Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Hitz Cannabis is stocked at 117 licensed dispensaries across Washington and California, 101 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Everett, and Olympia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

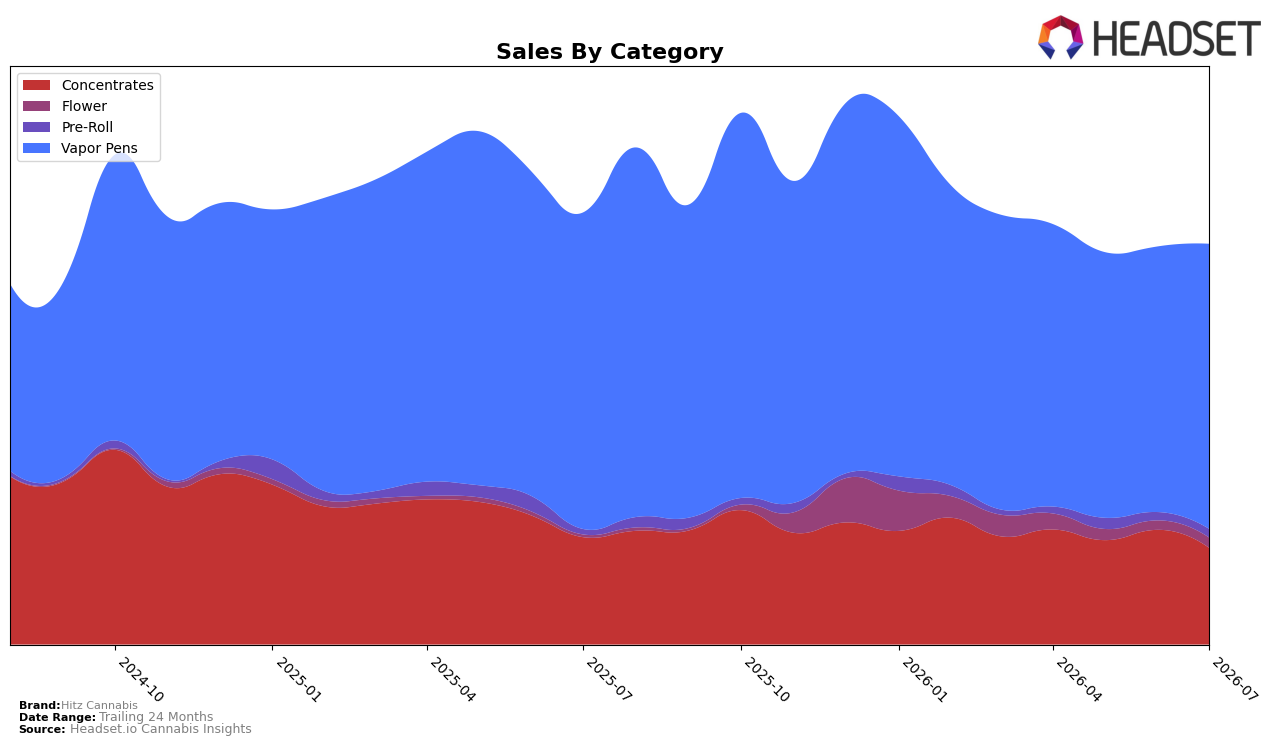

Hitz Cannabis concentrated 70.99% of July 2026 sales in Vapor Pens with a month-over-month gain of 7.32% but a year-over-year decline of 9.91%, while Concentrates held 24.14% share with a 15.63% MoM drop and a 9.90% YoY decline. Smaller lines moved in the opposite direction: Flower rose 8.87% MoM and 248.60% YoY to 2.63% share, and Pre-Roll grew 3.88% MoM and 56.58% YoY to 2.24% share. With brand-wide sales down 7.22% YoY and the average price down 6.10% YoY to $8.02, the mix shows a tilt toward lower-priced formats alongside recovery in niche segments, implying category breadth is cushioning Vapor Pen softness while price compression is a primary lever.

