Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Froot is stocked at 539 licensed dispensaries across California, with the deepest coverage in Los Angeles, Long Beach, Sacramento, San Diego, and San Francisco. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

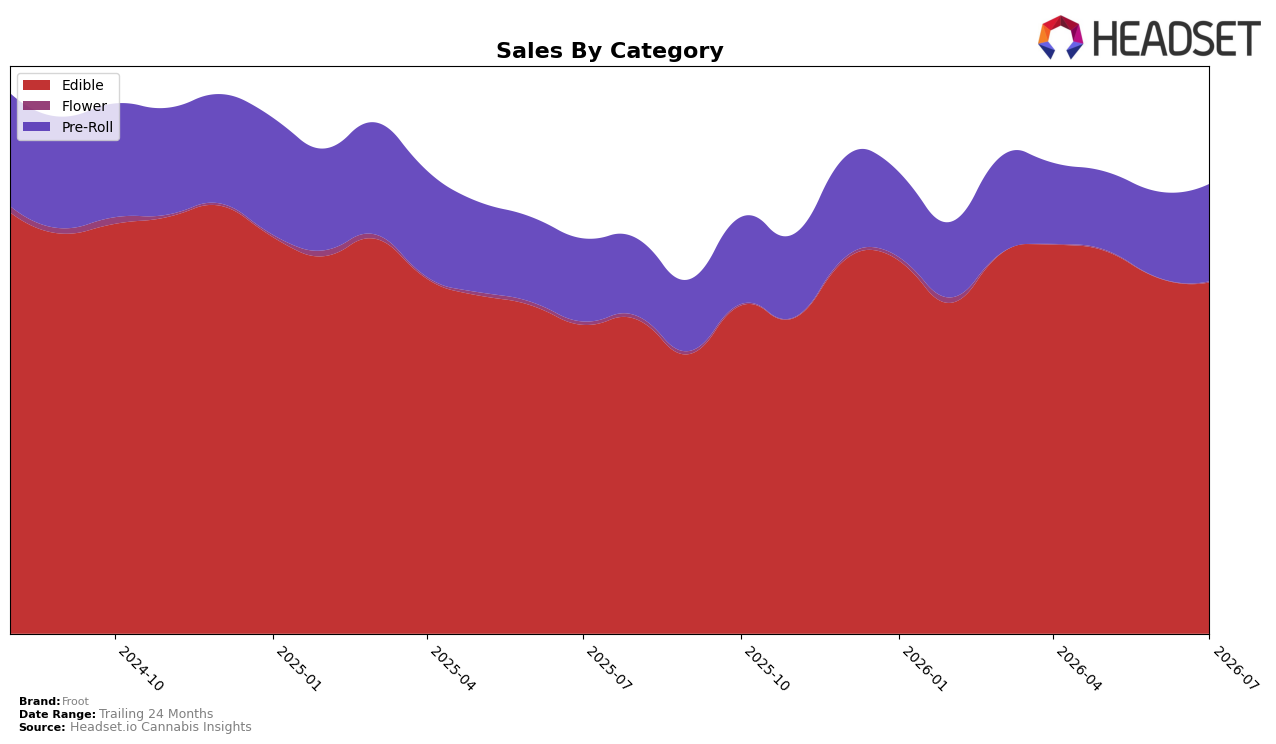

Edible holds 75.84% share with 13.40% year-over-year growth but a 1.24% month-over-month dip, while Pre-Roll sits at 22.25% share with 15.76% year-over-year growth and 12.12% month-over-month expansion; Flower remains a 1.91% sliver with a 19.88% year-over-year decline despite an 8.71% month-over-month lift. The brand’s average price fell 4.56% year over year to $8.80 as total brand sales rose 13.01% year over year, and the Edible rank in California is 7, indicating scale but limited headroom from the category leader tier. The pattern implies Froot is leaning harder into volume-led Edible throughput while redistributing incremental growth to Pre-Roll to offset Edible’s month-over-month softness.

With Edible still supplying three-quarters of sales yet slipping 1.24% month over month as Pre-Roll jumps 12.12%, Froot is quietly rebalancing toward a two-pillar mix where Pre-Roll provides near-term velocity and Edible anchors year-over-year stability at 13.40%. The 4.56% average price decrease alongside 13.01% brand sales growth suggests a deliberate price-to-volume trade that supports rank 7 in California Edibles while creating headroom to build Pre-Roll share above 22.25%; this positioning implies the brand can protect Edible incumbency while using Pre-Roll as the marginal growth engine.

