Where to Buy

Honeybee is stocked at 149 licensed dispensaries across Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Joplin, and Kansas City. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

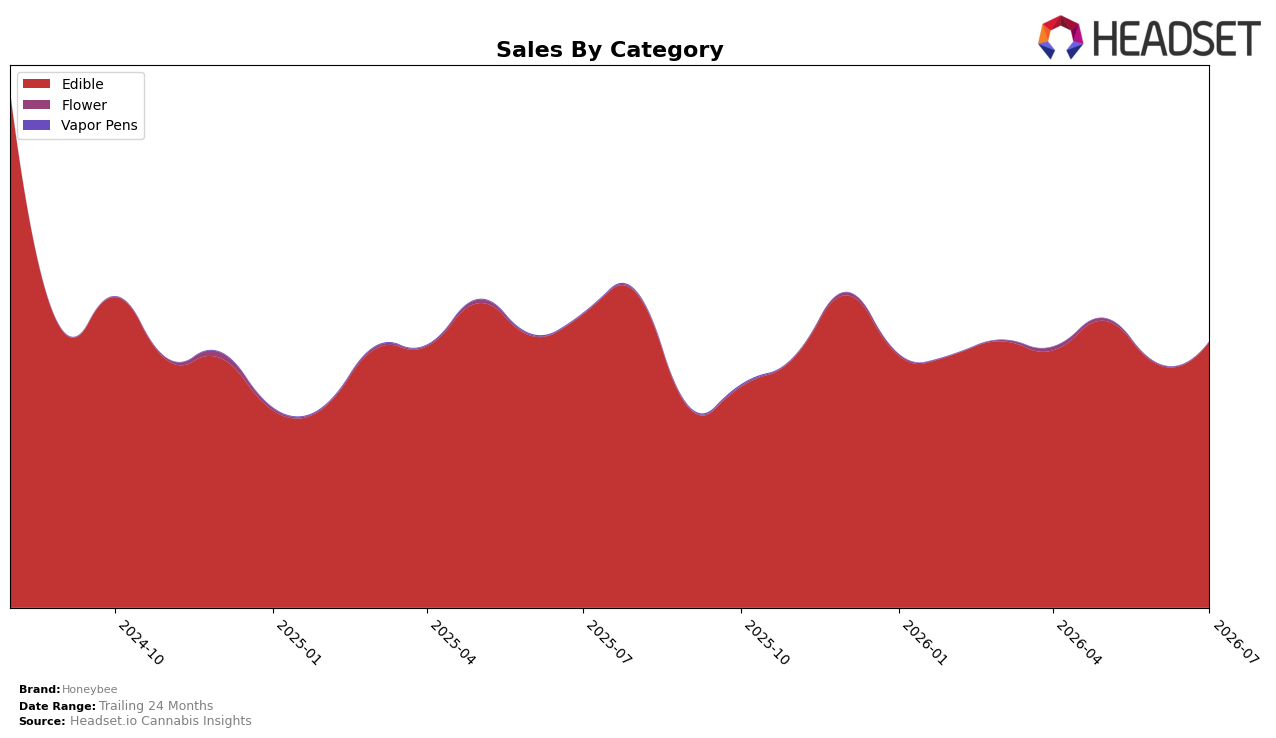

In July 2026, Honeybee remained a single-category brand with Edible at 100.0% of mix, while Edible sales shifted by -9.45% year over year and +9.42% month over month, indicating a rebound that does not fully offset prior contraction. The brand’s average price moved -13.39% YoY to $18.56 and the Edible category rose +9.42% MoM, pointing to unit-led recovery versus pricing, and rank at 11 in Missouri Edible frames the lift as sub-top-10 momentum without cross-category diversification. The pattern implies Honeybee is leaning on volume gains within Edible to counter a -9.62% brand-level YoY decline, trading price for share rather than expanding into adjacent categories.

The combination of a -13.39% YoY price move and +9.42% MoM sales lift within a 100.0% Edible mix suggests Honeybee is competing on accessibility to climb from rank 11 in Missouri Edible, with price elasticity driving near-term unit capture. Given a -13.76% 24-month trend alongside a -9.45% Edible YoY change and a fully concentrated mix, the implication is that sustainable share gains will rely on maintaining sub-$20 positioning while improving repeat rates rather than category expansion; in other words, price-led MoM recovery can stabilize rank before mix diversification becomes necessary.

