Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Highatus is stocked at 486 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, San Francisco, Santa Ana, and Fresno. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

In July 2026, Highatus operated as a single-category brand with Edible accounting for 100.0% of sales, while year-over-year sales in Edible rose 5.27% and month-over-month declined 6.92%. Average price fell 10.71% year over year alongside a current average of $10.30, indicating mix stability but price compression within the sole category. The brand’s statewide Edible rank sat at #10 in California, pairing a 5.27% annual lift with a 6.92% monthly dip to show that demand improvements are not translating into near-term momentum; the pattern implies that Highatus is leaning on pricing to sustain share in Edibles rather than broadening its mix.

The combination of a #10 Edible rank and a 10.71% price decline suggests a value-forward positioning that supports year-over-year growth of 5.27% but leaves the brand vulnerable to month-over-month pullbacks of 6.92%. With 100.0% of sales tied to Edibles and an average ticket of $10.30, the brand’s elasticity is being tested as it trades price for volume, implying headroom to defend rank in California but limited insulation against seasonal or promotional swings; the net effect is a positioning anchored in accessible price points within Edibles rather than diversification or premiumization.

Competitive Landscape

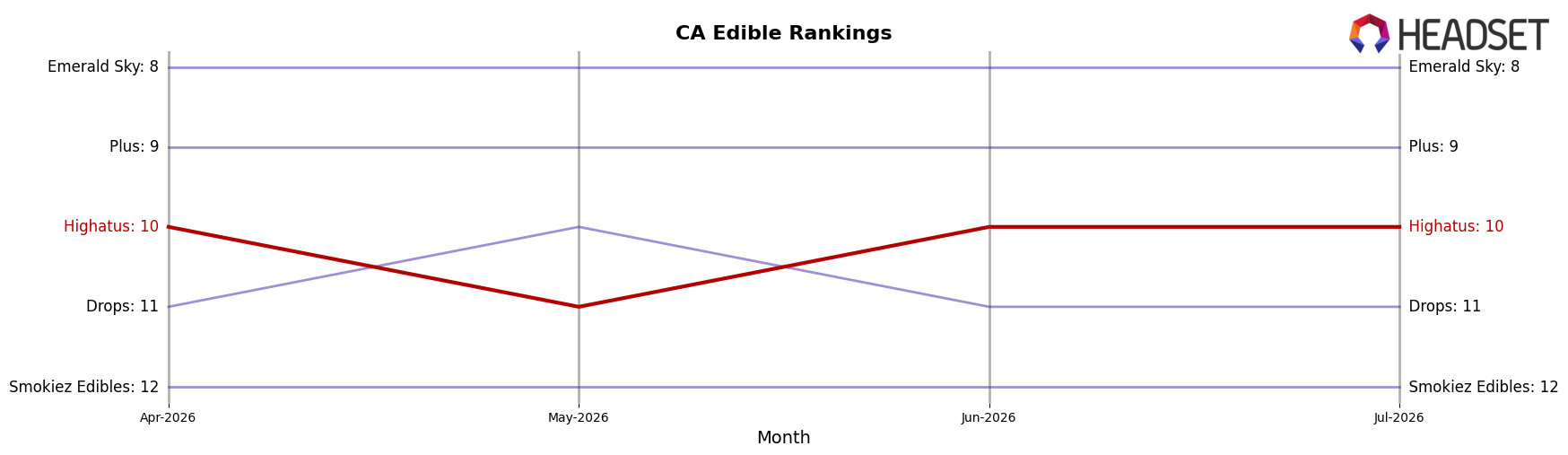

Highatus sits at rank #10 in CA Edible for July 2026, a 1-place improvement from #11 year over year, while holding flat versus April 2026 at #10; this stability contrasts with Wyld staying entrenched at #1 with 2.20% YoY sales growth and Camino holding #2 alongside a 14.77% YoY sales lift, indicating that top-tier momentum is concentrating above where Highatus competes. Highatus’s peak at #9 in February 2026 and current #10 suggest a narrow range, whereas Kanha / Sunderstorm remains anchored at #3 with 14.64% YoY growth and Good Tide holds #5 with 22.07% YoY growth, implying that without a step-change in velocity share Highatus risks being boxed into a persistent #9–#11 corridor.

Notable Products

The steepest decline came from Sour Strawberry Lemonade Gummies 10-Pack (100mg), down 13.4% month over month and holding rank 3 while the THC/CBN 5:1 Pomberry Sour Gummies 10-Pack (100mg THC, 20mg CBN) slid 10.1% at rank 7. At the top, CBN/CBD/THC 1:1:1 Sour Blueberry Gummies 10-Pack (100mg CBN, 100mg CBD, 100mg THC) dipped 4.2% yet stayed at rank 1, whereas the Chron Bons - S'mores Rosin Chocolate 10-Pack (100mg) jumped 19.8% at rank 10, hinting at traction for rosin chocolates despite overall gummy softness. Eight of the top ten are Edible gummies, and the category’s leaders at ranks 1-5 all posted negative MoM shifts between 4.2% and 13.4%, implying a maturation plateau even as niche formats edge up from lower ranks. The pattern implies Highatus is concentrated in gummies that are flattening while premium rosin chocolates begin to contribute incremental volume against a high base near $187,000 for the top SKU in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.