Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

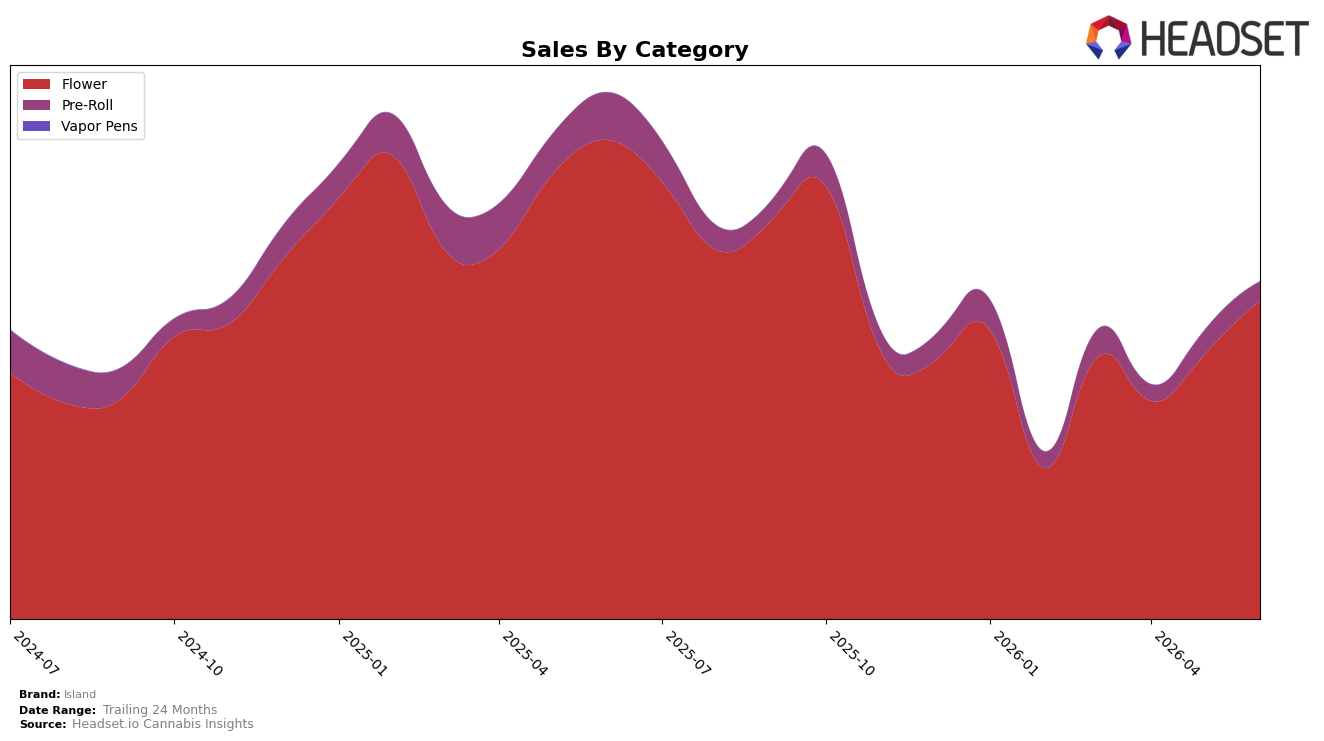

In June 2026, Island concentrated 94.40% of sales in Flower while Pre-Roll accounted for 5.60%, a skew that widened as Flower rose 20.40% month over month and Pre-Roll fell 22.41% month over month. Year over year, Flower declined 33.59% and Pre-Roll fell 60.04%, aligning with a total brand sales change of -35.97% year over year and a 12.25% increase in average price. With an average Flower price of $51.36 versus $8.22 in Pre-Roll and a state-category position at rank 20 in Flower in Illinois, the mix implies Island is leaning into premium-priced Flower to buffer volume erosion while accepting reduced breadth in value-oriented formats.

The combination of a 20.40% month-over-month rebound in Flower alongside a 22.41% month-over-month contraction in Pre-Roll, paired with a 60.04% year-over-year decline in Pre-Roll versus 33.59% in Flower, signals a deliberate pivot toward higher-ticket Flower that may defend share in a top category while ceding price-sensitive occasions. Given the brand’s -35.97% year-over-year sales trend against a 22.53% increase over 24 months and a current category rank of 20 in Flower in Illinois, the path forward implies Island’s positioning hinges on deepening Flower differentiation and selective retrenchment from lower-margin Pre-Rolls to stabilize rank and margin.

Competitive Landscape

Island sits at rank #20 in Illinois Flower in June 2026, down 6 positions year over year from #14, and up 4 ranks versus March 2026 when it was #24; the brand’s peak of #14 in June 2025 frames a 6-position slide over 12 months while the recent 3-rank climb in the spring quarter signals near-term stabilization. In contrast, High Supply / Supply holds #1 both this year and last year with sales up 32.1%, while RYTHM remains at #2 year over year despite a 5.2% sales decline; meanwhile, Good Green advanced from #4 to #3 alongside 30.9% sales growth. The pattern implies Island has ceded rank share to faster-rising leaders but may be stabilizing off its March 2026 trough, indicating that without a shift in velocity the brand risks remaining in the #18–#22 band rather than re-approaching its #14 peak.

Notable Products

Marz (14g) posted the largest movement in June 2026 with a +211.8% month-over-month surge into rank 9, while Sake Pre-Roll (1g) fell 17.7% yet held rank 1. Layer Cake (14g) in rank 7 grew 11.8% month over month, whereas Crazy Hazy (3.5g) slid 41.0% at rank 2, and six of the top ten are Flower SKUs, concentrating mix in larger pack sizes. The only cited dollar figure, Planet Sherb (28g) at $63,796 in rank 10, sits alongside Puffinz (14g) at rank 6, reinforcing a tilt toward value-weight formats over single grams. The pattern implies Island is pivoting toward heavier-weight Flower where volatility can be harnessed for share gains while pre-rolls stabilize mix at the top.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.