May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

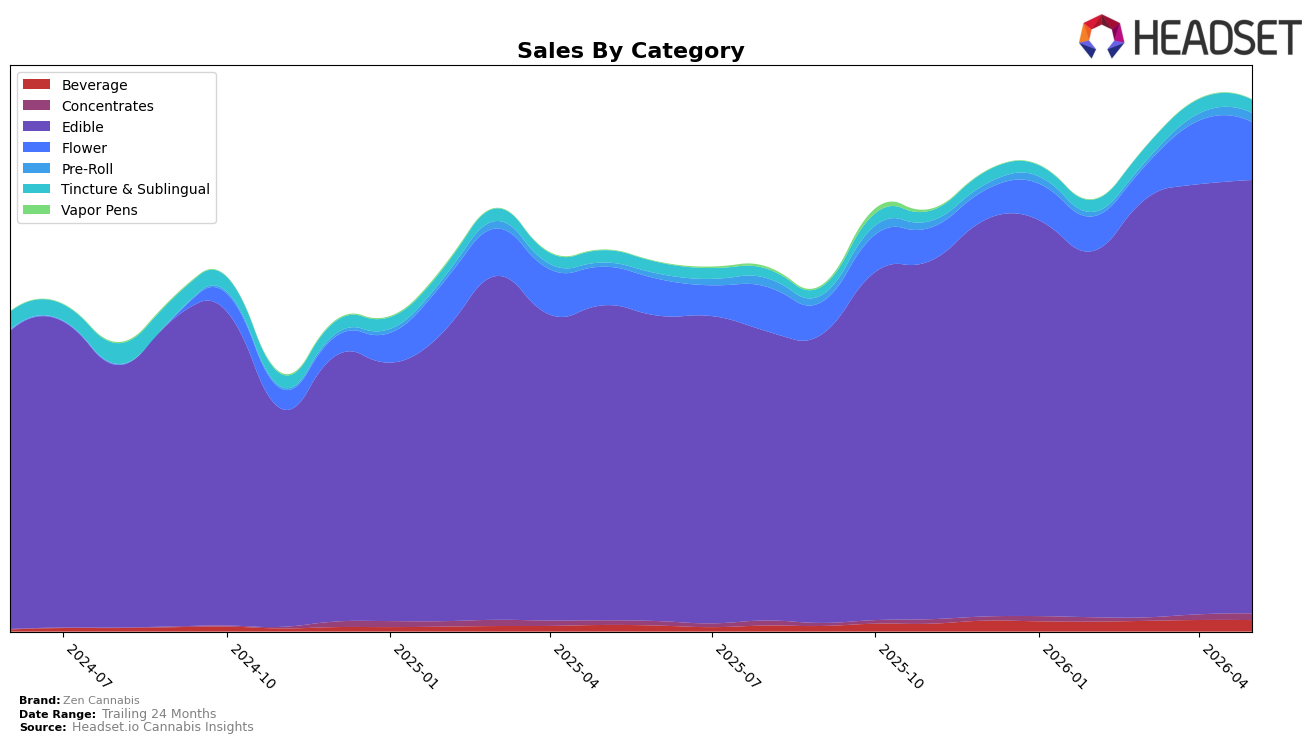

Edible dominated Zen Cannabis’s mix in May 2026 at 81.77% share with 37.62% year-over-year growth and a 0.74% month-over-month uptick, while the overall average price fell 4.78% YoY to $14.68. Flower held 10.88% share with 50.95% YoY growth but declined 8.64% MoM, and Pre-Roll, though only 1.64% share, surged 128.94% YoY and 28.98% MoM; by contrast, Beverage grew 77.88% YoY yet slipped 0.77% MoM. Tincture & Sublingual rose 7.83% YoY but dropped 8.49% MoM, and Concentrates increased 50.21% YoY with a 20.60% MoM lift; together these shifts imply a portfolio anchored in Edible with emerging momentum in Pre-Roll and Concentrates even as select form factors face monthly pullbacks.

The mix suggests a positioning centered on value-accessible ingestibles, as Edible scale coincides with a lower average price point and a rank of 7 in Missouri Edible, while Pre-Roll’s 28.98% MoM rise and Concentrates’ 20.60% MoM rise indicate traction in quicker-turn inhalables relative to Flower’s 8.64% MoM drop. Beverage’s 77.88% YoY expansion paired with a 0.77% MoM dip and Tincture & Sublingual’s 8.49% MoM decline point to experimentation without sustained monthly velocity, implying near-term share stability relies on maintaining Edible’s 81.77% share while selectively leaning into Pre-Roll and Concentrates to diversify growth channels.

