Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

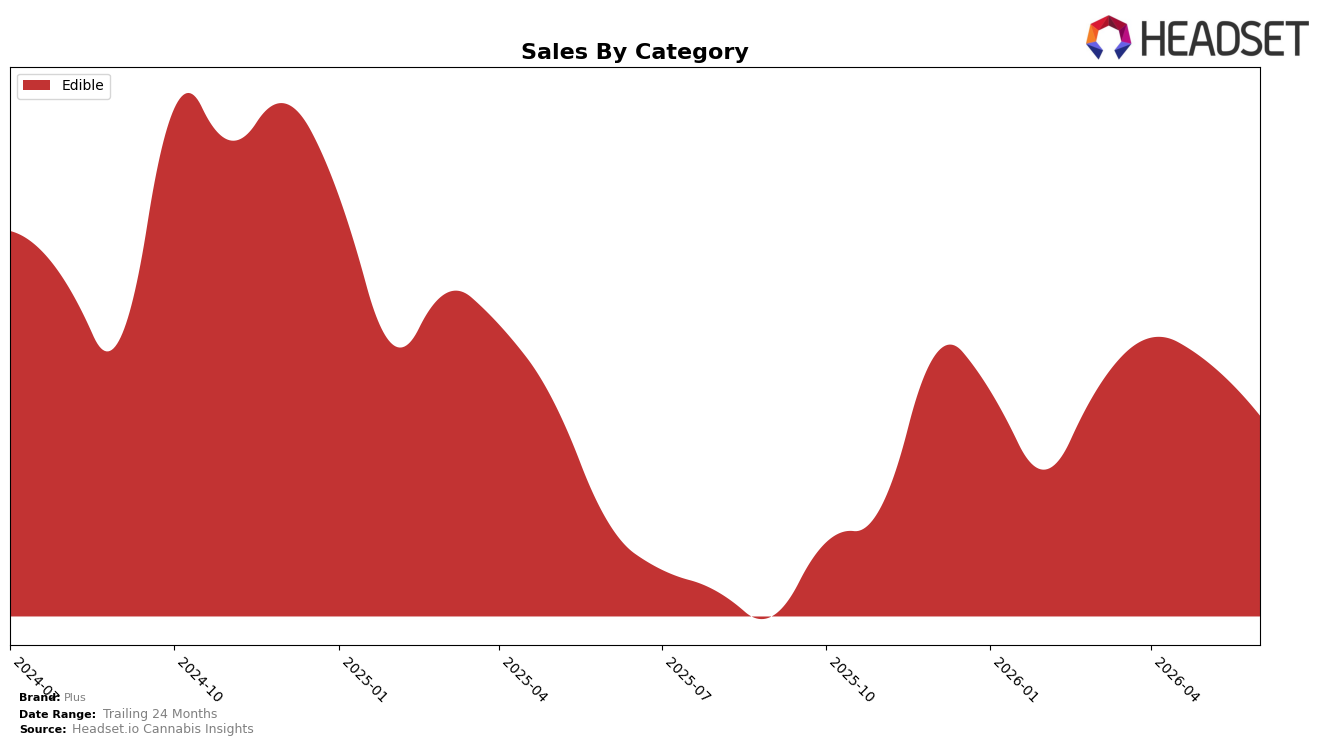

In June 2026, Plus operated as a single-category brand with Edible accounting for 100.0% of mix, posting 10.6% year-over-year growth while declining 4.8% month over month; this combination indicates category concentration with seasonal or promotional pullback against a lower average price that fell 8.9% YoY. The average unit price at $12.39 coincided with a rank of 9 in California Edibles, a placement that tightened versus YoY sales growth but softened versus MoM contraction, implying price-led volume support YoY and demand elasticity pressures MoM.

The pattern implies Plus is leaning into value within Edibles: an 8.9% YoY price decrease paired with 10.6% YoY sales growth suggests price elasticity gains, while the 4.8% MoM sales dip alongside the $12.39 price point indicates promotional timing or assortment gaps that did not sustain month-to-month momentum at a rank of 9. With 100.0% category concentration, maintaining rank in California hinges on converting the price strategy into steadier MoM sell-through, as current mix leaves little buffer if Edible demand normalizes or competitor promotions intensify.

