Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

High Supply / Supply is stocked at 755 licensed dispensaries across Illinois, Massachusetts, and 7 other states, 194 of them in Illinois, with the deepest coverage in Chicago, East Peoria, Naperville, Normal, and Peoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

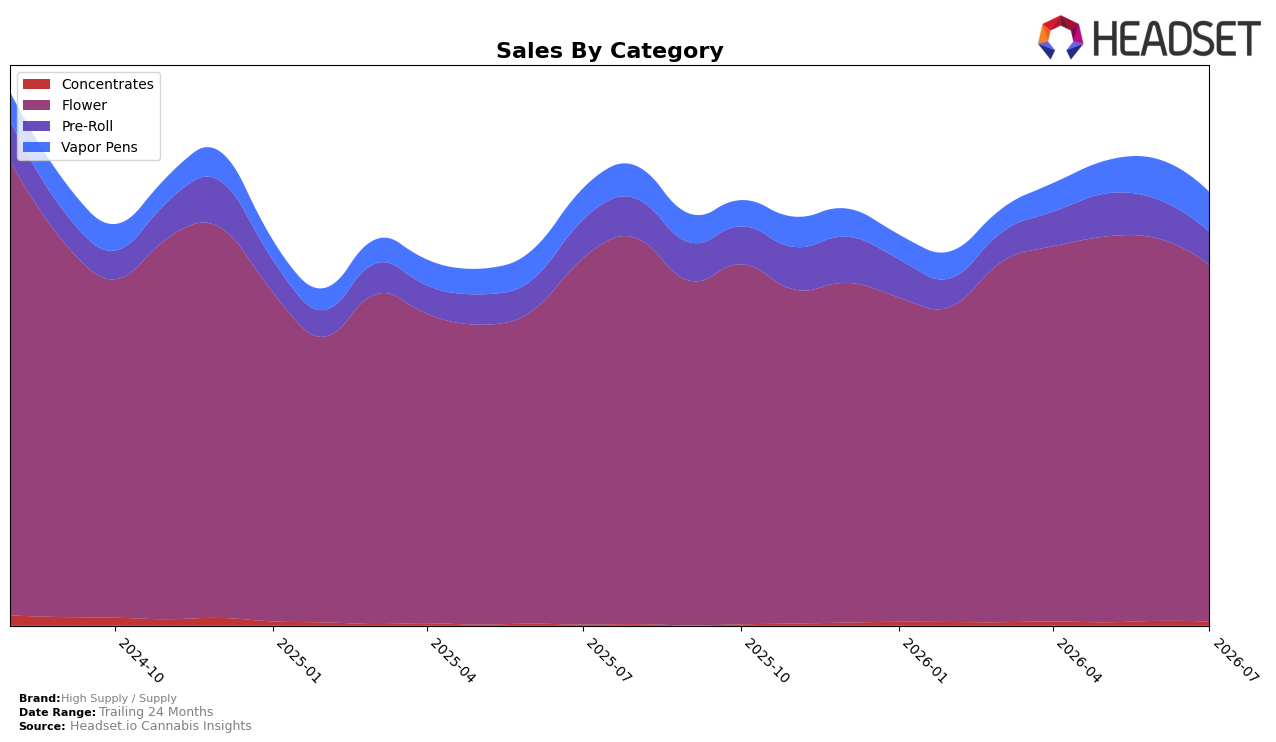

In July 2026, High Supply / Supply concentrated 80.25% of sales in Flower, holding rank 1 in Illinois Flower, while Vapor Pens and Pre-Roll accounted for 9.70% and 8.27% of mix, respectively. Year over year, Flower declined 2.70% and Pre-Roll fell 12.29%, whereas Vapor Pens grew 23.53% and Concentrates rose 61.07%; month over month, Flower slipped 6.73% and Pre-Roll dropped 13.33% as Vapor Pens eased 1.07% and Concentrates dipped 8.01%. With brand-wide sales down 85.66% year over year alongside a 13.30% price decrease, the mix signals overexposure to a softening Flower base and reliance on categories with smaller shares despite faster YoY growth, implying a need to rebalance toward formats with momentum.