Given Vapor Pens anchor the portfolio at 70.99% share but carry a 9.91% YoY decline, and Concentrates lost 15.63% MoM share momentum, the brand’s 28 rank in Vapor Pens in Washington signals mid-pack visibility that relies on price-led wins rather than premium trade-up. The contrasting surges in Flower at 248.60% YoY and Pre-Roll at 56.58% YoY, despite their combined 4.87% share, indicate an entry-point strategy that can diversify revenue while Vapor Pen performance normalizes; the implication is to lean into expanding Flower and Pre-Roll doors and SKUs to offset Concentrates volatility and to protect ranking headroom in Vapor Pens through targeted, not across-the-board, pricing.

Competitive Landscape

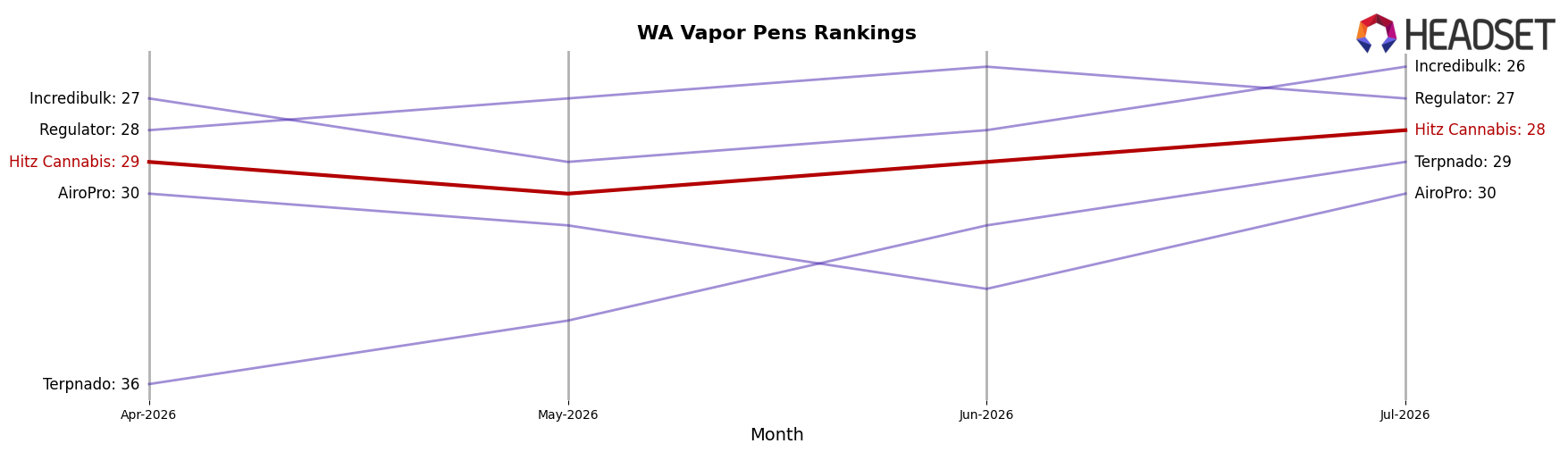

Hitz Cannabis sits at rank #28 in WA Vapor Pens in July 2026, down 3 positions year over year from #25 and up 1 place versus April 2026 when it was #29; the brand’s peak of #21 in October 2025 marks a 7-rank slide since that high, while its current standing places it 27 spots behind the category leader. Against competitors, Crystal Clear moved from #2 to #1 and posted a 12.6% year-over-year sales change, while Mfused fell from #1 to #2 with a 26.1% year-over-year decline; Full Spec climbed from #6 to #3 with a 12.9% increase, indicating upward mobility among leaders even as Hitz Cannabis drifts 3 ranks YoY. The pattern implies Hitz Cannabis is losing relative position while rivals with positive double-digit growth or improved ranks consolidate the top tier, signaling the brand must reverse share leakage to avoid further rank erosion.

Notable Products

Gorilla Glue #4 Distillate Cartridge (1g) posted the steepest decline in July 2026 at -13.2% and slipped to rank 3, while Blue Dream Distillate Cartridge (1g) moved up to rank 4 on a +24.0% month-over-month gain. Blackberry Kush Distillate Cartridge (1g) held rank 1 with a +4.0% lift and approximately $13,326 in sales, as two RSO items fell double digits with Blackberry Kush RSO down -10.8% at rank 8 and Narnia RSO Syringe down -11.1% at rank 5. Seven of the top ten are Vapor Pens, indicating the product mix is consolidating around cartridges and de-emphasizing RSOs for near-term growth focus.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.