Competitive Landscape

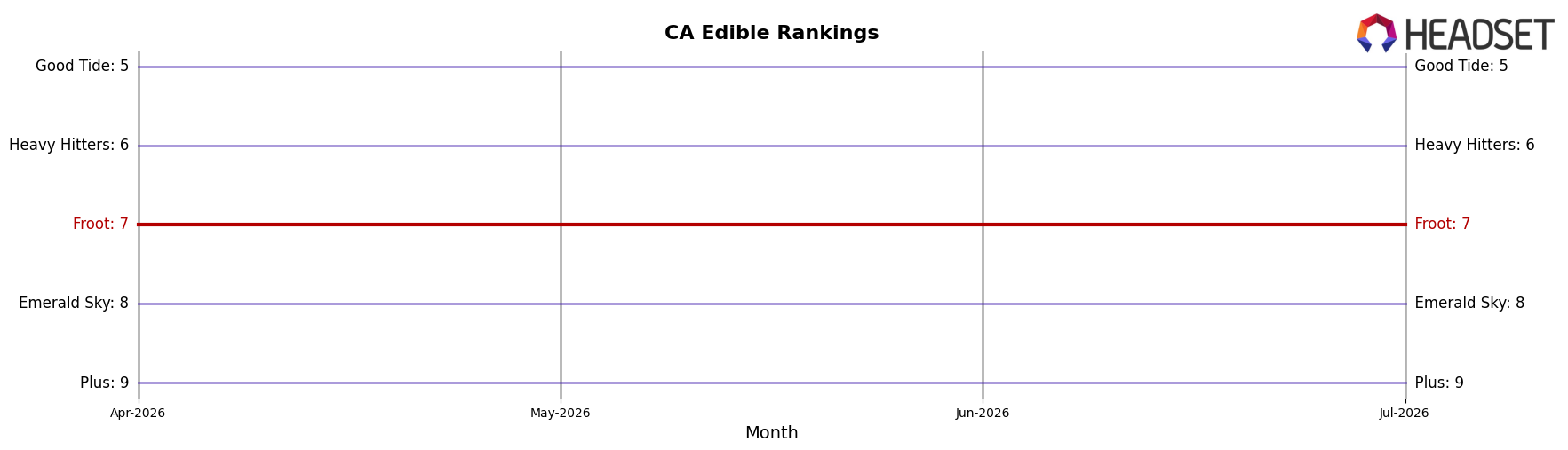

Froot ranks #7 in CA Edible in July 2026, unchanged from #7 year over year, and flat versus its three-month position at #7, while its historical peak was #5 in February 2025; in contrast, Wyld held #1 both this year and last with sales up 2.20% year over year and Camino remains #2 with a 14.77% YoY sales increase, indicating competitors are adding momentum as Froot’s rank stability persists. With Kanha / Sunderstorm steady at #3 and 14.64% YoY growth and Good Tide fixed at #5 alongside 22.07% YoY growth, Froot’s inability to convert its February 2025 peak at #5 into sustained gains suggests that holding #7 amid rivals’ double‑digit growth will likely compress Froot’s path back into the top 5 unless share-accretive moves change the trajectory.

Notable Products

M.Y. Sleep - THC/CBN/Melatonin 5:2:2 Mellow Berry Gummies 20-Pack (100mg THC, 40mg CBN, 40mg Melatonin) posted the steepest decline in July 2026 at -17.7% and slid to rank 7, while Hybrid Blue Razz Dream Chews 10-Pack (100mg) held rank 1 despite a -1.9% dip. Indica Cherry Pie Chews 10-Pack (100mg) jumped 14.9% to rank 2, and CBD/THC 1:1 Peach Gummies 10-Pack (100mg CBD, 100mg THC) was essentially flat at -0.1% at rank 3; across the top ten, all SKUs are Edibles, concentrating 100% of leadership in one category. The top two SKUs together generated about $181,750, indicating consumer pull toward core fruit chews even as sleep-focused formulations retrench. The pattern implies Froot’s commercial direction is consolidating around standard flavor chews with incremental cannabinoid variety rather than specialty sleep blends, prioritizing velocity over niche functionals.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.