Competitive Landscape

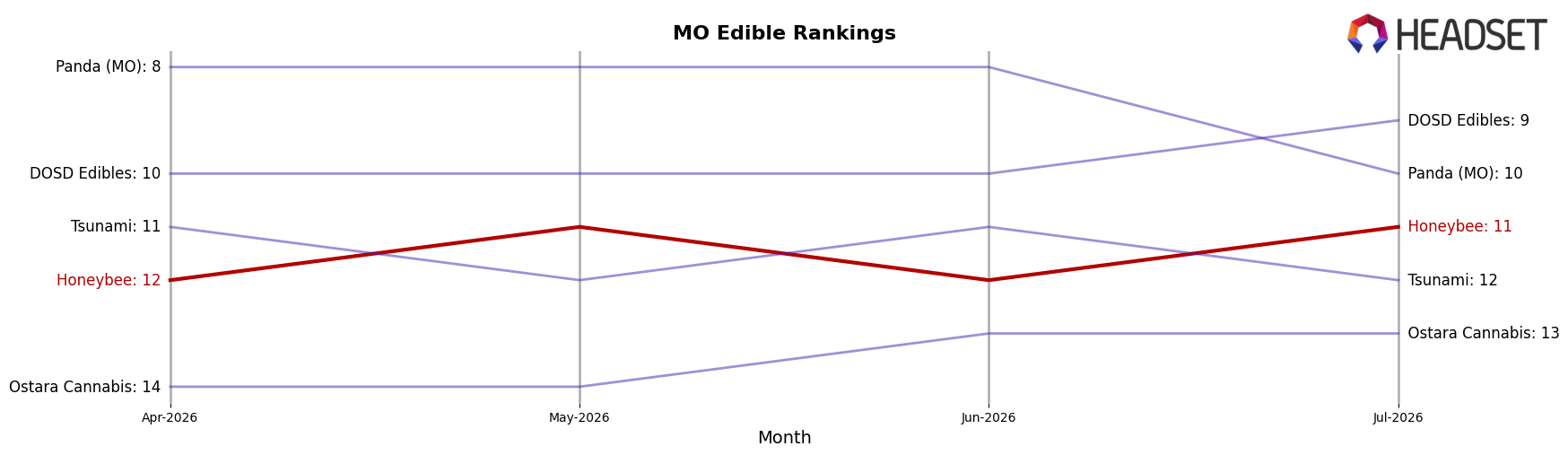

Honeybee is ranked #11 in MO Edible in July 2026, down 1 position year over year from #10, and up 1 spot versus April 2026 when it sat at #12; against its historical ceiling of #6 in August 2024, the current placement is 5 ranks lower. In contrast, Gron / Grön held at #1 year over year while its sales fell 5.5%, and Good Taste climbed from #8 to #4 on 63.8% sales growth, indicating Honeybee’s relative slippage is tied less to broad market contraction and more to share being captured by faster-rising peers; the trajectory implies a drift toward the mid-tier unless Honeybee reclaims momentum seen at its August 2024 peak.

Notable Products

Sour Raspberry Lemonade Gumdrops 20-Pack (100mg) posted the steepest decline in July 2026 at -16.35% and slid to rank 9, while CBD/THC 1:1 Sour Watermelon Passionfruit Gumdrops 20-Pack (100mg CBD, 100mg THC) fell -9.81% at rank 10, indicating flavor fatigue at the lower end of the top ten. In contrast, Blood Orange Strawberry Gumdrops 20-Pack (100mg) climbed +23.88% to rank 2 and Queen Bee - Blood Orange Strawberry Gumdrop Gummies (100mg) jumped +35.65% at rank 3, and together with Queen Bee - CBD/THC 1:1 Blue Raspberry Gummies 20-Pack (100mg THC, 100mg CBD) up +16.78% at rank 4, they signal momentum in both core flavors and 1:1 functional formats. Eight of the top ten are Edible Gumdrops, and Black Cherry Cola Gumdrops 20-Pack (100mg) held rank 1 with +8.33% MoM, suggesting Honeybee’s leadership is concentrated in repeatable gummy packs even as single-serve Queen Bee variants expand share. The pattern implies Honeybee is tilting the mix toward higher-velocity multi-pack gumdrops and 1:1 wellness SKUs, with selective pruning needed on underperforming sour profiles to protect the price ladder and defend a dollars base around $23.6k at the top SKU.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.