Competitive Landscape

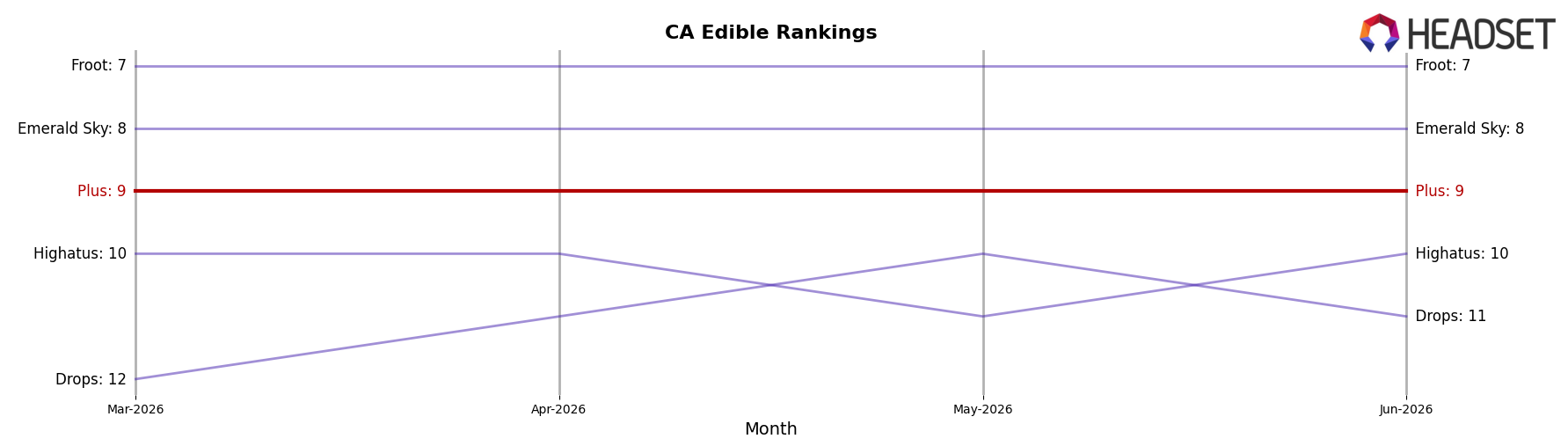

Plus ranks #9 in CA Edible in June 2026, improving 1 position from #10 year over year while holding flat versus March 2026 at #9; this contrasts with Wyld holding #1 year over year with a −1.92% sales change and Camino steady at #2 alongside a +12.91% sales increase, indicating that Plus’s single-rank YoY gain is occurring amid both top-tier stability and mixed momentum above it. With a historical peak of #7 in October 2024 and no movement over the last three months (staying #9), while Good Tide maintains #5 with +28.46% YoY sales and Kanha / Sunderstorm stays #3 with +10.85% YoY sales, the pattern implies Plus is in a holding pattern where incremental share gains are at risk of being outpaced unless it catalyzes movement to break out of the #7–#10 band.

Notable Products

CBD/CBG/THC 20:5:1 Relief Tart Cherry Gummies 20-Pack (400mg CBD, 100mg CBG, 20mg THC) posted the standout move in June 2026 with a +186% month-over-month surge to rank 2, while PLUS Sleep - THC/CBD/CBN 5:1:1 Cloudberry Sleep Gummies 20-Pack (100mg THC, 20mg CBD, 20mg CBN) fell -110% month-over-month to rank 3. Deep Sleep - THC/CBD/CBN 1:1:1 Goodnight Cherry Gummies 10-Pack (100mg THC, 100mg CBD, 100mg CBN) remained rank 1 despite a -26% month-over-month decline, and PLUS + CBD/THC 1:1 Raspberry Rosin Gummies 20-Pack (100mg CBD, 100mg THC) slipped -12% month-over-month to rank 10. With all top-10 items in the Edible category and four Sleep-formulation SKUs clustered across ranks 1, 3, 5, and 6 amid double-digit to triple-digit declines (e.g., -19% at rank 5 and -21% at rank 6), the mix implies a pivot toward daytime relief and functional non-sleep use cases as the primary growth engine.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.