Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Heylo is stocked at 56 licensed dispensaries across Washington, with the deepest coverage in Seattle, Bellingham, Everett, Spokane, and Tacoma. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

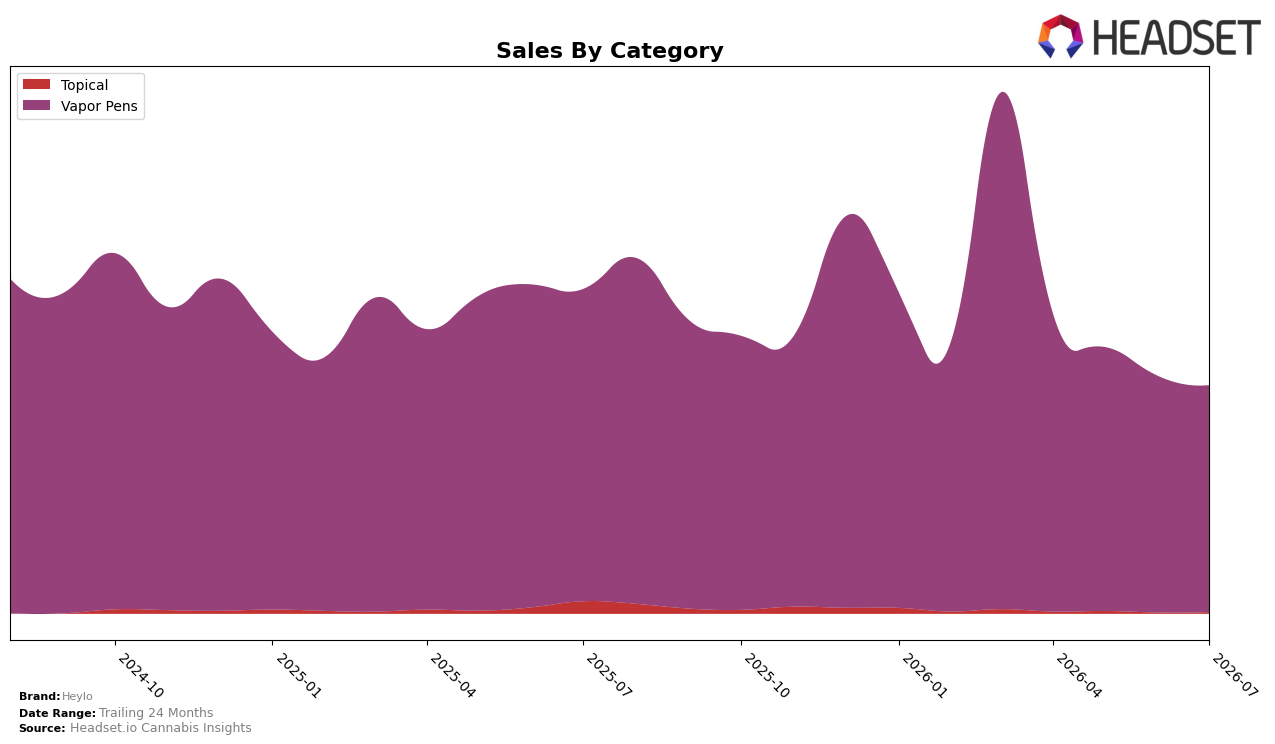

Heylo concentrated 98.59% of July 2026 sales in Vapor Pens, where year-over-year sales fell 27.17% and month-over-month dipped 4.09%, while the residual 1.41% in Topical plunged 76.84% year-over-year but rose 12.00% month-over-month; the average price moved down 2.05% year-over-year to $24.25, indicating limited price relief against volume contraction. In Washington Vapor Pens, the brand sat at rank 85, positioning it deep in the long tail as mix concentration increased, which implies a risk that further category-specific headwinds could disproportionately compress overall sales.

