Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

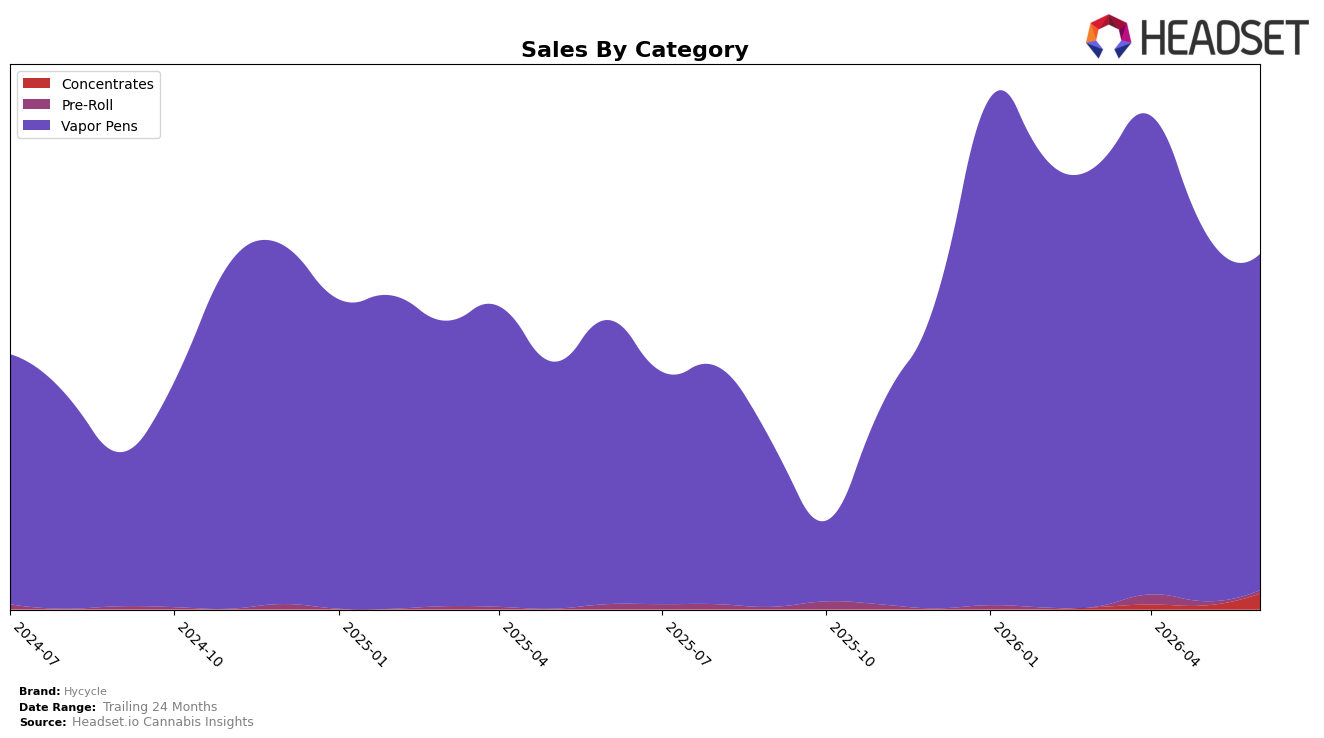

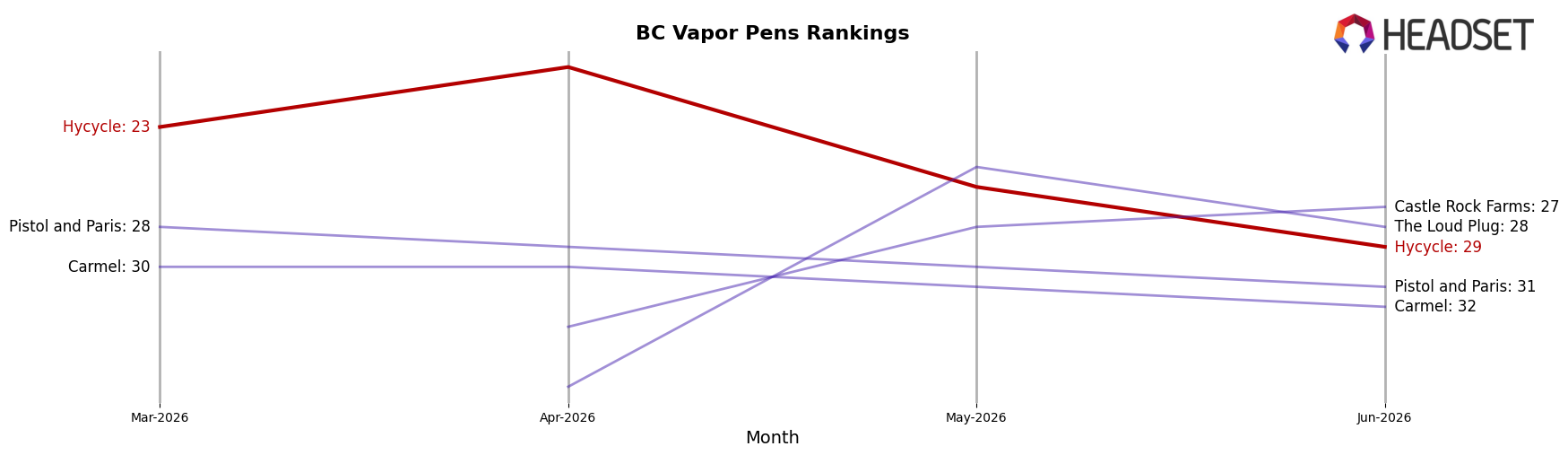

Hycycle concentrated 94.73% of June 2026 sales in Vapor Pens, where year-over-year sales rose 18.34% but month-over-month slipped 9.23%, while Concentrates expanded to 4.43% share on a 317.34% month-over-month surge despite no year-over-year baseline. Pre-Roll fell to 0.84% share with a 35.72% year-over-year decline and a 21.22% month-over-month drop, even as brand-level sales grew 22.92% year over year and average price increased 5.30% to $37.08. In British Columbia Vapor Pens, Hycycle held rank 29, implying that category concentration is sustaining annual growth but recent monthly softness in the core SKU set is offset by a tactical shift toward Concentrates.

The mix shift—Vapor Pens losing 9.23% month over month as Concentrates jumped 317.34% and Pre-Roll contracted 21.22%—implies Hycycle is rotating assortment toward higher-ticket niche formats (Concentrates at a $41.79 average price versus Vapor Pens at $37.06) to protect revenue density while the core cools. With 94.73% of volume still anchored in Vapor Pens and rank 29 in British Columbia, the strategy suggests near-term reliance on a dominant category for scale while seeding a secondary pillar to diversify risk and lift mix-level pricing power.

Competitive Landscape