The pattern indicates a share-defense posture in Flower paired with exploratory gains in Vapor Pens and Concentrates: a 23.53% YoY rise in Vapor Pens and 61.07% in Concentrates did not offset a 6.73% MoM Flower contraction and a 13.33% MoM Pre-Roll decline. With Flower’s 80.25% share amplifying its 2.70% YoY drop and Vapor Pens’ 9.70% share limiting contribution despite growth, the brand’s July 2026 positioning skews volume toward lower-growth legacy formats while price cuts of 13.30% compress value capture, implying that sustained leadership in Flower requires mix diversification and tighter price-pack architecture to convert category growth pockets into total-brand stabilization.

Competitive Landscape

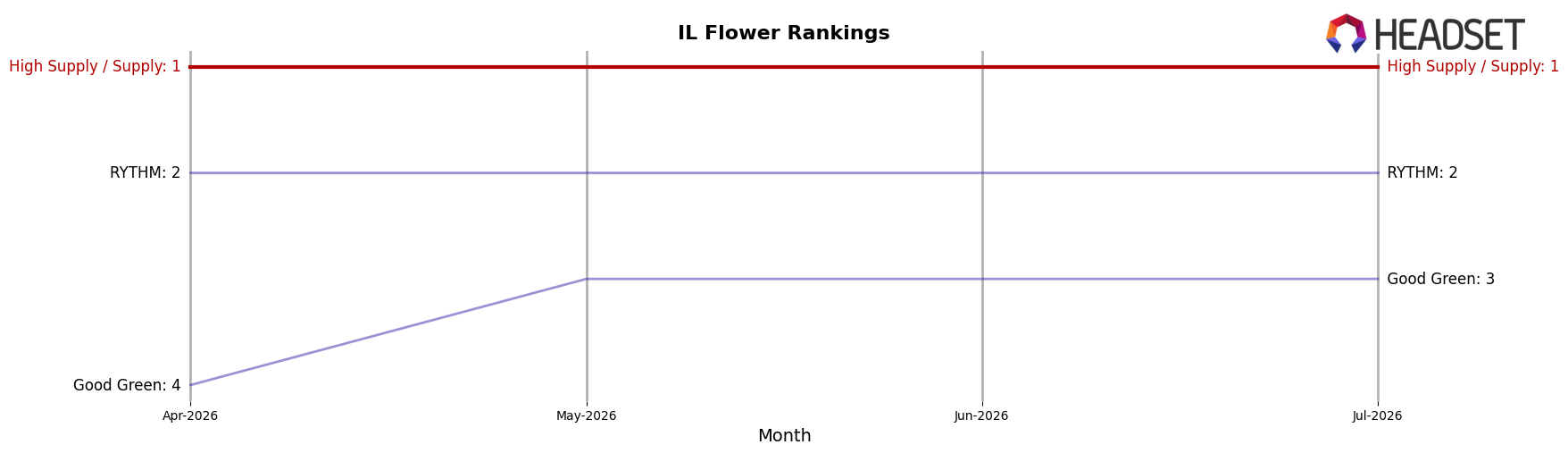

High Supply / Supply holds rank #1 in IL Flower in July 2026, unchanged from #1 in July 2025, while maintaining #1 for the past three months, and hitting its peak rank of #1 in July 2026; in contrast, RYTHM stayed at #2 year over year with sales up 20.8% and &Shine climbed from #8 to #4 with sales up 87.4%, signaling faster challenger momentum even as High Supply / Supply’s position remains static. With Good Green flat at #3 and up 12.7% and Daze Off steady at #5 and up 10.4%, the spread between #1 and the pack is narrowing on growth rates rather than rank shifts, implying that High Supply / Supply’s unchanged #1 trajectory depends on defending share against accelerating mid-pack risers like &Shine.

Notable Products

The steepest decline sits with Gastro Pop Pre-Roll (1g) at -44.9% MoM and rank 7, while The 4th Kind Pre-Roll (1g) also slipped -9.8% at rank 5, signaling Pre-Roll volatility even as Curacao Pre-Roll (1g) rose 10.2% at rank 6. In contrast, Pineapple Under the Sea (7g) climbed 37.4% MoM to rank 1, and Kush Mints Shake (7g) fell -25.1% at rank 8, indicating Flower is bifurcating between premium winners and value formats under pressure. Four of the top ten are Pre-Roll SKUs, but only one posted a double-digit gain while two logged double-digit drops, implying a fragmenting consumer response to strain and format rather than a category-wide tailwind. This pattern implies High Supply / Supply is leaning into a hero Flower SKU while treating Pre-Rolls as tactical, with mix management needed to stabilize value-oriented Shakes and erratic Pre-Roll strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.