Competitive Landscape

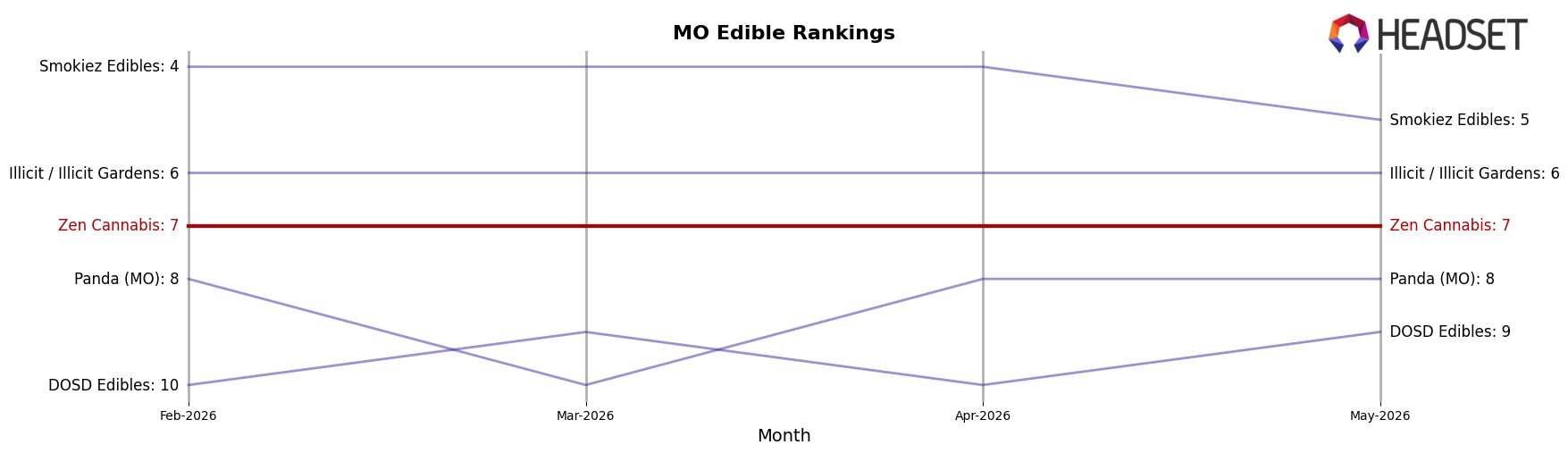

Zen Cannabis sits at rank #7 in MO Edible in May 2026, improving 2 positions from #9 year over year while holding flat versus February 2026 at #7; this places the brand at its peak rank of #7 in May 2026 and 2 spots behind the category’s top three. Competitively, Gron / Grön held #1 with a -14.1% YoY sales change, Wyld slipped from #2 to #3 with -11.8% YoY sales, and Good Taste climbed from #8 to #4 with +71.8% YoY sales, indicating that Zen Cannabis’s 2-rank YoY gain amid mixed competitor trajectories positions it as a steady mid-pack mover rather than a breakout share taker.

Notable Products

Sativa Fruit Punch Gummies 10-Pack (100mg) posted the sharpest movement in May 2026 with a -14.4% MoM decline and slipped to rank 2, while CBD/THC 4:1 Grape NiteNite Gummies 10-Pack (400mg CBD, 100mg THC, 50mg Melatonin) fell -7.4% yet held rank 1; together these shifts indicate demand is tilting away from standard 10-packs toward larger formats. Indica Mini Fruit Punch Gummies 25-Pack (250mg) rose 6.2% MoM at rank 3 as Sativa Mini Fruit Punch Gummies 25-Pack (250mg) was roughly flat at rank 4 (-0.4%), and the CBD/THC 4:1 Grape NiteNite Gummies 20-Pack (400mg CBD, 100mg THC) slid -9.3% at rank 5, pointing to momentum concentrating in 25-pack minis rather than mid-size wellness packs. With four of the top ten coming from Hybrid Mini Assorted Flavor 25-pack variants spanning 250mg, 500mg, and 1000mg, the assortment is clustering around higher-dose mini formats even as the 500mg version dipped -6.7% at rank 9 and the 250mg version gained 4.9% at rank 6, implying a strategic edge in reinforcing mini multi-pack value over single 10-packs despite a $174,637 launch for the 1000mg SKU at rank 10.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.