Pens with year-over-year growth of 38.39% and month-over-month growth of 8.20%, while Pre-Roll held 16.35% share with a 60.18% YoY surge and 8.40% MoM lift; by contrast, Edible’s 6.72% share contracted with a -23.47% YoY decline and -9.67% MoM slide. Flower accounted for 18.28% share on 35.10% YoY and 3.06% MoM growth, as Concentrates at 4.71% share slipped -5.09% YoY and -2.89% MoM; combined with a -4.20% YoY change in average price to $8.97 and an overall brand sales increase of 30.79% YoY, the pattern points to volume-led expansion anchored in inhalables while ingestibles retrench.

The mix shift toward Vapor Pens at a 53.94% share alongside a category rank of 17 in Washington implies O'Geez (WA) is leaning into scale within a high-velocity format, with Pre-Roll’s 60.18% YoY growth and 8.40% MoM momentum serving as a secondary growth engine; simultaneously, Edible’s -23.47% YoY and -9.67% MoM declines signal deprioritization or misfit with the brand’s current price architecture. With Concentrates down -5.09% YoY and -2.89% MoM and Flower growing at 35.10% YoY but only 3.06% MoM, the implication is a positioning concentrated on accessible, lower-priced inhalables that can sustain share gains, while categories requiring differentiated form factors or higher price points contribute less to near-term competitiveness.

Competitive Landscape

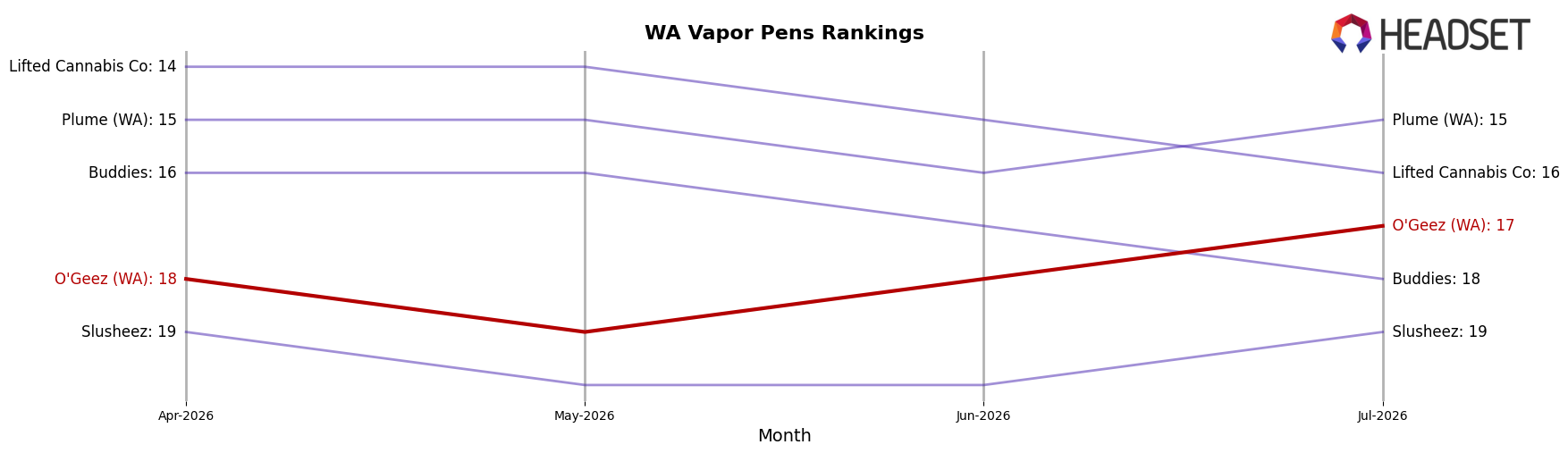

O'Geez (WA) sits at rank #17 in WA Vapor Pens in July 2026, improving 5 positions year over year from #22 while edging 1 position higher versus April 2026’s #18, and it also matches its peak rank of #17 in July 2026, indicating recent momentum from a mid-tier baseline. Against competitors, Crystal Clear rose from #2 to #1 with 12.6% year-over-year sales growth while Mfused slipped from #1 to #2 with a 26.1% sales decline, setting a corridor where O'Geez (WA)’s 5-rank YoY climb coexists with top-tier churn; the implication is that O'Geez (WA)’s rank trajectory points to opportunistic share capture if it sustains gains while incumbents rotate at the top.

Notable Products

CBD/THC 1:1 Strawberries & Cream Gummies 10-Pack (100mg CBD, 100mg THC) slid 10.2% month over month yet held rank 1, while Granddaddy Purple Distillate Disposable (1g) in rank 2 inched up 2.3%, and Pineapple Express Distillate Cartridge (1g) at rank 3 gained 9.8%. Seven of the top ten are Vapor Pens, with ranks 2 through 10 dominated by cartridges and disposables, and mid-pack Vapor Pens rose between 3.8% and 10.7% even as Ice Cream Cake Distillate Cartridge (1g) was flat at -0.2% in rank 9. With the leading Edible down but a deep bench of Vapor Pens growing across ranks 2–8, the mix points to O'Geez (WA) leaning further into Vapor Pens volume while treating the 1:1 edible as a high-dollar anchor at $46,532 that no longer drives growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.