May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

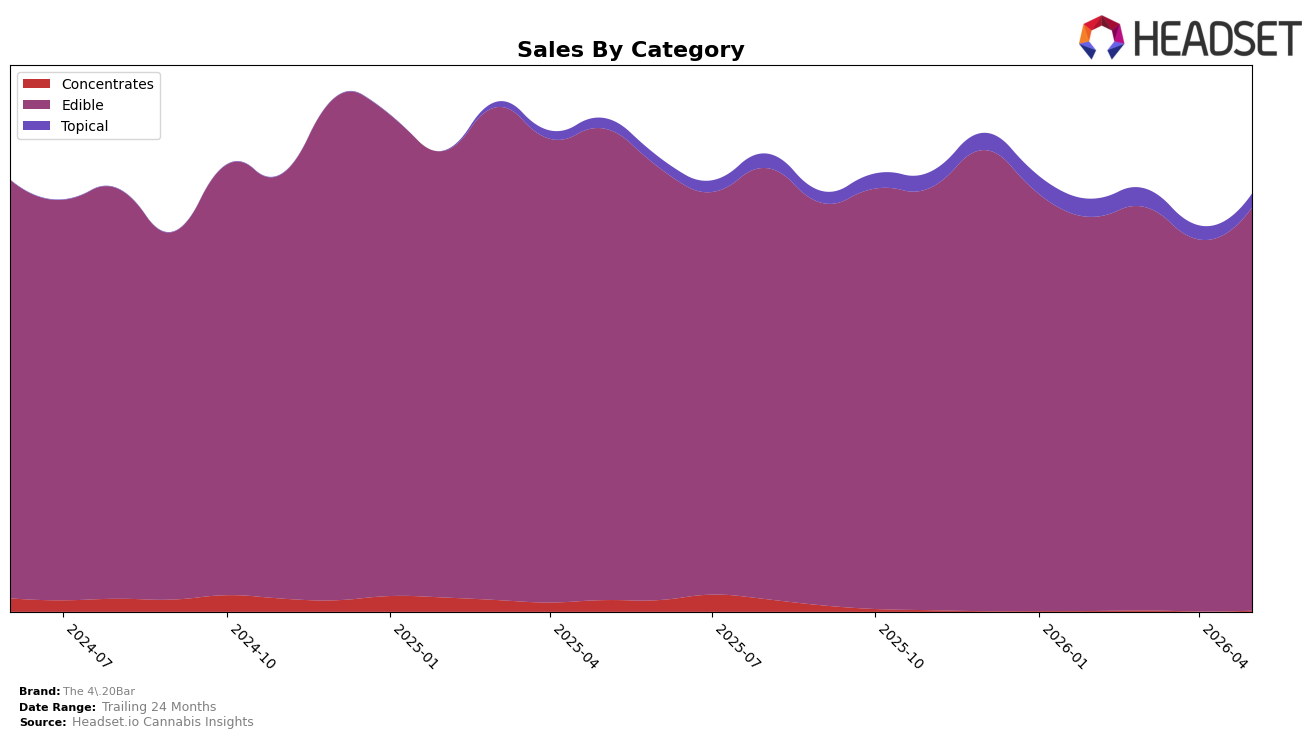

In May 2026, The 4.20Bar concentrated 96.58% of sales in Edible, with Edible up 8.39% month over month but down 14.56% year over year, while Topical held 3.26% share with a 0.92% month-over-month decline and a 34.75% year-over-year increase. Concentrates fell to 0.16% share with a 94.08% year-over-year drop and no reported month-over-month figure, and average price edged down 1.70% year over year to $14.46, implying mix-driven volume movement alongside category-specific retraction.

These shifts imply The 4.20Bar is doubling down on Edible as its demand anchor while selectively expanding Topical as a higher-growth adjacency, a posture consistent with a rank of 13 in Edible within Washington and a May 2026 brand-level year-over-year sales change of -15.36%. With Edible’s month-over-month gain of 8.39% offsetting a 14.56% year-over-year decline and Topical’s 34.75% year-over-year rise from a 3.26% share base, the portfolio suggests a strategy to defend share in the core while testing margin or basket accretion via Topical, rather than diversifying into Concentrates where a 94.08% year-over-year contraction implies limited traction.

