Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

SubX is stocked at 143 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellingham, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

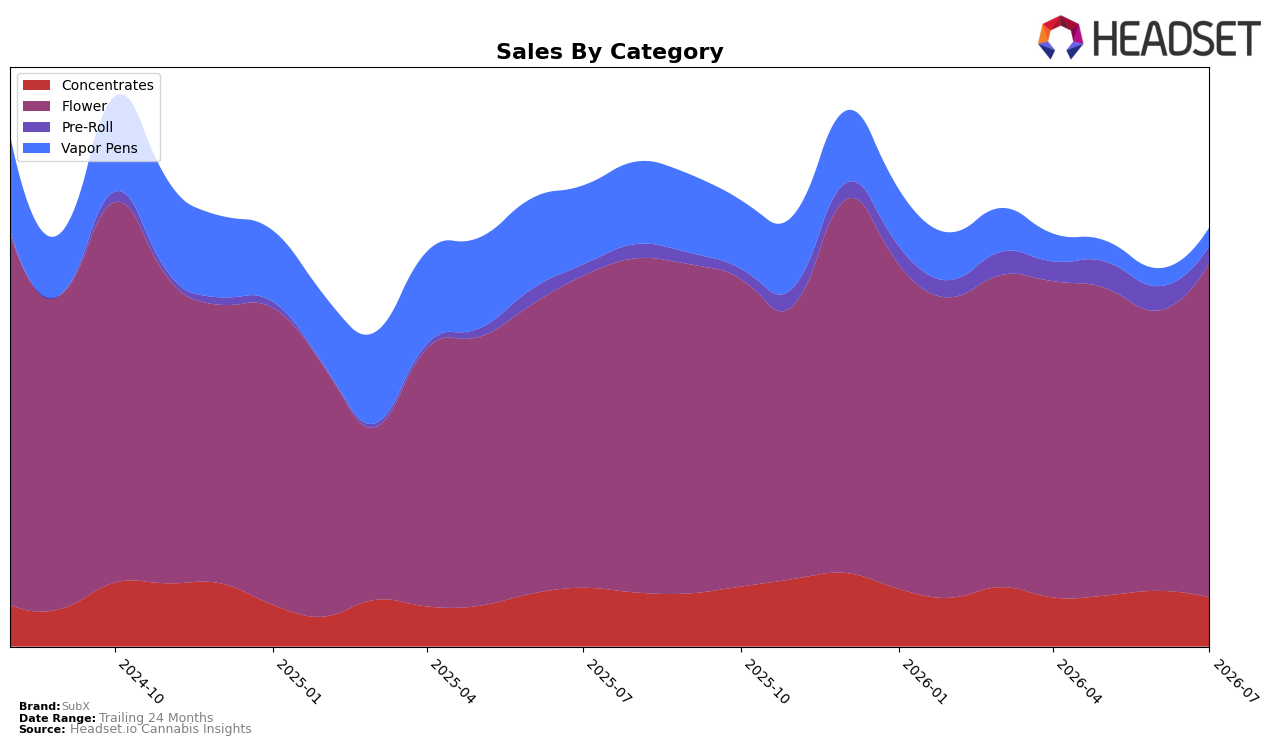

In July 2026, SubX concentrated 74.73% of sales in Flower with year-over-year growth of 7.19% and month-over-month growth of 18.81%, while Pre-Roll held 5.96% share with a 23.14% year-over-year increase but a 21.61% month-over-month decline. By contrast, Concentrates at 12.93% share fell 14.17% year-over-year and 10.18% month-over-month, and Vapor Pens at 6.38% share dropped 67.11% year-over-year despite a 2.07% month-over-month uptick; the overall brand sales declined 8.28% year-over-year as average price moved down 8.57%. The mix indicates SubX’s near-term momentum is carried by Flower’s double-digit month-over-month gain and Pre-Roll’s year-over-year growth, while sustained contraction in Concentrates and Vapor Pens caps total-brand recovery.

With Flower ranked 19th in Washington and commanding nearly three-quarters of mix at an average price of $19.89 versus the brand’s $17.35 overall, SubX is leaning into its highest-ranked, premium-priced pillar as a stabilizer. The simultaneous 18.81% month-over-month lift in Flower and 21.61% month-over-month pullback in Pre-Roll suggest a trade-up dynamic toward core Flower as discount-sensitive segments retreat, while a 67.11% year-over-year decline in Vapor Pens and a 14.17% year-over-year decline in Concentrates point to a narrowing multi-format footprint; together this implies SubX’s positioning is consolidating around Flower-led differentiation, with reduced exposure to volatile extract and pen segments.

Competitive Landscape

SubX is ranked #19 in Washington Flower in July 2026, improving 2 positions from #21 year over year, and matching its rank from April 2026 at #19 while still trailing its peak of #15 from August 2024; by contrast, Phat Panda held at #1 year over year with sales up 18.6%, and Lifted Cannabis Co climbed from #8 to #3 with a 13.1% sales lift. Meanwhile, Sweetwater Farms surged from #14 to #5 on 48.2% growth as Legends stayed at #2 despite a 22.9% sales decline, indicating a market where upward mobility is attainable but concentrated at the top ranks; the flat 3‑month rank at #19 alongside a 2‑spot YoY gain implies SubX has stabilized in the upper‑teens and will need a discrete share capture event to re‑enter the mid‑teens cohort.

Notable Products

GMO (1g) posted the steepest decline at -15.1% MoM while slipping to rank 5, whereas Super Boof (3.5g) surged 48.4% MoM to rank 3; the absence of any MoM change for I95 Cookies (3.5g) at rank 2 points to stability rather than momentum. Four of the top ten are Flower SKUs, led by GMO (3.5g) at rank 1 with +17.7% MoM and $34,987 in July 2026, while Crunch Berries (3.5g) fell 40.4% MoM to rank 9; together these divergences indicate consumer consolidation around a few hero Flower strains alongside pruning of underperforming variants. The pattern implies SubX is concentrating on premium 3.5g Flower formats as volume drivers, while smaller unit sizes and weaker 3.5g entries are being deprioritized to streamline the lineup.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.