Hycycle sits at rank 29 in BC Vapor Pens in June 2026, down 4 positions year over year from rank 25 and 6 spots below its January 2026 peak at rank 18, while also sliding 6 places from rank 23 three months ago; by contrast, BoxHot held rank 1 with a -7.1% YoY sales change and Spinach climbed from rank 4 to rank 2 on +129.9% YoY sales, indicating Hycycle’s relative share is being diluted as faster movers ascend. The combination of a 4-rank YoY decline and a 6-rank three-month drop, alongside competitors gaining or holding top-5 positions, implies Hycycle’s trajectory is downward unless mix, pricing, or activation can counter accelerating category leaders.

Notable Products

The steepest decline came from Sour Diesel Distillate Cartridge (1.1g), down 53.7% month over month and sitting at rank 6, while White Widowmaker Liquid Diamonds Cartridge (1g) fell 16.4% and slipped to rank 2. In contrast, Blue King Live Resin Disposable (1g) in Vapor Pens jumped 33.3% to rank 5 and Ace - Limonone No 9 Live Resin Disposable (1g) rose 20.6% at rank 3, indicating momentum is concentrated in disposables even as certain cartridges retrench. With Vapor Pens occupying ranks 1 through 8 and four of the top ten coming from the Limonene/Ace or Blue King live resin family, the mix signals a pivot toward higher-velocity disposable formats and terpene-led positioning rather than broad cartridge expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.