Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Honu is stocked at 174 licensed dispensaries across Washington and Oregon, 171 of them in Washington, with the deepest coverage in Olympia, Spokane, Seattle, Tacoma, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

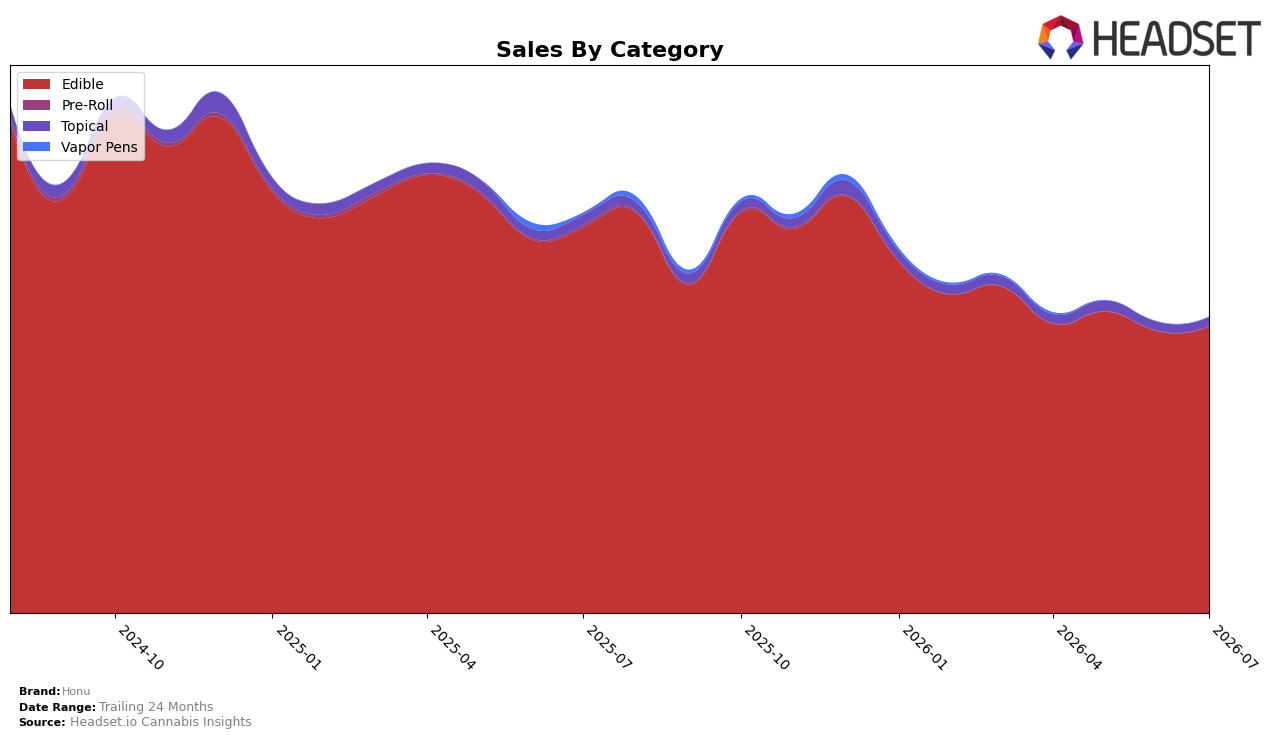

In July 2026, Honu concentrated 97.10% of sales in Edible while Topical held 2.90%, with Edible down 25.64% year over year but up 1.71% month over month, and Topical down 13.00% year over year but up 0.64% month over month. Against a brand-level year-over-year sales change of -26.07% and an average price shift of -5.92%, Edible’s month-over-month uptick paired with Topical’s smaller base and slower month-over-month lift indicates category dependence is easing slightly at the margin but still anchors performance; the pattern implies that maintaining a narrow focus in Edible keeps Honu sensitive to that category’s demand cycles even as July 2026 shows incremental stabilization.

With Edible at 97.10% share and ranked 17 in Edible in Washington, a -25.64% year-over-year decline alongside a 1.71% month-over-month gain suggests pricing and mix are working tactically while long-cycle demand remains lower. The Topical mix at 2.90% with a -13.00% year-over-year change and 0.64% month-over-month growth implies limited diversification headroom today; combined with a -5.92% average price move, this skew suggests Honu’s positioning hinges on depth in Edible rather than breadth across adjacent formats, which implies July 2026’s small month-over-month lifts are maintenance signals rather than drivers of a mix-led reset.