Competitive Landscape

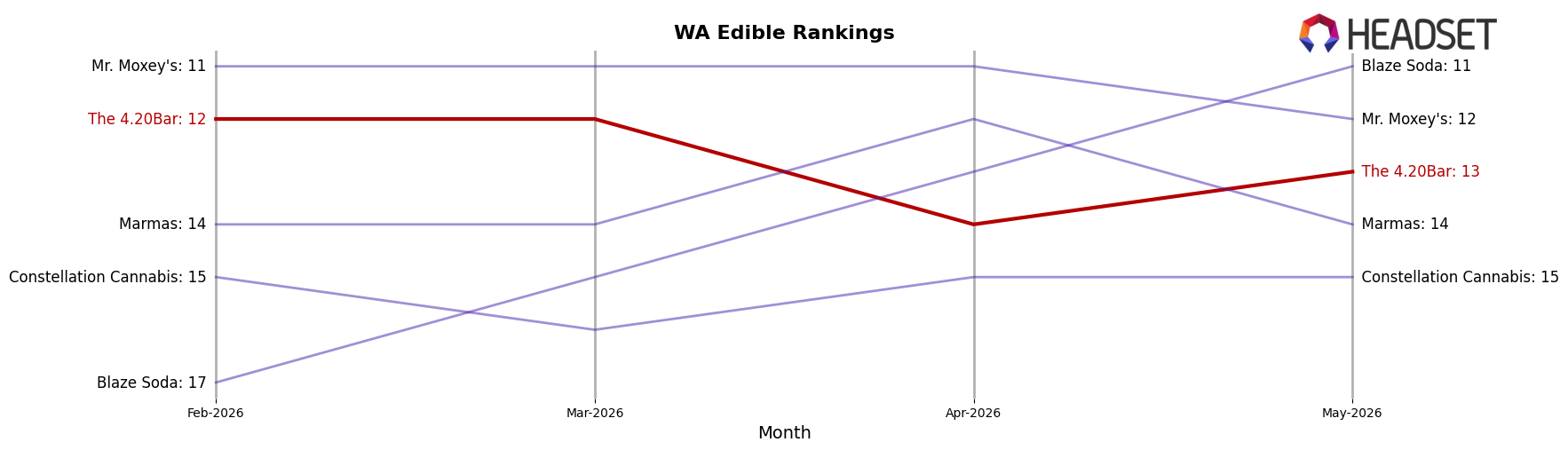

The 4.20Bar sits at rank #13 in WA Edible in May 2026, a 1-place improvement from #14 year over year and a 1-place decline from #12 three months ago, while still trailing its peak of #11 from May 2024; meanwhile, Wyld held #1 year over year and in May 2026 as its sales grew 26.5%, and Green Revolution maintained #2 with a 15.8% sales increase, indicating that The 4.20Bar’s modest rank lift is occurring amid upward pressure from leaders. With Hot Sugar steady at #3 despite an 8.1% sales decline and Craft Elixirs fixed at #5 with a 6.4% drop, the competitive gap is widening at the very top while volatility below the top five is limited, implying The 4.20Bar’s current trajectory points to incremental share defense rather than a path back to its #11 peak without a step-change in velocity.

Notable Products

Minis - CBD/CBN/THC 2:2:1 Dark Chocolate Sea Salt Bites 10-Pack (200mg CBD, 200mg CBN, 100mg THC) posted a 46.7% month-over-month rise to enter May 2026 at rank 5, while Minis - CBG/CBC/CBD/THC 1:1:1:1 Milk Chocolate Bites 10-Pack (100mg CBG, 100mg CBC, 100mg CBD, 100mg THC) slipped 7.7% to rank 4. The top three ranks stayed concentrated in 1:1 SKUs, with rank 1 up 5.2% and rank 2 up 19.5% as rank 3 edged only 1.5%, implying that multi-minor-cannabinoid variants are gaining share without dislodging the 1:1 leaders. The mix points to The 4.20Bar leaning into functional minor-cannabinoid formats to drive incremental growth alongside steady 1:1 anchors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.