Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sinners & Saints is stocked at 27 licensed dispensaries across Washington, with the deepest coverage in Bellingham, Everett, Lynnwood, Mt Vernon, and Olympia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

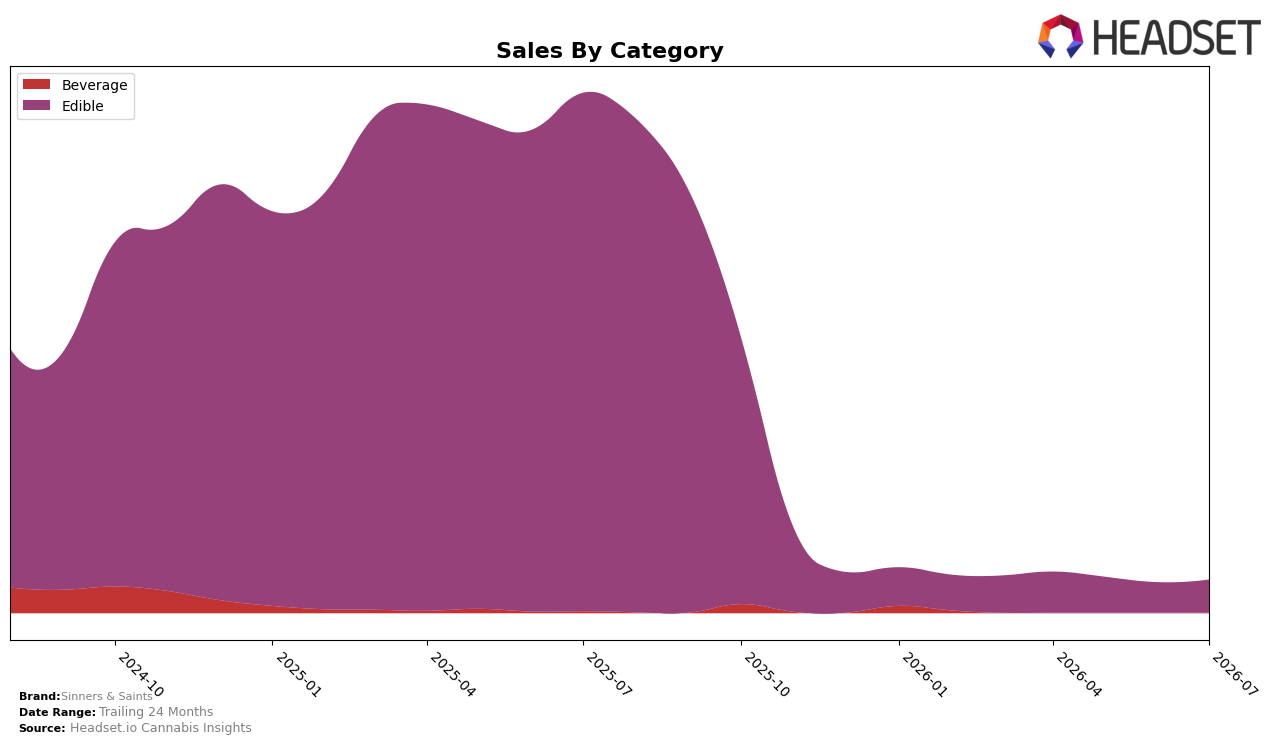

In July 2026, Sinners & Saints operated as a single-category brand, with Edible accounting for 100.0% of sales and a month-over-month change of 8.83% contrasted against a year-over-year decline of 93.66%. Average price fell 10.25% year over year to $13.81 while total brand sales declined 93.68% year over year, consolidating entirely in Edible. The brand held rank 41 in Edible within Washington, and the 24-month sales change of -86.86% underscores that the Edible-only mix is the result of contraction rather than diversification. The pattern implies that short-term volume stabilization within Edible is not offsetting a multi-period retrenchment, leaving the brand dependent on a single price-sensitive segment.

The combination of a 100.0% category share in Edible and a 10.25% price decrease alongside an 8.83% MoM sales uptick signals a pricing-led nudge that is insufficient to regain lost rank position beyond 41 or reverse the 93.66% YoY category decline. With total sales down 93.68% YoY and 86.86% over 24 months, the brand’s positioning is drifting toward a value-oriented Edible niche where elasticity drives short-run gains but limits margin leverage. The implication is that remaining at rank 41 in Washington while concentrated in a single category narrows competitive optionality, suggesting the near-term path is price-based defense rather than share capture through assortment breadth.