Competitive Landscape

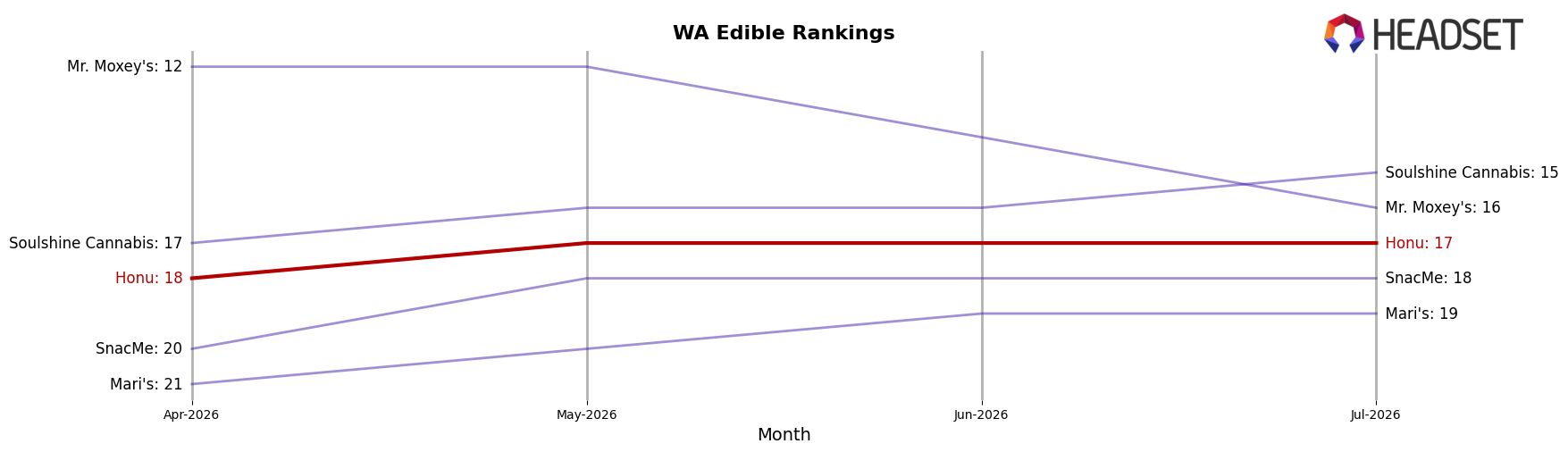

Honu is ranked #17 in WA Edible in July 2026, unchanged YoY from #17, while improving 1 rank position versus April 2026’s #18 and sitting 3 places below its peak at #14 from December 2024; in contrast, Wyld held #1 both YoY and currently with a 7.99% YoY sales increase, and Journeyman moved up from #5 to #4 with 6.47% YoY growth. The flat YoY rank alongside a recent 1-position uptick suggests Honu’s trajectory is stabilizing rather than accelerating, implying share preservation amid leaders consolidating at the top.

Notable Products

Indica Milk Chocolate Turtle 10-Pack (100mg) posted the steepest decline in July 2026 at -10.1% MoM while slipping to rank 2, contrasted by Sativa Peanut Butter Cups Chocolate 10-Pack (100mg) up 15.5% MoM at rank 4; this divergence signals shifting demand within chocolate subtypes rather than a broad category downturn. Indica Peanut Butter Cups Chocolate 10-Pack (100mg) held rank 1 with a -5.7% MoM dip against $22,846 in sales, while Gimme Sa'More! Treats 10-Pack (100mg) climbed 8.3% MoM to rank 3, suggesting mix resilience at the very top despite pressure on one legacy turtle SKU. With all top-10 items in Edible and multiple Peanut Butter Cups variants occupying top-5 positions, the portfolio concentration in chocolate formats is intensifying even as single-serve Sativa Milk Chocolate Turtle (10mg) rose 27.5% MoM at rank 8, pointing to trial-driven entry formats supporting the core multipacks. The pattern implies Honu is pivoting toward a peanut-butter-and-caramel-led chocolate mix with multipacks anchoring share while single-serve lifts broaden the funnel.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.