Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Dank Czar is stocked at 117 licensed dispensaries across Washington and Nevada, 103 of them in Washington, with the deepest coverage in Seattle, Bellingham, Spokane, Olympia, and Bellevue. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

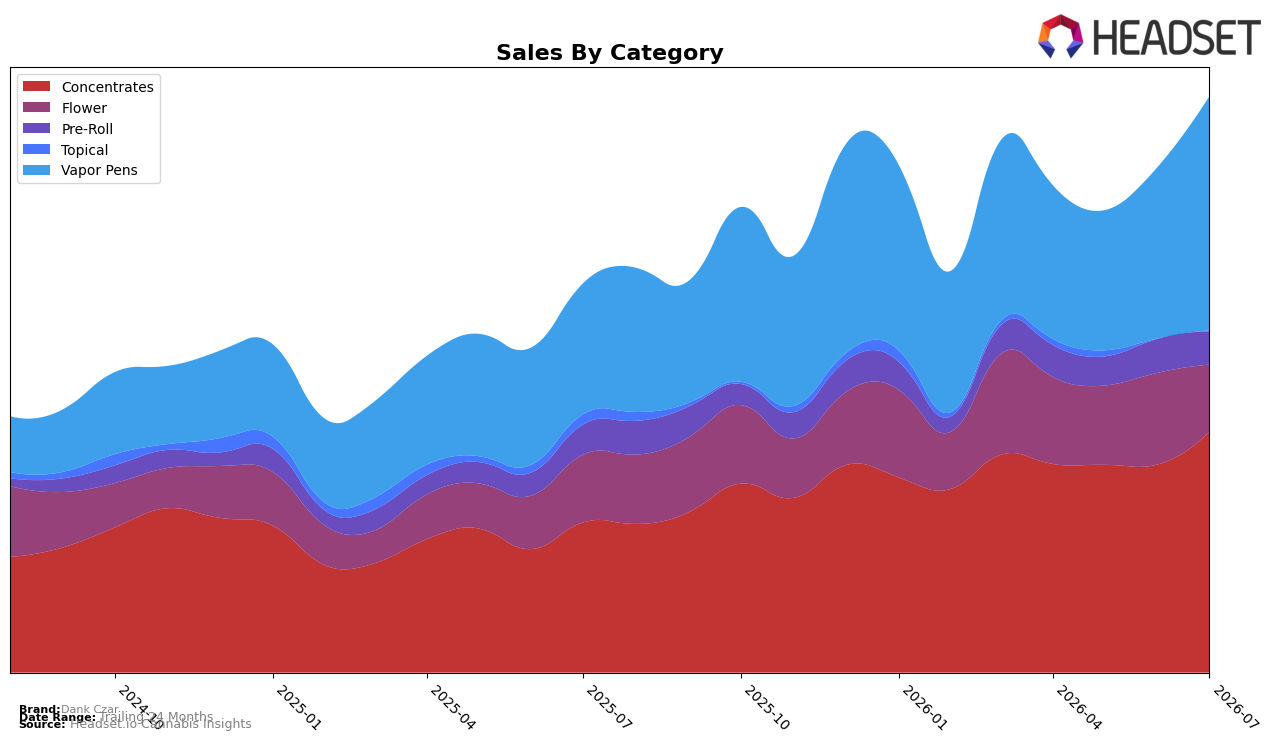

Dank Czar concentrated its July 2026 mix in Concentrates at 40.78% share and Vapor Pens at 39.67% share, with both categories expanding faster than the brand overall YoY at 58.26% and 75.41% respectively while total brand sales grew 44.83%; on a month-over-month basis, Vapor Pens rose 35.06% and Concentrates climbed 15.25%, while Flower contracted 25.19% and Pre-Roll slipped 2.94%. Flower’s YoY change of -0.92% alongside a 7.61% YoY rise in Pre-Roll contrasts with a 55.60% YoY pullback in Topical despite a 20.50% MoM rebound, indicating the growth engine is concentrated in inhalables; with an average price down 16.69% YoY to $11.24, the pattern implies price-supported volume gains are concentrating in Concentrates and Vapor Pens, not in Flower or Topical.