Competitive Landscape

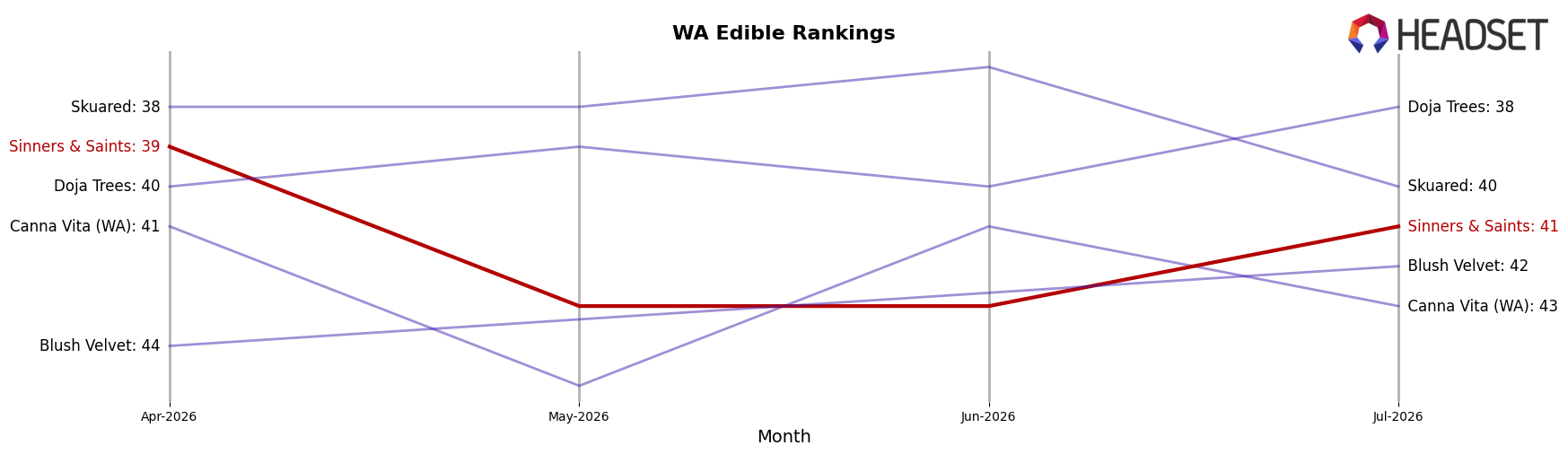

Sinners & Saints is currently ranked #41 in WA Edible, down 25 positions year over year from #16 to #41, and 2 spots lower than April 2026 when it was #39; this follows a peak at #16 in July 2025 and contrasts with a 0-position change for Wyld holding #1 YoY while posting a 7.99% sales increase, and with Craft Elixirs slipping from #4 to #5 alongside an 8.01% sales decline. Compared with Journeyman improving from #5 to #4 and gaining 6.47% in sales YoY, Sinners & Saints’ 2-rank slide since April 2026 and 25-rank YoY drop indicate that momentum has shifted toward incumbents consolidating the top tier, implying that regaining relevance will require reversing multi-quarter share loss rather than counting on category churn.

Notable Products

CBD/CBC/CBG/THC 1:1:1:1 Mango Passionfruit Gummies 10-Pack (100mg THC, 100mg CBD, 100mg CBC, 100mg CBG) delivered the standout move in July 2026 with +78.3% MoM to rank 2, while the top-ranked CBN/CBD/THC 2:2:1 Blue Raspberry Gummies 10-Pack grew +29.4% MoM, signaling a shift toward balanced multi-cannabinoid formats across the very top of the chart. In contrast, CBD/CBC/CBG/THC 1:1:1:1 Strawberry Kiwi Gummies 10-Pack fell -48.8% MoM at rank 5, and Pomegranate Acai in the same 2:2:1 family plunged -75.8% MoM at rank 7, indicating polarization between winning and lagging flavor variants within similar ratio architectures. Four of the top five are Edible SKUs with multi-cannabinoid ratios, and two 2:2:1 CBN/CBD/THC items sit at ranks 1 and 3 while single-flavor extensions like Mango Passionfruit 10-Pack (100mg) dropped -74.6% at rank 8, implying that potency-tiered, ratio-led gummies are consolidating share while low-potency or single-compound variants lose relevance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.