The July 2026 mix pattern implies Heylo is over-indexed to a single growth engine where share gains are unlikely without a shift: with 98.59% exposure to Vapor Pens and a 27.17% year-over-year decline alongside an 85th rank, the path to recovery likely depends on either accelerating share capture within the segment or rebalancing toward niches like Topical that, despite a 76.84% year-over-year drop, posted a 12.00% month-over-month uptick that may signal tactical whitespace. The 2.05% price decrease combined with a 4.09% month-over-month sales decline suggests recent elasticity is weak, so positioning should pivot from price-led tactics to format and portfolio breadth to reduce volatility from single-category swings.

Competitive Landscape

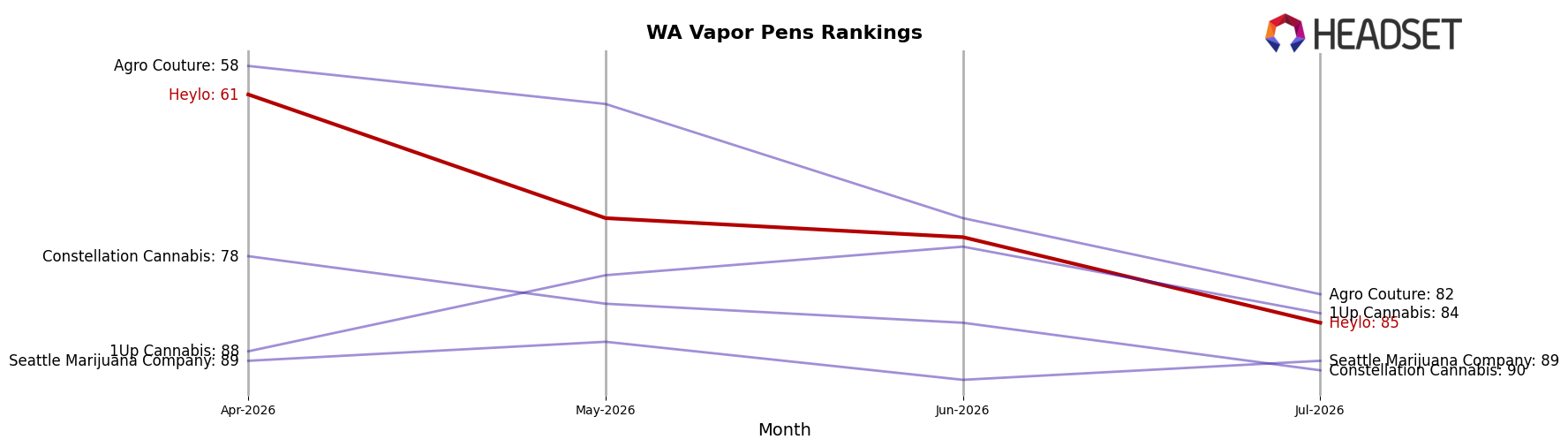

Heylo sits at rank #85 in WA Vapor Pens in July 2026, down 21 positions year over year from #64, and 24 positions below its April 2026 three-month mark of #61; the brand’s peak of #44 in March 2026 underscores a multi-month slide of 41 ranks from peak to current. Meanwhile, Crystal Clear moved from #2 to #1 with 12.6% YoY sales growth, and Full Spec advanced from #6 to #3 with 12.9% YoY growth, while Mfused slipped from #1 to #2 amid a 26.1% YoY sales decline; this mix of upward and downward competitive moves alongside Heylo’s 21-rank YoY decline implies that Heylo is ceding relative shelf presence to faster-rising leaders rather than simply tracking a category-wide contraction.

Notable Products

Wedding Cake CO2 Cartridge (1g) posted the standout move in July 2026 with a 59.4% month-over-month gain to rank 1, while Face Off OG CO2 Cartridge (1g) fell 39.9% and slid to rank 5. Snorlax CO2 Cartridge (1g) advanced 50.3% to rank 4, contrasting with The New Workout Plan RawX CO2 Cartridge (1g) dropping 24.8% at rank 9. With Vapor Pens accounting for all top-10 placements and two RawX-labeled SKUs sitting at ranks 8–9, the pattern points to a pivot favoring core CO2 flavors at the top while experimental or co-branded lines consolidate lower in the chart.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.