With Concentrates and Vapor Pens now comprising 80.45% of July 2026 sales and improving MoM by 15.25% and 35.06% respectively, the brand’s positioning tilts toward value-forward inhalables where downpricing can scale velocity, while the -25.19% MoM drop in Flower and 55.60% YoY decline in Topical indicate retreat from slower-turn formats; in this context, a 12th-place rank in Concentrates in Washington sets a near-term ceiling that can be moved by leaning further into high-velocity SKUs. Because the average price fell 16.69% YoY even as Concentrates grew 58.26% YoY and Vapor Pens advanced 75.41% YoY, the mix suggests deliberate price elasticity capture rather than broad premiumization, implying that share gains are likelier to come from depth in mid-tier Concentrates and Pens than from recovery in Flower or Topical.

Competitive Landscape

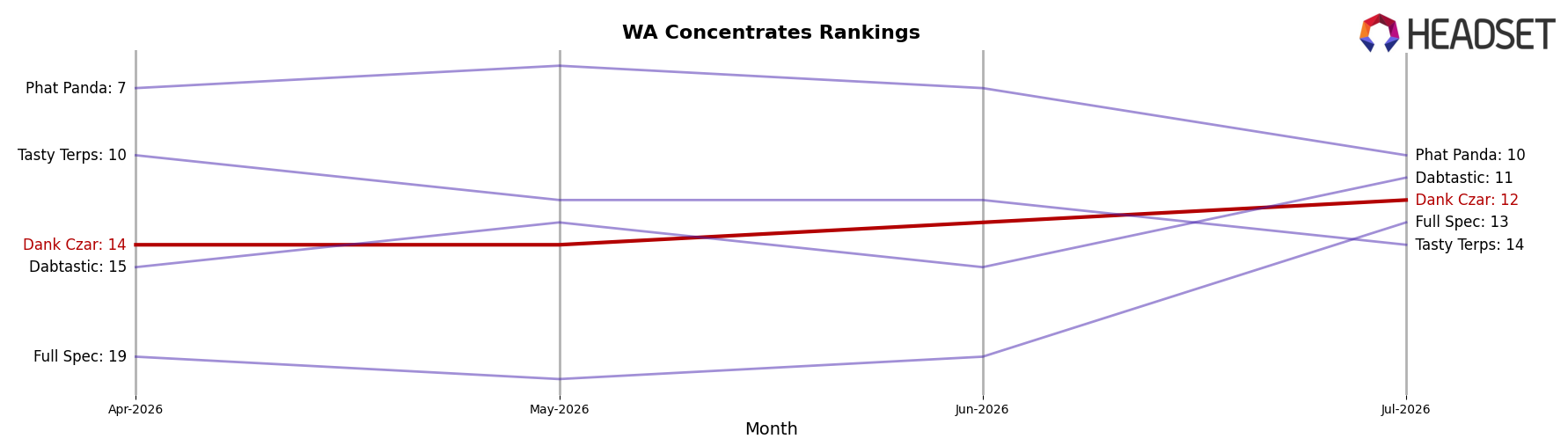

Dank Czar sits at rank #12 in WA Concentrates in July 2026, improving 9 positions from #21 year over year and edging up 2 ranks from #14 three months ago; meanwhile, Ooowee held #1 year over year but posted a -6.9% sales change, and Dabstract rose from #4 to #3 with +5.2% sales growth, indicating Dank Czar’s upward rank mobility is occurring while the category’s top tier is mixed between flat-to-declining leaders and modest climbers, implying the brand’s trajectory toward its peak at #12 in July 2026 positions it to contest the lower end of the top 10 if momentum continues.

Notable Products

Blueberry Banana Bread Flavored Distillate Cartridge (1g) posted the standout move in July 2026 with a 76.8% month-over-month surge to rank 3, while Blue Tangie Live Resin (1g) rose 76.0% to rank 4, indicating momentum concentrated in a few fast-advancing SKUs rather than broad-based lift. Indica RSO Tanker (1g) held rank 1 with a 22.0% MoM increase, outpacing the 25.0% gain that lifted Orange Sherbet Flavored Distillate Cartridge (1g) to rank 2, and five of the top ten are Vapor Pens, signaling skew toward inhalables over Concentrates. With only one raw revenue leader near $5,252 anchoring the spike and ranks 1–4 split between Concentrates and Vapor Pens, the mix implies Dank Czar is leaning into high-velocity flavors and formats to climb share where quick rank gains are still attainable.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.