Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Highly Casual is stocked at 279 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Monroe, and Lansing. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

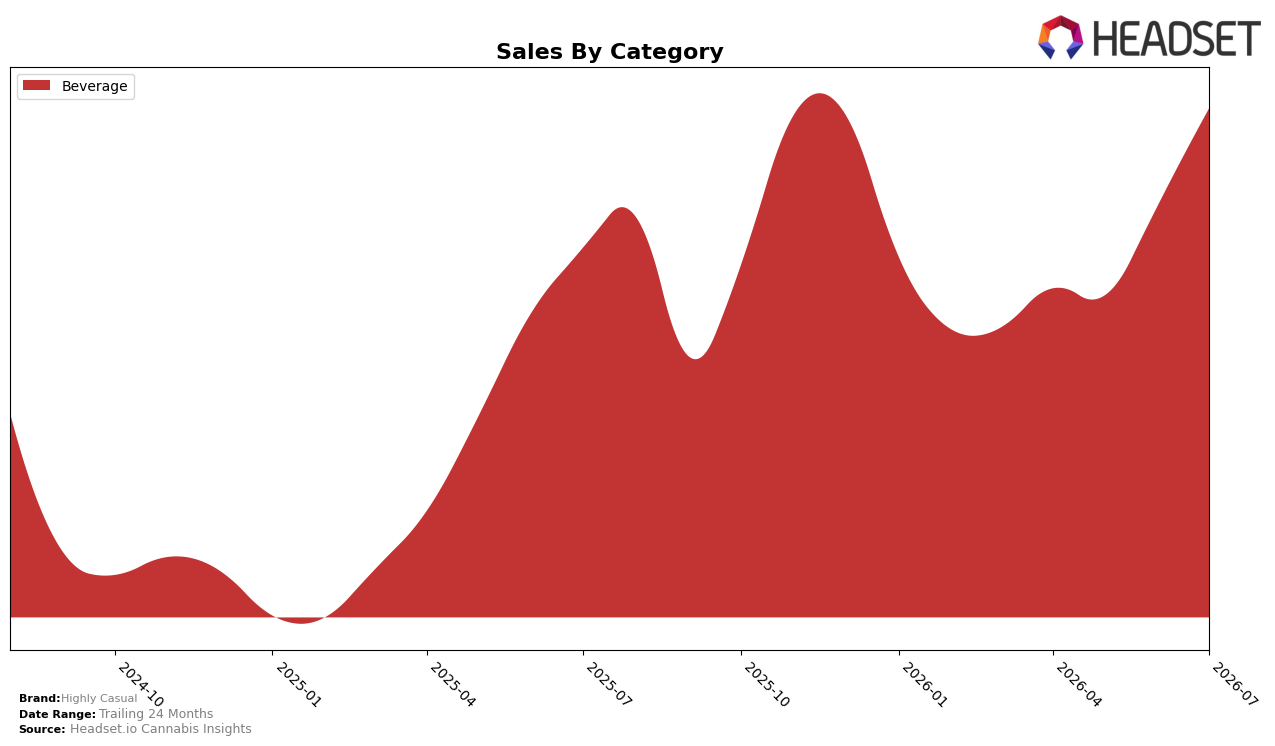

Highly Casual operated as a single-category brand in July 2026 with Beverage at 100.0% of sales share and a rank of 6 in Beverage within Michigan, pairing 21.96% year-over-year growth with a 14.42% month-over-month lift. The average price fell 9.53% year over year to $4.19 while sales expanded 21.96%, indicating volume gains outweighed unit price compression; the same period delivered a 69.37% increase versus 24 months prior alongside a July 2026 rank position of 6. The pattern implies Highly Casual is trading price for velocity within Beverage and consolidating category focus to defend a mid-tier rank despite discount-driven dynamics.

With 100.0% of mix in Beverage and a July 2026 rank of 6, the 14.42% month-over-month rise coupled with a 9.53% price decline suggests tactical pricing is expanding unit throughput faster than peers holding price. The 21.96% year-over-year gain against a flat category mix and a 69.37% two-year expansion point to a volume-led strategy that prioritizes share-of-voice within Beverage over diversification; this positioning implies near-term gains are tied to maintaining sub-$4.19 price points while seeking marginal rank improvements from 6 through incremental distribution or pack-size engineering.

Competitive Landscape

Highly Casual sits at #6 in MI Beverage in July 2026 with a 0-rank YoY change from July 2025 and a 0-rank change versus April 2026, despite previously peaking at #3 in December 2025; meanwhile, Mary Jones holds #1 with a 0-position YoY change and +21.6% YoY sales, and Keef Cola is #2 with a 0-position YoY change but −3.6% YoY sales. The mid-tier is compressing as Chill Medicated jumped from #9 to #3 with +205.4% YoY sales and CQ (Cannabis Quencher) climbed from #8 to #4 with +128.0% YoY sales, while Pleasantea remains stable at #5 with a 0-position YoY change and +23.3% YoY sales; this pattern implies Highly Casual’s flat #6 rank is a share-erosion risk if momentum brands continue upward and incumbents at #1–#2 hold position.

Notable Products

Blueberry & Pineapple Seltzer (2mg THC, 12oz, 355ml) posted the largest month-over-month gain at 117.3% and entered the top ten at rank 8, while High 5 - Fruit Punch Seltzer (50mg THC, 12oz, 355ml) fell 13.6% to rank 6, indicating a swing toward lower-dose options over high-potency formats. Honeycrisp Apple Hang Ten Seltzer (10mg, 12oz, 355ml) held rank 1 with a 7.3% lift as CBD/THC 1:1 Lemon + Lime Seltzer (5mg CBD, 5mg THC, 12oz, 355ml) surged 81.2% to rank 4, signaling that balanced 1:1 profiles are accelerating within the leaders. With all top-10 SKUs in Beverage and four 1:1 seltzers occupying ranks 2–4 and 10, July 2026 concentration in sessionable and balanced drinks points to Highly Casual prioritizing breadth in approachable, lower-dose formats over a single high-THC anchor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.